Personal Wealth Management / Market Analysis

Autumn Statement Ends Age of Alleged Austerity

Pundits greeted the UK Autumn Statement like it signals a radical shift in plans, but it actually extends long running trends.

It is truly odd how the media approaches the issue of "austerity." The latest episode follows UK Chancellor of the Exchequer George Osborne's Autumn Statement and Spending Review, published last week. Here is how the Oxford Dictionary defines "Austerity":

"Austerity (noun)

Sternness or severity of manner or attitude

Extreme plainness and simplicity of style or appearance

Conditions characterized by severity, sternness or asceticism

Difficult economic conditions created by government measures to reduce a budget deficit, especially by reducing public expenditure."

We, as folks most interested in the economy and markets, focus on definition number four.

Osborne, UK Chancellor since 2010, has largely been seen as wielding a budget-cutting axe, slashing spending and, according to the media, bringing those "difficult economic conditions" the Oxford definition notes. But Wednesday, the media looked at an announcement we'd basically summarize as "more of the same" and claimed Osborne's proposals heralded the end of the "Age of Austerity." This brings austerity theories full circle: You see, the UK's budget deficit is indeed smaller. But the UK never cut spending, and rather than those "difficult economic conditions," the British economy has been among the developed world's growth-rate leaders for years. The disconnect between reality and media sentiment here is one lesson, but in our view, this is a good reminder for investors that buying into common narratives without digging into data is a dangerous practice.

As always, there are a slew of minor proposals embedded in the Autumn Statement. Here is a fairly comprehensive run-down of them, and here is another. Or you can click here for the actual version and flip to page 112. We won't bore you by adding another list, but it is worth noting why folks think this is the end of austerity. For one, Osborne backtracked on plans to cut £4.4 billion worth of tax credits for low-income households, an unsurprising U-turn given the House of Lords took the unusual step of voting against the measure recently. He also won't cut from the police budget, another widely watched decision, given the recent Paris terror attacks. When you sum the whole statement, Osborne's new plan would spend £128 billion more over the next five years than March's budget on public services and £12 billion on infrastructure.

So, yes, the Autumn Statement's proposals would increase spending versus the current Budget. But this isn't a total reversal of course. The British government, you see, has increased its spending every year that Osborne has served as Chancellor.

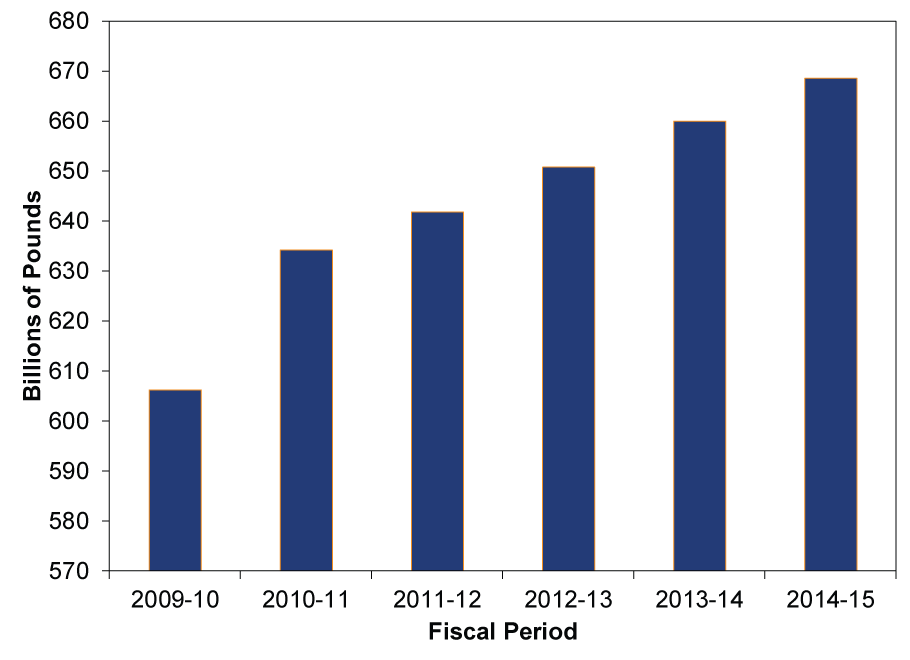

Exhibit 1: UK Central Government Spending

Source: Her Majesty's Treasury.[i]

Now then, it does seem the coalition cut the growth rate of spending, but to save you the trouble of scrolling back to the top of this article, definition #4 of "austerity" is:

"Difficult economic conditions created by government measures to reduce a budget deficit, especially by reducing public expenditure."

"Austerity" in Britain hasn't matched definition #4 at pretty much any point. Reducing is the keyword in that public expenditure phrase, and nothing in Exhibit 1 appears to be reducing.

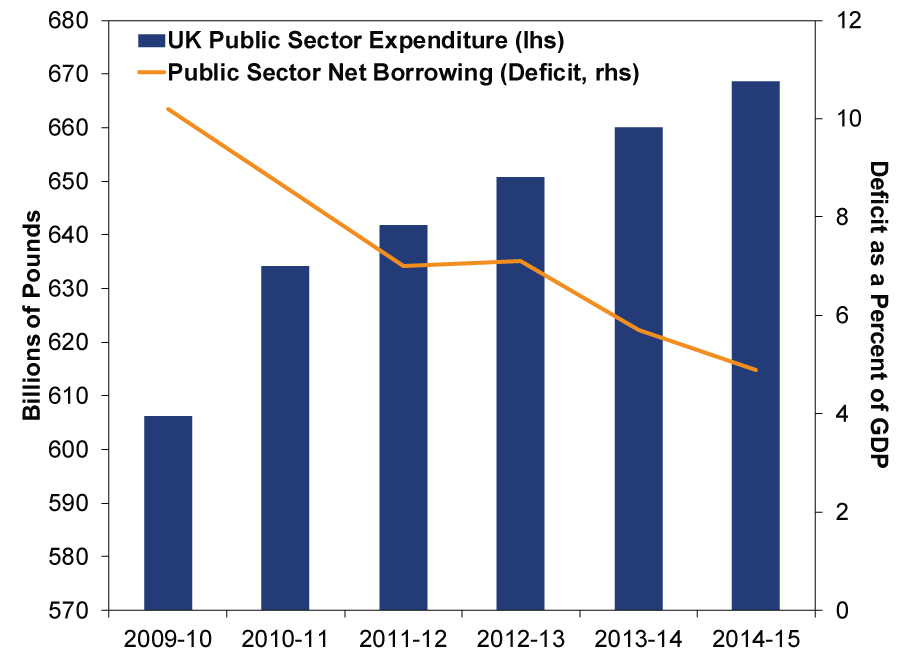

What did reduce, though, was the budget deficit. (Exhibit 2)

Exhibit 2: UK Deficit and Public Sector Expenditure

Source: Her Majesty's Treasury.

Perhaps that raises the question of how the reduced deficits have been achieved. It is partly through tax hikes, so we guess you could call that austere. But if you did call that austerity, then there is no real way to claim this is over. The Autumn Statement includes proposals that would increase tax revenue by about £56 billion by 2021, including a payroll tax on firms with more than £3 million in payrolls designed to fund increased apprenticeship and a new transfer tax on residential rental properties, expected to bring a total of just under £4 billion in new revenue over the next five years.

But the major deficit-reducing factor is growth. Now, much has been made of the Office of Budget Responsibility revising its economic growth outlook upward over the next few years, resulting in £27 billion in newfound tax revenue. Yet realistically, the upward revision reflects a stubborn fact, one further calling into question the application of the term "austerity" to Britain: The UK economy hasn't been experiencing particularly "difficult economic conditions."

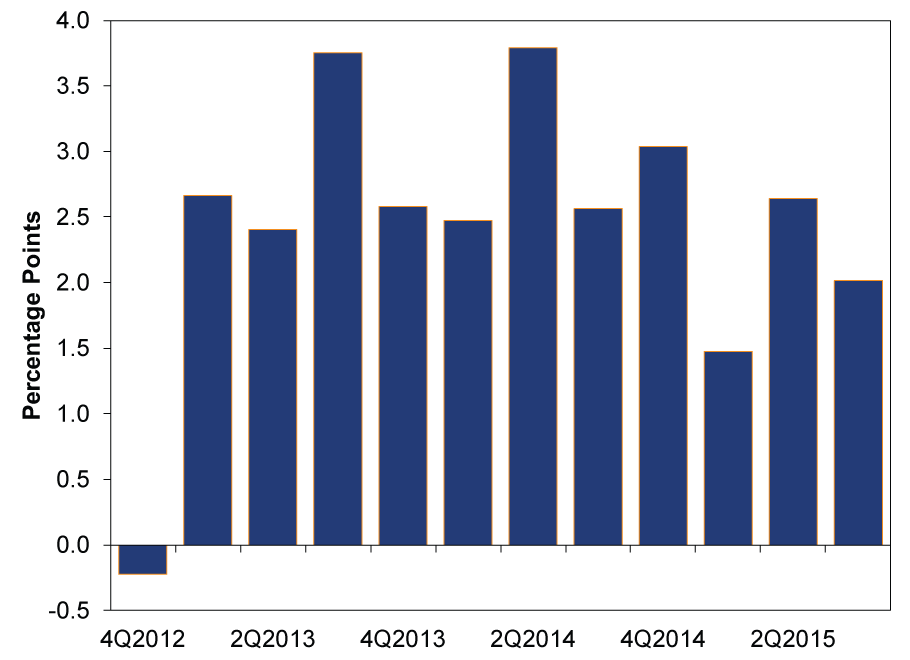

Since the end of 2012 (when the Bank of England ceased its quantitative easing program), UK GDP growth has been at the forefront of the developed world. (Exhibit 3)

Exhibit 3: UK Annualized GDP Growth During the Age of Alleged Austerity

Source: FactSet, as of 11/27/2015.

And this growth has been underpinned by strong domestic demand-and Q3 2015's GDP report echoes the point. While headline growth slowed to 0.5% q/q (2.0% annualized), this doesn't indicate the UK economy weakened. Household spending rose 0.8% q/q (3.4% annualized), adding 0.5 percentage point to quarterly growth (2.0% annualized).

The big drag behind the slowdown isn't even negative. Net trade (exports minus imports) detracted a record 1.5 percentage points from quarterly growth (5.7 percentage points annualized). And this wasn't because exports cratered-they grew 0.9% q/q. Imports caused the drag by surging 5.5% q/q. British consumers and businesses gobbling up imports at a record clip does not exactly signify a weakening economy. It suggests the opposite. That GDP tallies rising imports as a negative says more about how detached econometrics are from the actual economy than anything else.

So if you are keeping score at home, the UK economy has grown nicely, which doesn't seem like "difficult economic conditions." Government spending, too, is up-so whatever the economy did, it wasn't caused by "reducing public expenditure" to bring down the budget deficit. By definition, then, the "age of austerity" never existed, unless we are talking about Osborne's sartorial choices.[ii] The Autumn Statement is basically a call for more of the same, despite the punditry claiming it is a substantial shift. So perhaps pundits' allegations of austerity will end, but little else. To us, this episode is just another reminder that narratives are never substitutes for facts, data and evidence. Media is often both a reflection of and the originator of sentiment trends. To invest successfully requires coldly analyzing these trends and comparing them to reality.

[i] Total Managed Expenditure (TME, spending plus depreciation and net investment) did dip slightly in one year, but this was entirely due to an accounting change involving the Royal Mail's pension. Which speaks to why we are showing you spending and not TME.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 9 - March 132026-03-16

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today