Personal Wealth Management / Market Analysis

Assessing the Iran Deal’s Investment Impact

The Iran nuclear deal doesn't diminish Energy stocks' many headwinds.

Tuesday, the US and five other world powers reached a nuclear agreement with Iran: If Iran constrains its nuclear program as agreed, the six will lift economic sanctions. The agreement, which now goes to Congress for review and approval, has sparked passionate reactions-many centered on regional geopolitical and military what-ifs. Those are valid points to weigh sociologically, but for investors, they aren't really the right considerations. Markets care most about the conditions affecting the private sector over the next 12-18 months or so, and it is highly unlikely anything related to this deal snowballs into a major global conflict within this window. Trying to look much further out is sheer speculation, which markets don't discount. So the right question, in the here and now, is: What are an Iran deal's foreseeable implications for corporate profits and the global economy? Some already debate the impact on oil prices and the Energy sector. Should the deal go through-i.e., Iran pass nuclear inspections, sanctions ease and Iran fully returns to global oil markets-crude oil supply would probably increase. But those are a lot of ifs, and any assessments of the impact are pure speculation at this point. Regardless of whether Iran puts an additional weight on oil prices, though, Energy stocks still face many headwinds, and in our view, better investment opportunities exist elsewhere.

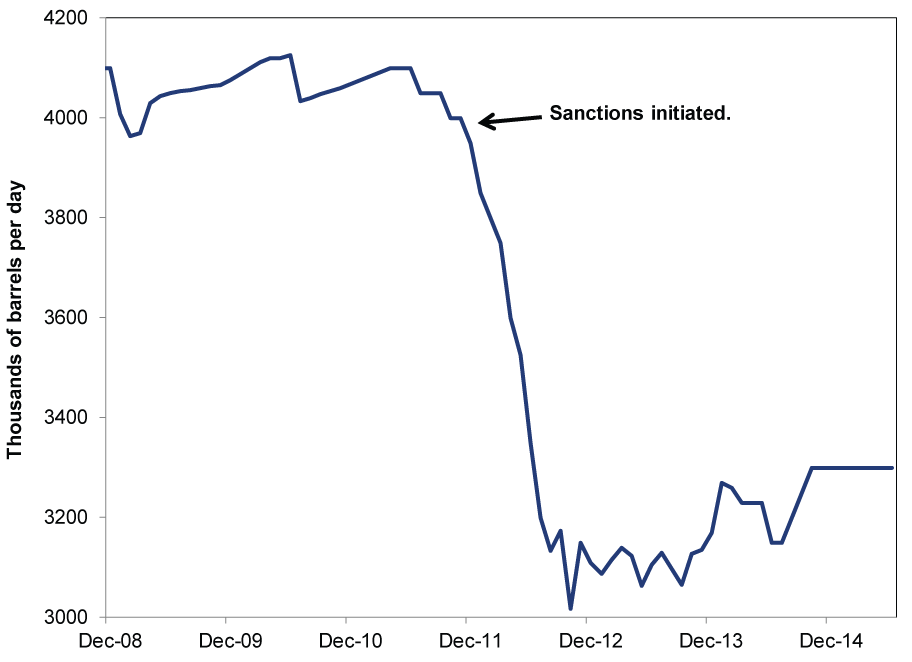

Should Iranian oil exports come back online, they would add to an already oversupplied global market-the question is how much and when. Iran currently exports about 1.4 million barrels of oil per day (mbpd), compared to 2.6 mbpd before sanctions were imposed in November 2011. Estimates for a post-sanctions export jump range from 200,000 to 500,000, though Iranian oil minister Bijan Namdar Zanganeh said his country could increase exports by 500,000 barrels a day (bpd) once sanctions are lifted and add double that in the following six months. However, 500,000 bpd equals just 0.6% of total world production. For comparison, the US's Bakken shale alone produces about 1.2 mbpd, and the Eagle Ford shale churns out about 1.5 mbpd. Iran's forecast may be overly optimistic, too, as its ability to ramp up production remains to be seen. After getting cut off from export markets, Iran slowed production by 1 mbpd, and it's unclear when old wells will be ready to produce again. (Exhibit 1) They have every incentive to move quickly and goose exports as much as possible, given how sanctions have hurt Iran's economy, but sometimes technology trumps will.

Exhibit 1: Iran Oil Production

Source: FactSet and EIA, as of 7/16/2015. Iran Crude Oil Production. From 12/31/2008 - 3/31/2015. H/T Brad Rotolo.

In short, Iran would add weight on prices, albeit a small one. We wouldn't expect crude to plunge anew, but this development is another reason for prices to continue bouncing around today's low levels.

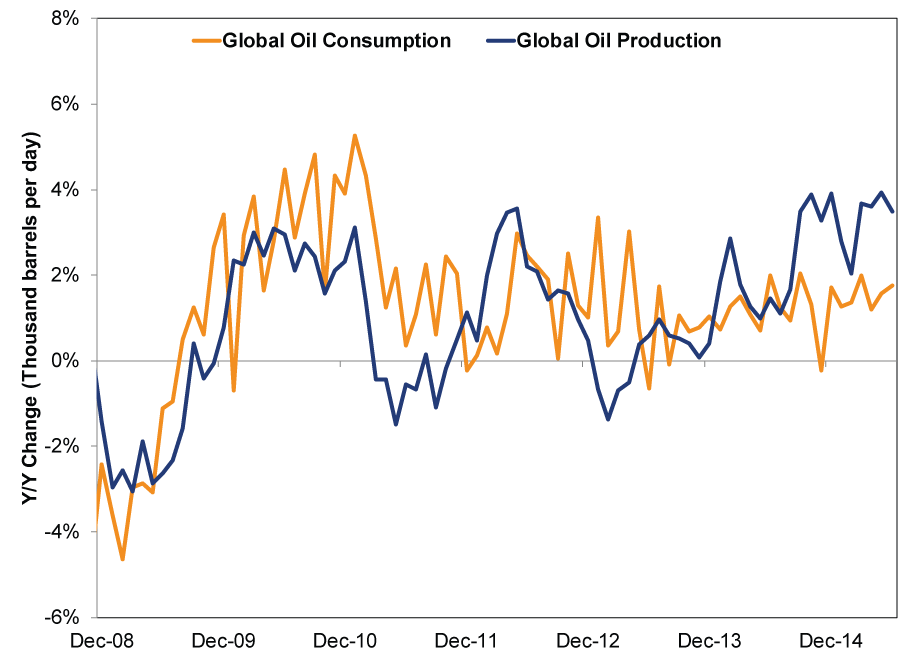

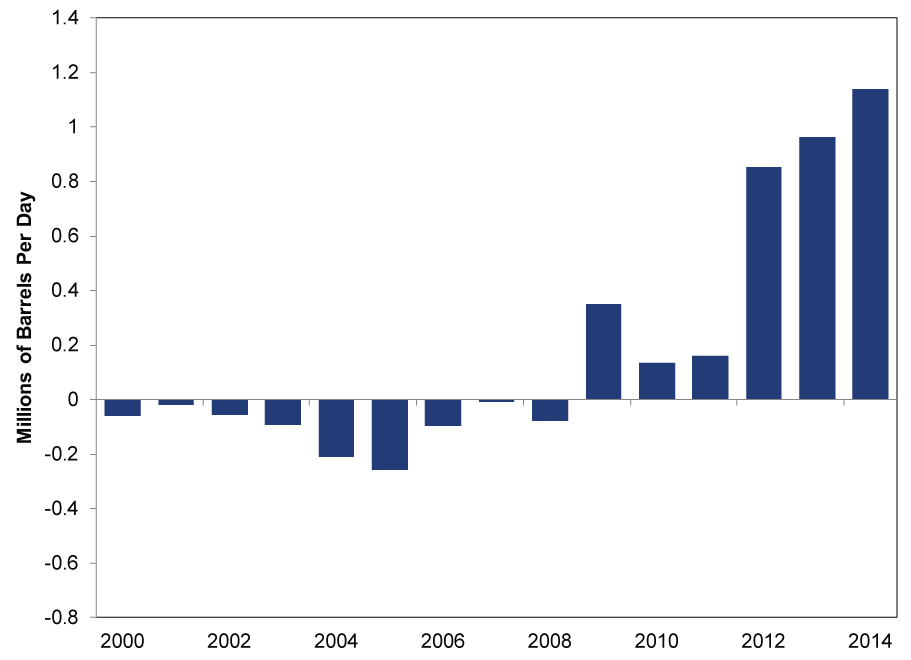

Even with Iran partially absent from the global stage, price pressures abound. Global supply growth has exceeded demand growth since September 2014. (Exhibit 2) US production growth has soared in recent years. (Exhibit 3)

Exhibit 2: Monthly Global Oil Consumption vs. Production, Year-Over-Year Change

Source: FactSet and EIA, as of 7/15/2015. International Oil Consumption and International Crude Oil Production in thousand barrels per day. From 12/31/2008 - 6/30/2015.

Exhibit 3: Average Monthly US Oil Production, Year-Over-Year Change

Source: EIA, as of 7/15/15. US oil production, 1/1/2000 - 12/31/2014.

Since energy firms' earnings and revenues tend to be highly price-not volume-sensitive, low prices have whacked both lately. S&P 500 Energy earnings and revenues fell -56.6% y/y and -34.6% y/y, respectively, the latest in a long string of red ink.[i] Even if prices stay steady, revenues likely keep falling as producers' hedges expire. Many used delivery contracts at higher prices or derivatives contracts to hedge short-term risk-common practice since commodity markets can be pretty darn volatile-partially insulating them as oil fell last year. Those arrangements' expiration is now forcing firms to bear the full brunt of lower prices.

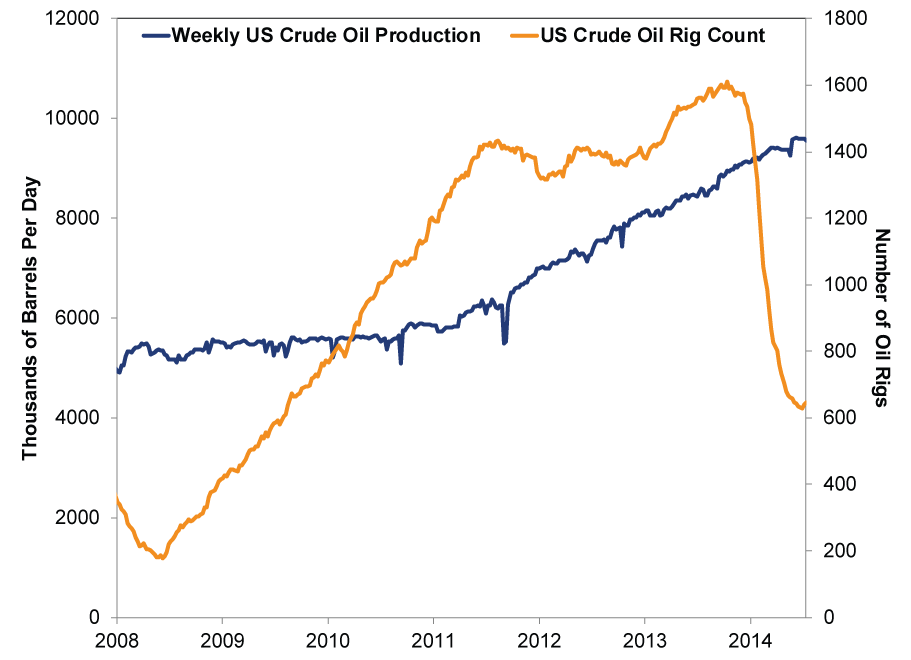

Despite those headwinds, production shows no signs of slowing. Since oil extraction requires a big upfront investment and prices are still around "breakeven" for many producers, it makes sense to keep extracting-some return on investment is better than none, especially as producers find different ways to boost efficiency. You can see this in the relationship between oil rig count and production. (Exhibit 4) Even as rig count tumbled in recent months, production kept rising (albeit with a couple hiccups). Firms have been doing more with less.

Exhibit 4: Rig Count and Production

Source: FactSet, as of 7/15/2015. Weekly Field Oil Production (thousands of barrels/day) and Baker Hughes Weekly Oil Rig Count, 12/31/2008 - 7/10/2015.

US shale drillers have also found clever ways to get more bang for their buck: consider the "fracklog" and "refracking." Many drillers have started wells but not yet fracked them-a big backlog (thus, "fracklog") of oil they can tap as soon as it's cost-effective. An uptick in price could prompt producers to tap their fracklogs, quickly boosting supply-and then probably sending prices back down. "Refracking"-injecting more water and sand into an older shale oil well-is a cheap, quick way to both extend shale fields' lifespan and goose production without the huge upfront costs associated with new wells. Though still in its early stages, the potential here is significant. These and other low-cost techniques probably keep supply elevated over the foreseeable future-pressuring oil prices.

OPEC hasn't cut production either. While there is some chatter about an emergency OPEC meeting to discuss additional Iranian oil potentially hitting the market, it's worth considering many members have strong domestic reasons to continue pumping at high volume, just like Iran does. Iraq, Venezuela and Libya need the cash. Saudi Arabia prioritizes maintaining its market share. All these factors drag down oil prices, which Iran probably contributes to once it comes back online.

For investors trying to measure the Iran's impact on oil, we suggest looking at the bigger picture. Plenty of pre-existing factors are keeping prices down, whether or not Iran increases its oil output-something to keep in mind for those who believe the Energy sector will bounce back soon.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis A Forward-Looking Lesson One Year After Liberation Day2026-04-02

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-01

-

Market Analysis Countertrends and Corrections: Banks in 2026’s Early Selloff2026-04-01

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today