Personal Wealth Management / Market Analysis

Britain Doesn’t Need Balanced Growth

Recent data reinforce the notion Britain doesn't need booming heavy industry to grow.

"A triple whammy of disappointing survey news."

"The clearest indication yet that uncertainty created by the EU referendum is hurting the economy."

"Lacklustre domestic demand is being compounded by a worsening global picture."

All those quotes were unleashed Thursday, after several economic data points suggested UK growth may have slowed in recent months. People, it seems, are worried about the UK economy. But are they right to be? At first blush, you might think the answer is yes. But most metrics still point to growth, which routinely fluctuates during expansions. What's more, forward-looking indicators suggest more growth likely lies ahead. The fact sentiment remains so gloomy is a sign that even if growth slows, it would likely still exceed too-low expectations, a tailwind for stocks.

Fears that Britain's growth is unsustainably "unbalanced"-too reliant on domestic consumption and services-have been a common narrative for years now, and data released thus far in 2016 spurred them further. Q4 GDP grew 1.9% annualized (0.5% q/q), a slight uptick from Q3's 1.7% rise. That may, on its surface, seem to cut against fears of a UK slowdown, but growth was largely driven by a 2.7% annualized rise in consumer spending.[i] Meanwhile, exports fell -0.5% annualized and business investment shrank by a whopping -8.3% annualized.[ii] On a sector basis, Services and Agriculture grew, but the Construction and Industrial sectors-the focus of fears-fell. The monthly gauge of industrial production has been soft lately, falling -1.1% y/y in December after an -0.8% November slide. December also saw manufacturing fall -1.7% y/y. Markit recently published February Purchasing Managers' Indexes (PMIs) for services, manufacturing and construction, and all three slowed from January, triggering that slew of quotes we typed up front. Services fell to 52.7 from 55.6 in January, manufacturing slipped to 50.8 from January's 52.9, and construction dropped from 55.0 in January to 54.2.

But despite the handwringing, these PMIs still suggest growth. PMIs measure the percentage of firms reporting growth, so any reading over 50 suggests expansion. Now, since PMIs measure the breadth of growth, not its magnitude, you could still get contraction with a PMI above 50. If the shrinking firms' collective contraction outweighs the growing firms' collective expansion, growth may be weaker than the headline number suggests. But the flipside is also true. Also, one month of falling PMIs doesn't necessarily predict further slides or economic weakness. They bounce around quite regularly.

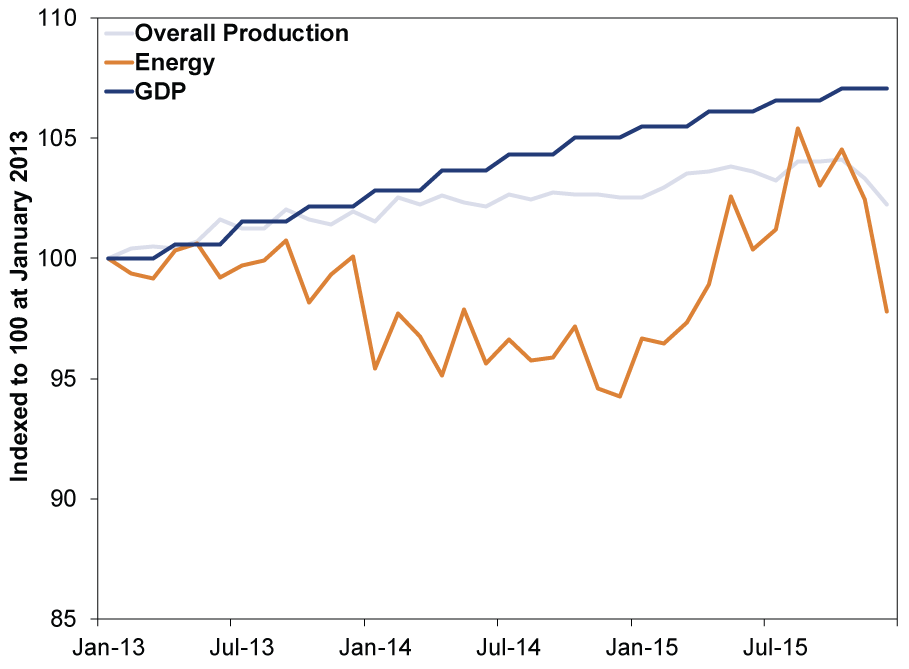

While manufacturing hasn't driven UK growth in years, its recent weakness is exacerbated by the global commodities slump. Even before oil began sliding in mid-2014, UK energy production waned, weighing on total industrial production. Energy production then surged in 2015's first half after the government enacted tax credits to promote drilling in the North Sea. But since then, oil's continued fall has quelled production, again skewing total industrial production lower. According to the UK's Office for National Statistics, investment in oil extraction fell about 20% between Q2 2014 and Q3 2015, and that is before the -2.3% q/q drop in oil extraction in Q4.[iii] Meanwhile, GDP expanded at a healthy clip throughout the period, driven by domestic consumption.

Exhibit 1: Energy's Influence on UK Industrial Production

Source: FactSet, as of 3/7/2016. UK industrial production, energy production and GDP, 1/1/2013 - 12/31/2015.

This all suggests that the allegedly unsustainable and unbalanced UK has defied these fears for quite a while. Maybe that seems like a headscratcher, but when you consider the UK's economic makeup, it isn't surprising at all. Industrial output is only 15% of UK GDP. Services-eating out, travel and accommodations, medical care, finance and consulting-is the biggest chunk at roughly 80%. If you want growth rates to be faster in one area of your economy, you should probably want it to be the vastly bigger part. In January, data continued to show consumption and services' strength. Retail sales volumes-the amount of stuff purchased, not the value-grew 5.2% y/y in January, with online sales climbing 10.4% y/y.[iv] Rising real wages should continue fueling healthy domestic consumption. January and February's services PMIs were firmly in expansion territory, as has been the case for the last few years. Money supply and bank lending have resumed rising. And The Conference Board's UK Leading Economic Index is in a persistent uptrend, suggesting that even if industrial production doesn't surge, growth will likely continue.

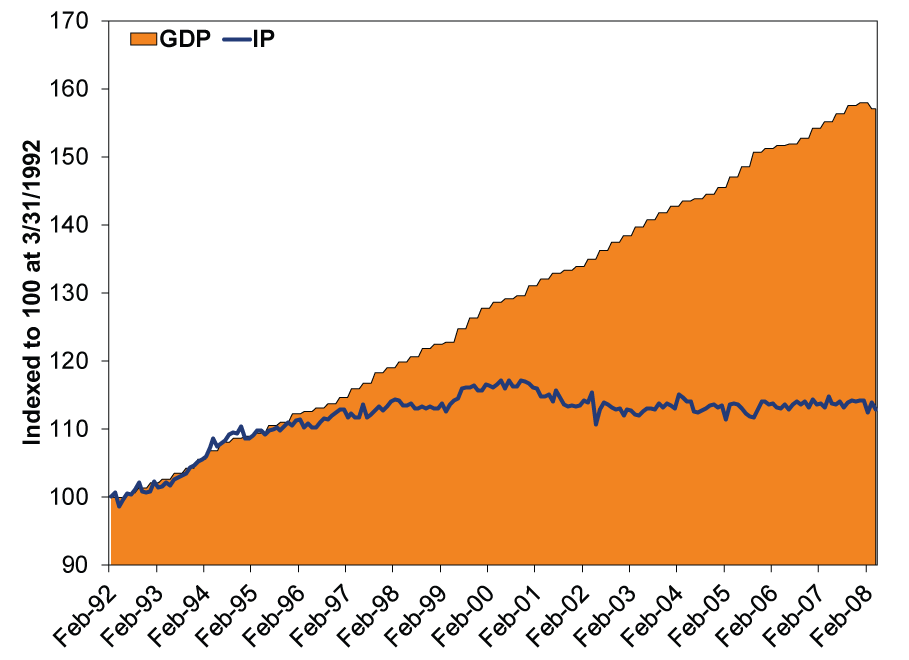

The unbalanced economy fears seem to be rooted in a misperception about what drove 2008 and the nature of the services industry in general. It seems many believe the global financial crisis, which hit Britain hard, exposed the services-and-consumption driven growth that preceded it as flimsy and debt-fueled. Trade and production are presumed to be more solid. However, this doesn't accurately pay reference to the nature of Britain's pre-crisis growth. As Exhibit 2 shows, Industrial Production was flattish-lagging GDP growth-for roughly 12 years preceding the financial crisis. No economy, no matter how balanced, is recession-proof. But 12 years of growth fueled mostly by services is pretty darn stable, in our view. And ultimately, the principal culprit ending that expansion was a supply-side financial crisis Britain imported from American policy missteps.

Exhibit 2: UK GDP and Industrial Production 1992 - 2008

Source: FactSet, as of 3/7/2016. UK GDP and Industrial Production, 3/31/1992 - 5/30/2008

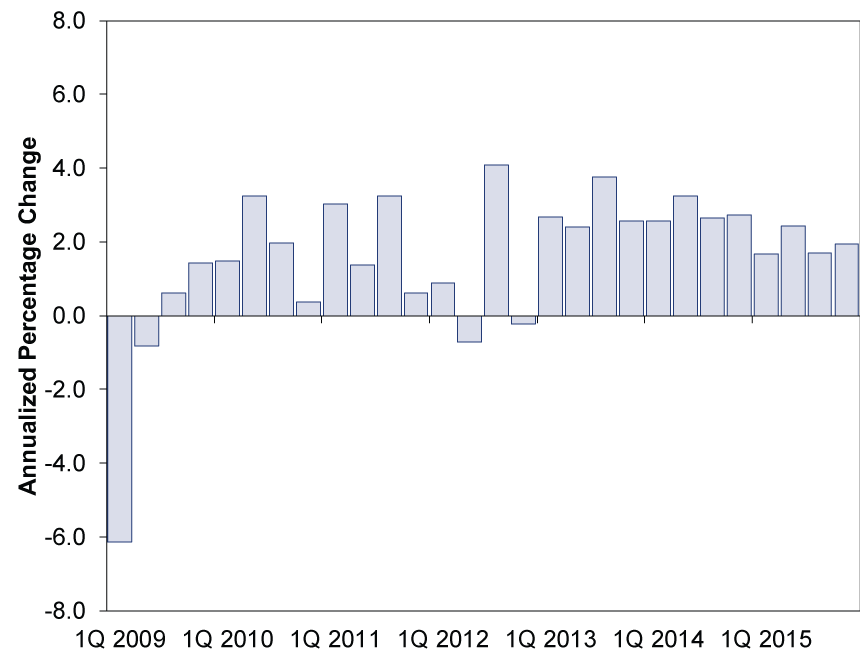

As for growth in the here-and-now, perhaps it does slow some in Q1 or Q2. But growth regularly wobbles during expansions. (See Exhibit 3)

Exhibit 3: UK GDP (Annualized Rate) 2009 - 2015

Source: FactSet, as of 3/7/2016. UK GDP annualized rate, Q1 2009 - Q4 2015

So why is the recent downtick now feared so different from all those others? Maybe it's because of stocks' volatile start to 2016. Macroeconomic fears have accompanied a number of corrections in this cycle, and this one may be no different. Or, maybe it's because Brits will vote this summer on whether to remain in the EU, and many fear a "leave" vote will be an economic shock, as trade will fall and the pound will weaken, crimping outside investment in Britain. In our view, though, this seems like a case of a narrative dominating the data, and the predictions are largely rooted in economic fallacy. There is little to no evidence growth measures in Q4 2015 and early 2016 were affected by Brexit. Heck, we didn't even know the terms of the renegotiated EU treaty or the referendum date until a couple weeks ago. To us, the preponderance of the evidence suggests the UK is in fine shape economically, not teetering unbalanced on the brink of recession.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

-

Expert Commentary US Inflation, Fed Minutes, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-06

2026-04-06 -

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03 -

Market Analysis A Forward-Looking Lesson One Year After Liberation Day2026-04-02

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today