Personal Wealth Management / Economics

An Equation to Shed Light on Inflation

Global central banks’ recent actions have some folks fearing hot inflation once again.

While it’s true inflation is always and everywhere a monetary phenomenon, it’s not exclusively the money supply that matters.

We issue this reminder in the wake of recent global announcements the Fed will launch QE3 with no targeted end date, coupled with some actions by their global cohorts like the Bank of Japan similarly adding liquidity. The ECB has also announced measures involving debt purchases—their new Outright Monetary Transactions program—but those will be sterilized, meaning money created will be near-simultaneously withdrawn through deposit auctions. In the US, though, at least, it’s the stated objective of the central bank to essentially force more cash onto the balance sheets of financial institutions. So money supply is increasing. And without a doubt, it’s also true this is one factor that could drive quicker inflation in the period ahead. But it doesn’t necessitate it, nor does it tell you when, or even if, hot inflation will come to pass.

In the early 20th century, famed economist Irving Fisher (no relation to Fisher Investments’ CEO, Ken Fisher) derived a theoretical equation for use in thinking about inflation drivers. It is: MV=PQ. “M” is money supply, the factor directly influenced by the Fed. “V” is velocity of money—or how quickly money flows throughout the economy via lending, spending and other transactional means. “P” is the general level of prices, and “Q” is economic output.

Now, in recent years “M”—if defined as the monetary base, or M0—has increased globally quite a bit via the various forms of accommodative policy central banks have employed. In the US, that’s largely 2008-2009’s QE1, 2010’s QE2 and the recently announced QE3.

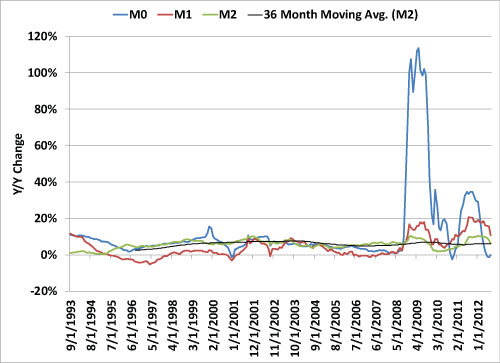

Yet, as shown in Exhibit 1, this increase in the monetary base (blue line) hasn’t been reflected in hot inflation. Why is best explained by the V—or lack thereof.

Exhibit 1: US Monetary Base (M0 Money Supply) vs. M1 and M2

Source: Federal Reserve Bank of St. Louis as of 08/31/2012. Year-over-year percentage change.

As shown, the increased monetary base simply isn’t translating into a vastly increased amount of money moving through the economy, as measured by broader monetary indicators like M1 and M2. Simply, bank lending, while it’s increased in recent quarters, hasn’t exactly spiked upward. There are likely many factors at work behind this: Slow loan demand growth, bank bashing, legislative change, shifting regulatory winds and a much tighter set of lending standards each likely play a role. But a major force (and a frequent omission in articles discussing expectations of hot inflation ahead) is the Fed’s four-year old policy of paying interest on excess reserves—a policy born while the Fed was launching QE1.

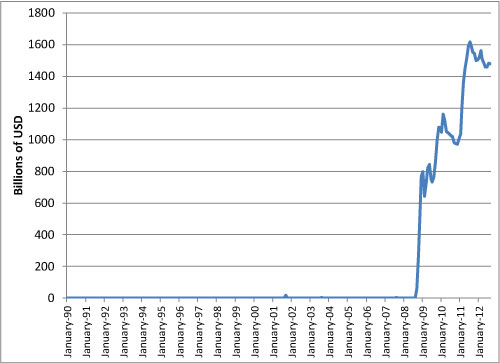

This policy pays banks (currently 0.25%) to park excess reserves at the Fed—a relatively dramatic shift from the pre-2008 period when banks had to do something to earn return on reserves held above and beyond regulatory requirements. That something often amounted to lending—taking on risk. The Fed’s interest paid on excess reserves, by contrast, may be low yielding, but it’s credit risk-free. And as Exhibit 2 shows, banks’ excess reserves on deposit at the Fed surged when the policy was implemented in October 2008.

Exhibit 2: Banks’ Excess Reserves on Deposit at the Fed

Source: Federal Reserve Bank of St. Louis as of 08/31/2012.

So simply put, the lion’s share of the money created in recent years currently sits on deposit at the Fed, meaning the connection between the money supply increases and resulting inflation isn’t very strong currently.

But it isn’t just velocity that’s dampened the inflationary impact of QE. Another way to think about inflationary factors is more money chasing a constrained amount of goods and services. Damp velocity implies the money isn’t chasing much. Yet the economy also still has considerable slack to work off, implying the amount of goods and services isn’t very constrained today. While industrial capacity has risen since the recession’s end, it was still 78.2% in August—below the last 40 years’ average 80.2% rate and well below points seen in the inflationary 1970s. Moreover, labor markets (as is widely known) are far from constrained, considering low labor force participation rates and elevated unemployment.

Now, don’t get us wrong: There is risk of hotter inflation ahead. A key factor will be how quickly the Fed reins in the liquidity it’s added when the time comes, which the bank’s history suggests won’t be executed perfectly. Could they get it right here? Sure, but it seems more apropos to ask: Do they get it mostly right or wrong from a timing and magnitude perspective?

But that doesn’t seem a question for the here and now, and given the Fed isn’t a gameable, market-oriented institution, we’ll not speculate about choices they might make. Today, inflation metrics like CPI, core CPI and the PCE price index haven’t shown much inflation. Bond yields, like near record-low 10-year Treasury rates, aren’t reflecting higher inflation ahead either.

Inflation is, of course, a key factor to watch in the period ahead. And the factors we note above—capacity utilization rates, loan growth, central bank policy (including those beyond simple monetary policy like interest on excess reserves rates) and more—are a good place to start.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today