Personal Wealth Management / Market Analysis

An Election Palate Cleanser

October's PMIs show businesses globally are growing just fine.

Despite recent GDP reports from the US, UK, eurozone and China showing the global economy's heavy hitters grew just fine in Q3, many folks remain concerned world growth is faltering. But there is a bullish array of other data that should help allay these fears. We are referring, of course, to the recent bevy of purchasing managers' index (PMI) reports. If you want data-driven reasons to be bullish, you have a lot to like here. Though just one month, October manufacturing and services PMIs add another section to a constantly overlooked story: The global economy is broadly growing, amid constant doubts.

For some quick background, purchasing managers' indexes are monthly surveys that inquire about general business activity. Respondents will answer whether business was better, worse or about the same, as well as more nuanced queries: details about new orders, hiring, export orders, inventories and some squishy stuff like expectations of future orders. After compiling all this information, the survey compilers work their magic and, vóila!, out pops a number. Readings above 50 mean more businesses grew than contracted; below 50, vice-versa.

However, like any dataset, PMIs have their limitations. Being rather high-level, they don't reveal the magnitude of growth-just the breadth. A firm could grow (or contract) bigly[i] one month, but that wouldn't be captured. And while monthly releases provide a regular stream of data-a positive-media types have a tendency to hype up a smashing report or bemoan a weaker one. Longer-term trends are more meaningful than month-to-month volatility, an important caveat to consider. With all that said, this month's PMIs for both manufacturing and services counter the frequent concerns of a weak global economic environment.

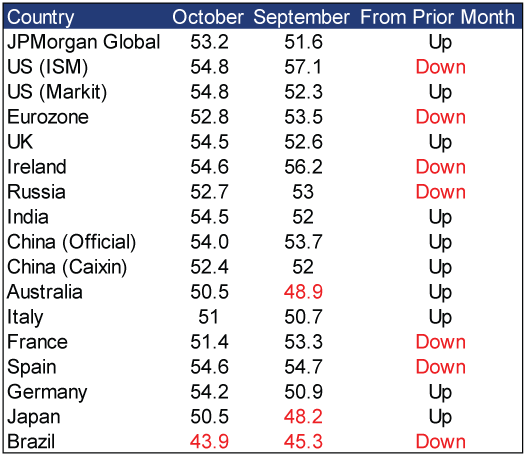

First, let's look at manufacturing PMIs. Here is a big table. Red numbers indicate contractionary readings. (Exhibit 1)

Exhibit 1: A Large Manufacturing PMI Table

Source: Markit, Institute for Supply Management, FactSet and the National Bureau of Statistics of China as of 11/4/2016. The JPMorgan Global Manufacturing PMI covers more than 30 countries, accounting for an estimated 90% of global manufacturing output. The ASEAN Manufacturing PMI covers Indonesia, Malaysia, Myanmar, the Philippines, Singapore, Thailand and Vietnam, accounting for about 98% of ASEAN manufacturing.

We aren't saying all the countries here are equal, or that being in the black is a sign of broad economic strength while red is trouble. For example, Brazilian and Russian manufacturing improved in October-and more Russian businesses grew than contracted-but their oil-dependent economies are still struggling overall, thanks to the oil supply glut. On the flipside, UK manufacturing slowed from September to October, but its services-led economy doesn't rely on manufacturing to drive growth. We could go on and add color for every country listed here,[ii] but the broader point is this: Manufacturing, which has struggled for large parts of this expansion, now seems to be shifting from a minor headwind to a minor tailwind for the global economy.

A table for non-manufacturing[iii] and services PMIs looks even better. (Exhibit 2)

Exhibit 2: A Medium-Sized Non-Manufacturing/Services PMI Table

Source: FactSet, Institute for Supply Management, Markit and the National Bureau of Statistics of China, as of 11/4/2016. The JPMorgan Global Report on Services covers 15 countries, accounting for about 74% of the global service sector gross value added.

And, as a nod to our neighbors to the north,[iv]Canada's Ivey PMI-a composite[v] gauge-also rose to a solidly expansionary 59.7 from September's 58.4.

This services/non-manufacturing table has fewer entries in part due to later release dates for services PMIs, but also because most econometrics are biased toward manufacturing for historical reasons. However, the ones here are telling. For example, in the US-the world's biggest economy-more services-oriented businesses are growing than contracting. Considering services comprise the largest swath of US economic activity by far, this is a good thing. Ditto for the UK and, to a lesser extent, China. Big economies' biggest sectors reporting broad-based growth suggests the expansion is on solid footing.

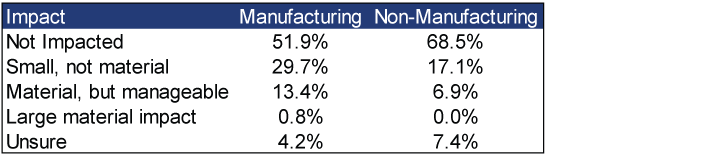

For all the handwringing and concerns-hello, IMF-these data show a healthier global economy than most appreciate. Consider a special survey question in the latest ISM US manufacturing and non-manufacturing surveys regarding the impact of Korea's Hanjin Shipping filing bankruptcy. Headlines earlier this fall warned the shipper's problems could "ruin the holiday season." Were those dire predictions right? (Exhibit 3)

Exhibit 3: Has Hanjin Hassled You?

Source: Institute for Supply Management, as of 11/3/2016.

For those of you scoring at home, less than 1% of respondents between the ISM's two surveys said this was a big issue. Or, if you're more optimistic like us, nearly 90% were A-OK (since about 12% weren't sure). And you know who else thinks business in general is solid? The businesses themselves, as evidenced by the following quotations:

"Strong economy driving steady sales." (Food, Beverage & Tobacco Products)

"Domestic business steady. Export business trending higher." (Chemical Products)

"We secured lots of new clients, and business in our division is booming." (Construction)

"Economy is becoming stabilized. All segments doing fairly well." (Finance & Insurance)

These aren't just US-based ISM surveys, either. JPMorgan's Global Services gauge is at an 11-month high while manufacturing growth is at a two-year high. This certainly doesn't mean every sector globally-let alone every business-is doing great. However, these numbers and responses are coming straight from the folks who are directly responsible for "economic growth." In our view, their input is a bit more valuable than a bunch of theorists warning that the global economy is slowing and government-led fiscal stimulus is the only solution.

PMIs aren't some magic indicator telling you exactly where the economy is (or is headed) at a given point. Nothing is. Economics and economic data are frequently more art than science. However, given PMIs from all over the world continue complementing other growthy numbers, these reality checks keep unmasking the many negative narratives out there for the false ghost stories they truly are.

[i] Heh heh.

[ii] But that would turn into a long, think tank-esque report, rather than a snappy, concise MarketMinder article that we believe you, dear reader, would prefer.

[iii] ISM's US and China's official "non-manufacturing" PMI include more than services industries. ISM, for example, also includes mining and agriculture.

[iv] We very much like Canada. And, given a trying presidential election that (mercifully) concludes next Tuesday, many other Americans seem to have taken a new liking to Canada, too!

[v] Which combines a swath of sectors, including manufacturing and services. Thus, it doesn't neatly fit in one table.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics The Tenth Question Facing Alberta2026-08-06

-

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today