Personal Wealth Management / Economics

Balanced Budgets and a Surplus of Sociology

The UK government's plans to pass a balanced-budget rule are sociologically sweeping, but their economic and market-moving scope appears limited.

Goodbye to budget deficits! George Osborne, the UK Chancellor of the Exchequer, has vowed to outlaw UK budget deficits during economic expansions, calling this a positive step toward reducing the UK's growing debt and ensuring fiscal responsibility. Sounds sensible to many, we're sure! However, government deficits and debt are not the economic scourge some believe, and a balanced budget rule isn't an automatic positive. It could introduce negatives downstream and, if a rule had teeth, it could be the sort of extreme legislation stocks might not like. On the bright side, Parliamentary quirks and gridlock mean a strict rule likely won't come to pass.

Osborne's exact proposal, revealed at his annual speech to financial bigwigs, was to "entrench a new settlement" whereby "in normal times, governments to the left as well as to the right should run a budget surplus to bear down on debt and prepare for an uncertain future. In the Budget, we will bring forward this strong new fiscal framework to entrench this permanent commitment to that surplus." In this context, "normal" most often means a growing economy, and "abnormal" a recession. The Office for Budget Responsibility (OBR, the UK's Congressional Budget Office for you yanks) would be Ye Olde Official Arbiter of Abnormality. In principle, then, the proposal would require the UK to run a balanced budget most of the time-at least, as far as we can tell from Osborne's speech. The specifics won't be out until July 8, when Osborne releases the summer Budget.

This issue is mostly sociological. As several commentators have noted, a Parliamentary vote for perma-surplus would make the Labour Party's traditional agenda logistically difficult. An election manifesto resembling this year's would attract a chorus of "yah, but what about the balanced budget rule?" (We reckon the answer would be "we'll amend it," but anyway.) Scoring points with voters is probably another goal, considering deficits have been a hot-button issue in the UK for years. After the global recession, UK budget deficits soared to over 10% of GDP, the highest in decades. As in America, this spike in deficits led to a great deal of British handwringing. It was one of the central campaign issues in 2010, when Labour and the Conservatives offered voters dueling deficit reduction plans. When the Conservatives and Liberal Democrats emerged from that contest with a coalition government, fiscal responsibility (deficit and debt reduction) was their government's central tenet.

When the Coalition enacted their "austerity" plan, some celebrated it as fiscal sanity, and others derided it as draconian spending cuts and tax hikes the economy couldn't handle. And indeed, growth wobbled after they hiked the VAT in 2011. Yet the spending "cuts" were largely reductions in future spending growth, not actual spending reductions. And unsurprisingly, the deficit stubbornly remained above the Coalition's targets for years thereafter, costing them some support. As some were quick to point out in the 2015 election, the Coalition added more to debt in five years than the preceding government did in 13.[i] We largely view Osborne's plan to enshrine balanced budgets (with that "abnormal" loophole) as the Conservatives attempting to show supporters they mean business with their new (teensy) majority.

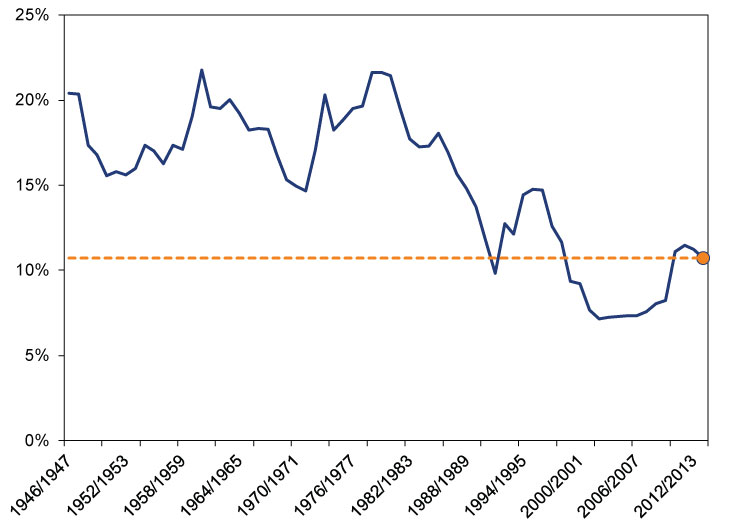

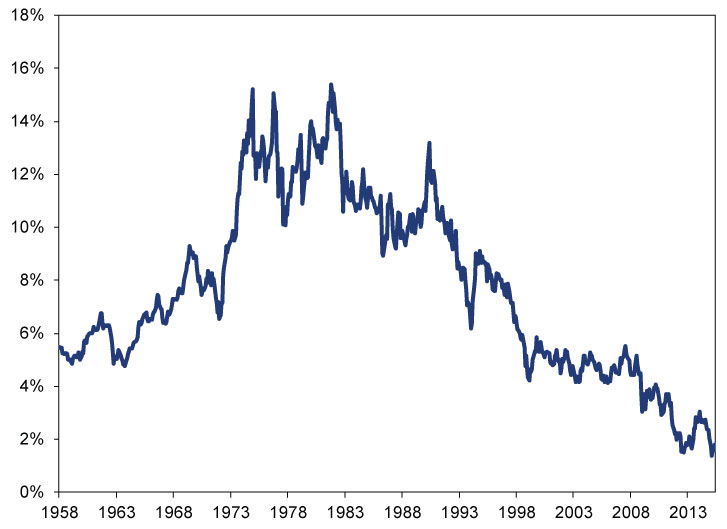

But for all their societal unpopularity, deficits aren't inherently an economic scourge. They aren't automatically problematic when they exceed some arbitrary share of GDP. They are problematic when the government can't finance its spending or debt. That hasn't remotely been the case in Britain at any point in recent years, nor is it now. UK debt interest payments as a share of tax revenue are quite low by historical standards, and UK 10-year bond rates are presently near their lowest levels in more than half a century. (Exhibits 1 and 2) This is not how yields look when a nation's solvency is in question. (Just ask Greece.)

Exhibit 1: UK Central Government Interest Payments as a Share of Tax Revenue

Source: Office for National Statistics, as of 6/16/2015. Fiscal years 1946/1947 - 2013/2014.

Exhibit 2: UK 10-Year Gilt Yields

Source: Global Financial Data, Inc., as of 6/16/2015.

If investors thought UK debt was too high and needed to fall, or else, we reckon they wouldn't require a smaller premium to own UK bonds than they did in the 1980s, 1990s or 2000s, when debt was much lower. That, coupled with low debt service costs, is a good sign debt reduction isn't a burning need.

Beyond being unnecessary, a balanced budget rule could have negative unintended consequences. If the UK needs to fund a war, deficit spending may be prudent. Such borrowing for the Napoleonic and Crimean Wars in the 19th century did not break the Empire or quash the Industrial Revolution. But also, what if they need to fund a major public works project that would unlock a huge economic return?[ii] What if they need fiscal stimulus in a downturn? While there is a recession loophole (remember "abnormal" times?), the OBR may erroneously declare times normal when they are actually quite abnormal! National statistics agencies and budget watchdogs tend not to officially recognize recessions until they are well underway-or even over. By the time the OBR decides deficits are justified, the government may have missed an opportunity to help cushion a downturn. Heck, a balanced budget rule could actually require the opposite, forcing the government to raise taxes or slash spending to balance the budget, even when it might be the worst possible timing. (Exhibit A being Japan's sales tax hike last year, which choked a nascent recovery and caused the country's third recession since 2009.)

On the bright side, none of those consequences seem likely to become reality. The Conservatives have only a 12-seat majority in the House of Commons, and some Conservative MPs-especially those who recently won seats in traditional Labour strongholds-might not go along with this for fear of alienating voters with the threat of tax hikes and benefits cuts. Ramming this through could take significant political capital-capital they'll need for other, more contentious debates like EU membership and devolution. Even if it does go through, the rule is redundant and nonbinding. Based on all available public comments and leaks, Osborne isn't proposing a statutory deficit limit. It's a political requirement that says, "run a surplus, get political cover for a deficit, or face a confidence vote." But every Budget already requires majority Parliamentary approval-yet another sign Osborne's plan is mere politicking. We suspect this would just add another layer of debate to the annual Budget spectacle.[iii]

History shows just how near-totally feckless this rule would be. In 1997, then Chancellor of the Exchequer Gordon Brown introduced the "Golden Rule", which stipulated the government can only borrow to invest, not to spend.[iv] Its sibling, the "Sustainable Investment Rule," pledged to hold net debt-to-GDP at a "stable and prudent level" over the course of an economic cycle. Parliament passed these via 1998's "Code for Fiscal Stability." But they were always just goals, with no penalties for a miss, just like the rule Osborne envisions today. And a year after Brown took over as Prime Minister in 2007, his "Golden Rule" met the financial crisis. It lost and was abandoned in 2009, bringing about the very situation Osborne now cites. An "abnormal" time is responsible for the deficits seen in recent years-so how would Osborne's change the current situation?

All in all, this rule is a ploy that carries more negative aspects than positive. But the good news is it isn't likely to pass.

[i] This is also a function of math (compound growth), not necessarily government policy. And it is somewhat cherry-picked. Public sector net borrowing under the Coalition exceeded net borrowing under the Labour governments of 1997 - 2010. However, net debt in pounds sterling and as a percentage of GDP rose more in the Blair/Brown years than under the Coalition.

[ii] Yes, we are aware that this could in theory be funded privately, but that is not how the UK operates and we are realists.

[iii] Other questions come to mind, like, what happens if tax revenues come in below forecast, and a projected surplus turns to deficit even if spending meets the target? Perhaps that would trigger a confidence motion?

[iv] Sound like semantics to anyone? Anyone?

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

-

Market Analysis The Golden Paradox2026-03-24

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today