Personal Wealth Management /

About That Turkish Flu

Turkey’s problems, though severe, shouldn’t infect the rest of the world or Emerging Markets.

Turkey’s turmoil continued Monday, with the lira hitting another record intra-day low against the dollar—then firming after the central bank said it would hold an extraordinary meeting Tuesday to “discuss recent developments and take the necessary policy measures for price stability” and release its plans in a midnight statement. Meanwhile, headlines continued warning Turkey is a bellwether for Emerging Markets’ broader vulnerability to the end of Fed bond buying—both in terms of experiencing capital flight and adjusting monetary policy to deal with resulting currency declines appropriately. As we said here and here, however, this view is rather misguided—Turkey’s problems have nothing to do with Fed policy, and its central bank decisions aren’t emblematic of decision making throughout the developing world. Simply, we highly doubt Emerging Markets—or the world—will catch the Turkish flu.

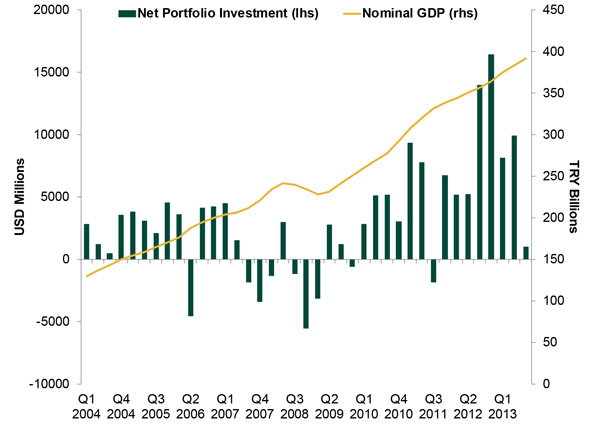

It is true Turkey has occasionally seen high portfolio investment inflows since the Fed launched quantitative easing (QE) in November 2008—but there doesn’t appear to be a direct relationship between the two. As shown in Exhibit 1, net inflows were quite choppy through 2010. They’ve gained steam since in absolute terms, but so has Turkey’s economy. For much of that span, Turkey was considered one of Emerging Markets’ darlings, with a rapidly modernizing economy and ambitions to join the EU (many observers were willing to turn a blind eye to Prime Minister Recep Tayyip Erdogan’s increasingly authoritarian methods, which included neutering the military and silencing journalists). Higher inflows since 2011 were likely tied to the growing opportunities as Turkey expanded and gained more international notice.

Exhibit 1: Turkey Portfolio Investment Inflows vs. GDP

Source: Central Bank of the Republic of Turkey, Federal Reserve Bank of St. Louis, as of 1/27/2014.

Turkey’s problems stem from within its borders—namely, from mounting political instability (something most Emerging Markets don’t share). Late last May, what began as a small protest against the destruction of a public park turned into countless throngs demonstrating against Erdogan across 20 cities—and suffering police brutality for their trouble. According to one report from the Turkish Medical Association, protesters were exposed to tear gas “for up to eight hours a day over multiple days,” in June, and thousands reported lingering after effects in September.

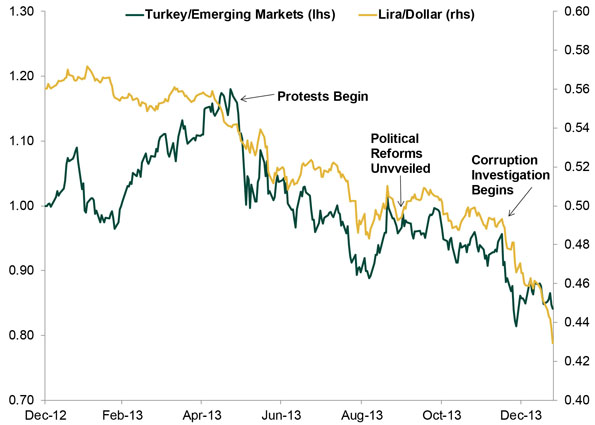

The violence spooked markets (Exhibit 2). The lira had been relatively stable and Turkish stocks outperforming for much of 2013’s first five months, but that changed when the protests kicked off. The lira plunged, Turkish stocks underperformed wildly, and portfolio investment flows turned negative in June and July—when violence was at its peak. Markets briefly stabilized late last year—and portfolio investment inflows were positive through November—after Erdogan announced a raft of shallow political reforms, but the trouble began anew in late December, when the judiciary hit Erdogan with a corruption investigation. Protests resumed (and then some), Erdogan sacked dozens of judges, and the ruling and opposition parties came to blows in Parliament (landing the opposition’s deputy leader in the hospital). The crackdown has been swift and brutal, and on Friday, Erdogan likened the unrest to civil war.

Exhibit 2: Turkish Markets and Unrest

Source: FactSet, as of 1/27/2014. Turkish stocks are outperforming Emerging Markets when the green line is rising.

This unrest is what touched off the lira’s latest freefall—political chaos drives massive investor uncertainty. The central bank isn’t helping matters. Typically, central banks will intervene to stem a currency slide, hiking overnight rates to attract foreign capital. But Turkey’s central bank operates under Erdogan’s thumb, and he has all but ruled out a rate hike by fiat, denouncing it as out of step with the country’s cultural aims. So the bank has resorted to using its forex reserves, by some reports depleting one-third of its net reserves since June. It hasn’t helped, however, and now the central bank is in a pickle. Last week, policymakers tried to placate both Erdogan and the markets, keeping money market rates at 7.75%—except for special “additional monetary tightening days,” when they’d rise to 9%. But the lira kept falling—haphazard monetary policy fueled, rather than helped, uncertainty.

Hence Tuesday’s super special midnight meeting. Judging by the lira’s midday stabilization, markets seem to think policymakers will emerge with something credible. But only time will tell whether economic interests beat political—these things are impossible to forecast.

But for global investors, what matters most is this: Turkey’s story, though harrowing, is an outlier. Most Emerging Markets aren’t ruled by a thuggish tyrant willing to bring his country to the brink of civil war and markets to the brink of collapse simply to keep his grip on power. Most, like South Korea, India and Mexico, have healthy democracies. That’s not to minimize political risks—Egypt and Thailand are going through their own difficulties at the moment—but problems the size of Turkey’s simply aren’t the norm.

The same goes for monetary policy. Many Emerging Markets have politically independent central banks, giving them more latitude if the going gets tough—they won’t have to bow to political or cultural pressures. That doesn’t guard perfectly against monetary policy errors, but history shows free central banks have better track records, overall and on average, than politicized institutions.

In the short term, rattled sentiment can impact currencies in other, healthier Emerging Markets, giving the appearance of a contagion. But sentiment-driven volatility doesn’t make a categorical currency crisis. That would require severe fundamental issues across a wide swath of the developing world—not the case today, with most Emerging Markets nations growing and stable.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Insights Ken Fisher on Inflation Data, Currency Reset Risks, Commodity Opportunities and More– April 20262026-04-17

-

Market Analysis Foraging Through Japan’s February Data2026-04-17

-

Expert Commentary This Week in Review | Iran Conflict Update, Canada Election, UK GDP

2026-04-17

2026-04-17 -

Market Analysis An Economic Check In on the UK2026-04-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today