Personal Wealth Management /

Book Review: The Sarbanes-Oxley Debacle

A decade after SarbOx became law, a look back seems apt.

This year, the Sarbanes-Oxley Act of 2002 turns 10. With the passage of this nice round number of years, I thought perhaps a retrospective was in order and set out to find books both critical and supportive of the law.

Yet my trips to Amazon.com and Portland, Oregon’s legendary Powell’s Books turned up exactly zero books extolling the law’s wide-ranging economic benefits. Critiques and lengthy preparation manuals abound, however. If history is, as is often said, written by the victors, the pro-SarbOx vacuum is rather damning. One major critique, Henry N. Butler’s and Larry E. Ribstein’s 2006 study, The Sarbanes-Oxley Debacle, encapsulates most major SarbOx objections in one volume. Ultimately, Butler and Ribstein come to the conclusion some small amount of fraud is regrettable but unfortunately simply unavoidable—however, that doesn’t spell doom for markets as they are capable of pricing stocks for that risk over time. Moreover, in their view, government attempts to outright eliminate all fraud are fraught with even greater peril, relatively speaking. (Fisher Investments has long held outliers from an industry group should raise a red flag to a potential investor—and firms committing fraud often look materially different in key ways from peers. Further, a well-diversified portfolio should mitigate the risk of stock-specific trouble.)

As Butler and Ribstein note, many politicians have opined the law (also known as the Public Company Accounting Reform and Investor Protection Act) generates important benefits. Passed in the wake of the Enron/Worldcom scandals following the dot.com-led bear market, the law targeted accounting wrongdoing and wrongdoers. Through various means, the law’s major aim was stamping out Enron-style fraud—thereby boosting investor confidence in markets. In its day, this was a tremendously politically popular concept. Both parties supported the law, forms of it passed nearly unanimously in both the House and Senate, then-President Bush supported each version (at various times), ultimately selecting the more stringent Senate version. This version (re)criminalizes accounting fraud, attaching criminal liability to errors on public company balance sheets—with fines up to $5 million and 20 years in jail. SarbOx essentially equates accounting errors (not just fraud, as intent isn’t part of the law) to a violent crime.

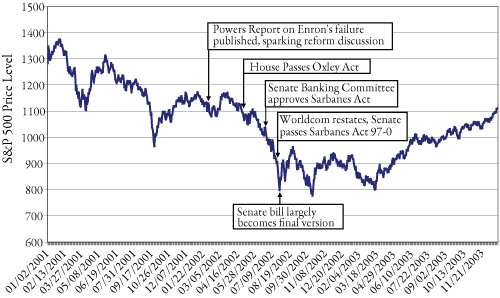

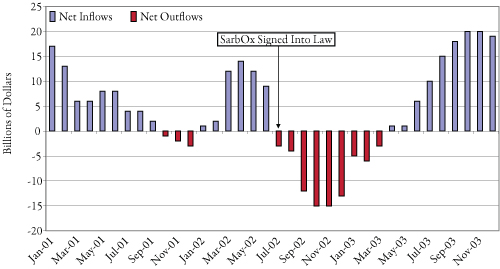

Now, determining the success of a law targeting a vague, immeasurable factor like confidence is perhaps tough. Butler and Ribstein are very skeptical it accomplished anything—which seems warranted, if you base confidence metrics on things like stock market returns (Exhibit 1) or equity mutual fund flows (Exhibit 2).

Exhibit 1: The Run-Up to SarbOx—S&P 500 Price Level

Sources: Global Financial Data as of 04/26/2012, Library of Congress, Fisher Investments Research.

Exhibit 2: A Vote of Confidence? Equity Mutual Fund Flows, 12/01/2001 – 12/31/2003

Source: Investment Company Institute, Fisher Investments Research.

Falling stock prices around the law’s passage coupled with net mutual fund redemptions doesn’t imply increased confidence to me. But maybe Congress uses another metric.

Ribstein and Butler then go on to detail many intended and unintended follies brought by SarbOx. Massively increased compliance costs, both direct and indirect in the sense law and compliance budgeting for public firms had to compensate for. Compliance with Section 404 alone is estimated to average $4.8 million in direct costs per impacted company. The SEC estimates the cost of 404 compliance averages over $1.3 million per annum for firms above $75 million in market cap. Now, the Russell 3000 Index’s smallest company’s capitalization is $130 million, so using the SEC’s figures, Section 404 costs these firms 1% of their market cap per year to comply. Nearly quadruple that if other estimates are used. This is why “crowdfunding” was a hot topic earlier this year. And it’s one reason some major firms like Facebook may have waited so long to go public. Indirect costs also accrue—Butler and Ribstein carefully document many: Attempts to erect barriers and rotations involving auditors, which means auditors are less familiar with a company’s operations; the unseen costs (Debacle cites a figure exceeding $1 trillion by 2006) associated with capital that wasn’t raised, expansion that didn’t occur, etc. The book cites many more (quite cogently), readable even to one not steeped in legalese and not necessarily just the common critiques.

Some of Butler and Ribstein’s charges are open to questioning. For one, they speculated the law would bring a huge increase in shareholder class-action lawsuits—presumably, frivolous ones. Yet a decade later, it’s tough to find evidence actually suggesting this surge occurred. Data compiled by Stanford University’s Law School would suggest it hasn’t. Moreover, for all the discussion of unseen costs in the book (which I’m entirely convinced exist), I’m skeptical of attempts to calculate the value. In that way, Debacle citing $1 trillion in lost economic output seems unnecessary and runs the risk of obscuring serious consideration of the broader point.

All in all, the book shows signs of the passage of time, but it’s still an excellent work fully demonstrating the political motivations behind sweeping reforms that have carried a high cost and, thus far, seemingly little reward. It was written while a legal challenge (the Free Enterprise Fund suit) was being heard in the Supreme Court, and the authors speculated then the case presented an opportunity to revise—or better, discard—SarbOx. However, the decision has proven relatively unimpactful. Moreover, there are other unintended follies not fully explored in this book: How SarbOx, through increasing CEOs’ and CFOs’ risk, likely boosted their compensation (reward); how SarbOx may have contributed to 2008’s financial panic through executives’ accounting behavior and poorly designed oversight for FASB; how audit quality, in the SarbOx-created Public Company Accounting Oversight Board’s opinion, has yet to markedly improve.

Sadly, Professor Larry Ribstein passed away in December 2011, so the Ribstein and Butler duo won’t have an opportunity to revisit and update the work. But for a powerful critique—and a mostly economically sound counterpoint to political rhetoric—Ribstein and Butler’s Debacle stands the test of time well enough to merit a read.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10 -

Market Analysis Trim Your Angst on Economic Measurement Tweaks2026-07-09

-

Politics Long-Term Forecasts and Court Verdicts: The Latest in British and French Politics2026-07-09

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-07-08

2026-07-08

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today