Personal Wealth Management /

Keep Calm as Stocks Carry On

Stocks’ quick drop last week led to many fears more is to come. Our suggestion? Stay cool.

Volatility seems to have caught some traders’ eyes. By Spencer Platt/Getty Images.

January’s bumpy ride got a little bumpier last Friday, when S&P 500 fell -2.1%—the worst plunge in 2014. (Just 16 trading sessions.) Short-term volatility can rattle even the toughest of nerves, but at times like this, it’s important for long-term investors to stay cool and take a longer view. Stocks weather steep moves routinely amid strong bull market years—volatility is commonplace in markets. And yet, stocks overcome this negative volatility frequently.

The mediaseems to think last week’s drop is tied to a brewing Emerging Markets currency crisis, driven by the slowing of Fed bond purchases (aka quantitative easing, or QE). The popular narrative holds that easy Fed money has flooded into the developing world since QE began, propping up economies and asset prices in those nations—and ending QE will be like pulling the rug out. Though, as we wrote here, after an initial burst—largely a reversal of outflows occurring during the financial panic—Emerging Markets portfolio investment inflows haven’t been gangbusters during QE. Nor have Emerging Markets economies and stock markets—economically, many slowed, and Emerging Markets stocks have underperformed during the bull. If QE were so massively positive for the category, the reverse would be more probable.

As for contagion, short-term currency volatility is possible, just like equity volatility. But the worst of the rout is confined to Turkey, Argentina, South Africa and Russia—all of which have deep-rooted, domestically isolated fundamental issues. Turkey’s political turmoil has spooked markets locally for nearly a year, and its monetary policy became just as chaotic this week. Argentina’s economy suffers from crippling government intervention and haphazard monetary policy. South Africa has far fewer political issues, but it’s economically dependent on metals and mining—an industry trapped in a big slowdown. Energy-dependent Russia is in a similar position, thanks to the shale boom. These are fringe issues—they aren’t representative of all developing economies. Overall and on average, Emerging Markets are in good fundamental shape—and have high forex reserves, just in case. Short-term volatility notwithstanding, a true categorical currency crisis is highly unlikely. The coverage fretting otherwise, in our view, is just noise.

Still, this recent volatility has many people jumping to conclusions about future market direction. Some headlines already say it’s a correction—a quick, sentiment-driven drop of about -10% to -20%. Maybe it is, but it’s too soon to tell. Take 2013—we didn’t have a correction, but we did have 17 days where the S&P 500 dropped by -1% or greater. Sometimes isolated volatility just happens during bull markets. Yes, sometimes corrections follow, but they’re never clear without hindsight. By the time you’ve identified a correction, the downside could almost be over—they start and end without warning, and the inflection points are impossible to time. Navigating a correction requires near-perfect timing—getting out before markets have fallen too much, and getting back in at a lower point, before that quick recovery—just when fear is probably near its apex. We aren’t aware of anyone who’s managed this repeatedly. And investors certainly won’t get there by assuming big one-day drops predict a correction—volatility is too random, and assuming it’s predictive is too myopic.

Short-sightedness is deadly for long-term investors. If acted on, it can severely impact long-term returns. Volatility—whether big intraday moves or corrections—is the tradeoff for long-term growth. Consider it the cost of doing business. Since this bull market began on March 9, 2009, the MSCI World Index has already had five corrections—yet it’s up 161%.i

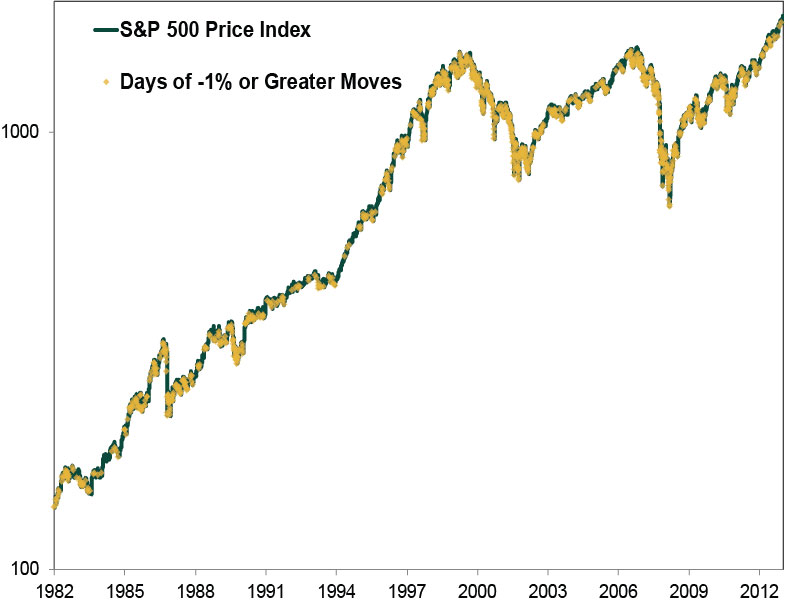

But take an even broader look: From 1982 to 2013, the S&P has fallen by -1% or more 954 times. The cumulative S&P 500 price return over this period? A whopping 1214.2%. (Exhibit 1) Sell out at the bottom of a correction or after a big down day, and you could miss out on significant upside, making your goals harder to reach. Quick drops are uncomfortable, regardless of whether they occur over a day, week, month or more. But they’re also normal and expected during bull markets—they help keep stocks from running ahead of reality. That’s healthy! It’s important for folks to consider the larger, longer-term picture.

Exhibit 1: S&P 500 Days of -1% or Greater Moves, 1982-2013 (Logarithmic Scale)

Source: FactSet as of 1/23/2014. S&P 500 price index return, 12/31/1982 – 12/31/2013.

At times like this, we suggest investors put these dips and drops into perspective, stay disciplined, and look beyond the next day, week or month. Consider instead what stocks are likeliest to do over a more actionable period, like the next year. With global growth continuing (even accelerating), the political climate favorable and sentiment far from euphoric, the bull market appears well positioned to continue.

i Source: Factset, MSCI World Total Returns, 03/09/2009 – 01/24/2013.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today