Personal Wealth Management /

Another Fruitful Earnings Season

Publically traded companies' earnings and revenues continue to rise.

Q2 earnings season is nearing the finish line, and it's a good one: Aggregate S&P 500 earnings and revenues accelerated, and in a fresh twist, headlines actually noticed. And didn't respond with a chorus of yah-buts. Publicly traded firms are making money, confidence is growing, and with the global economy on an upswing, there should be plenty more in store-powerful bull market fuel.

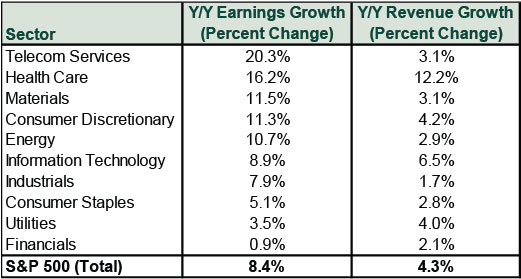

With 446 companies reporting as of August 8, aggregate S&P 500 Q2 earnings per share are up 8.4% y/y-the 19th straight quarter of growth-and revenues are up 4.3% y/y.[i]Growth is broad-based, with all 10 sectors in the black and half up double-digits. (Exhibit 1) Financials' earnings were just barely positive, largely due to yet more legal and regulatory costs, but some perspective is in order. According to analysts, Q2 bank profits totaled $40.24 billion-the second highest on record and only 0.3% below the top spot-and growth is expected to snap back bigtime in Q3. This, combined with healthy revenue growth, does not paint a picture of a beleaguered banking industry.

Exhibit 1: Q2 2014 Earnings and Revenue Growth by Sector

Source: FactSet Earnings Insight, as of 08/08/2014.

Another new high isn't exactly earthshattering. But Q2 earnings did come with a twist. Once again, the majority beat estimates-73%, above the long-term average. But "beating estimates" this time doesn't mean what it did in recent quarters. For the past few years, analysts have ratcheted down their estimates in the run-up to earnings season, setting the bar lower and lower-and setting up an easy beat. This time, analysts lowered their forecasts a bit three to nine months before firms started reporting, but during the home stretch, they largely held steady. The bar was higher, and the majority still topped it! That's not to talk down earnings growth in prior quarters, rather to show where sentiment is these days. Professional forecasters have more faith in companies' ability to perform and profit-budding optimism, if you will. But it also doesn't appear their expectations are getting out of hand-it's a rational optimism.

Warming sentiment is apparent in the media, too-a barometer for mass investor sentiment. In past quarters, if headlines acknowledged earnings growth, they cast it in a negative light, saying cost cutting was the sole driver-baffling, in our view, considering revenues rose in all but two quarters since Q4 2009.[ii] Now, revenue growth is getting more ink ... err, pixels ... and pundits are rather optimistic about the future. But in a rather odd way. If you read most of the coverage, you'd never know revenues were up five straight quarters and at all-time highs. You'd think corporate America was mired in a sales slump, and revenues just finally started driving earnings. Headlines might have a sunnier outlook, but most still don't realize just how strong firms have been in recent quarters.

This is sort of a running theme these days. When China's HSBC Manufacturing index moved back into expansionary territory in June for the first time since December, pundits acted as if China was emerging from a recession. Even though the broader economy as measured by GDP never grew slower than 7%, gangbusters growth by most standards. When UK GDP got back to pre-crisis highs last month, headlines (bizarrely) declared the end of the recession. Even though the UK had achieved six straight quarters of growth! The media take on banks' performance is another place to see sentiment evolving. Just 10 months ago headlines accused banks of unjustifiable "profit padding" when they cut bad loan reserves. Now, the same action brings statements that, "The bad is starting to bottom out, the good is starting to gain momentum." Sentiment might be brightening now, but it is improving off a very low base. That tells you optimism has quite a bit of room to grow before it becomes anywhere near the euphoria that typifies bull market peaks.

[i] FactSet Earnings Insight, as of 08/07/2014.

[ii] FactSet, as of 01/10/2014. S&P 500 year-over-year revenues per share. Two quarters of decline were Q3 2012 (-0.54%) and Q1 2013 (-0.21%).

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 11 - May 152026-05-18

-

Behavioral Finance Investing Lessons From the Indianapolis Motor Speedway2026-05-18

-

Expert Commentary 3 Things You Need to Know This Week | Global Inflation, Fed Minutes, US Sentiment2026-05-18

-

In The News Around the World in Tax Policy Talk2026-05-15

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today