Personal Wealth Management / Market Analysis

Britain’s Balance

The UK economy doesn't need its politicians' help.

So the first estimate of Q1 2015 UK GDP hit Tuesday, and the number was lower than most expected: 0.3% q/q (1.2% annualized). With the general election days away, British politicians used the news to rally voters (and knock the competition). Conservative Chancellor George Osborne said the UK was now at a "critical moment" and that "you can't take the recovery for granted." Labour shadow chancellor Ed Balls called the figures evidence the Tories "have not fixed the economy for working families."[i] While politicians seem to think the UK recovery needs more help, we chalk that up to good old fashioned politicking and recommend investors look past the rhetoric-Britain's economy doesn't appear to need a lifeline.

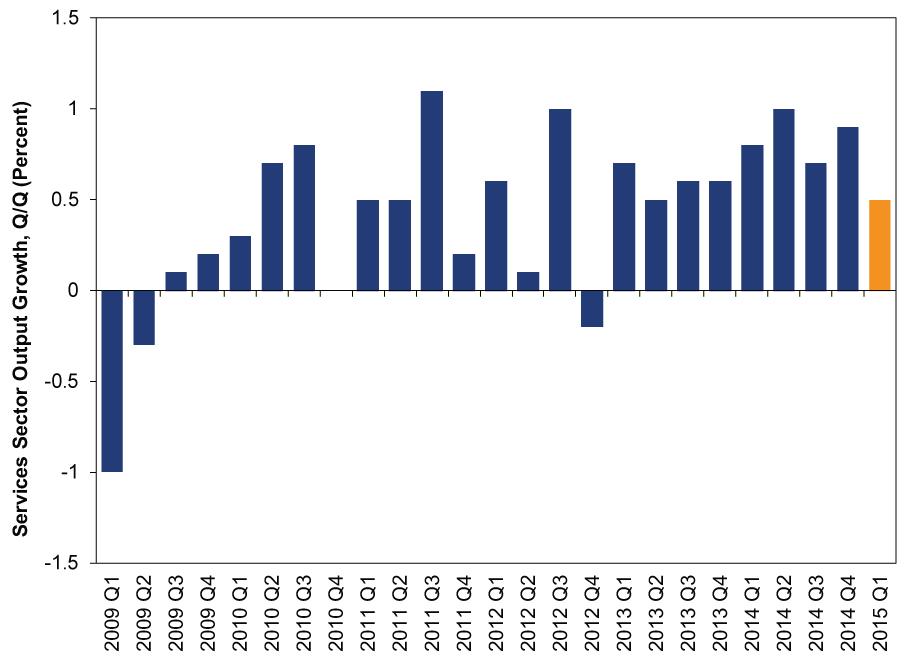

While Q1's growth rate halved from Q4 2014's 0.6% q/q, a look under the hood reveals Britain isn't uniformly weak. Services rose 0.5% q/q, adding 0.4 percentage point to GDP-slower than past quarters, but slowdowns aren't so unusual. (Exhibit 1)

Exhibit 1: Total UK Services Growth

Source: Office for National Statistics, as of 4/29/2015. From 1/1/2009 - 3/31/2015.

While falling Construction output (-1.6% q/q) sliced 0.1 percentage point from growth, this comes with caveats. The Office of National Statistics (ONS), which calculates GDP, has advised "caution should ... be taken" when referencing recent construction estimates, especially as industry surveys have showed strong growth in the sector. For example, Markit's UK Construction purchasing manager's index (PMI) hit 57.8 in March-well above 50, indicating well over half of respondents report expansion. The Construction PMI has been rolling for a while-it averaged 61.8 in 2014-so the ONS figures don't jive with recent trends. The ONS has also been updating their construction methodology, which may be causing some distortions.

Industrial production also fell (-0.1% q/q), due largely to declines in mining and quarrying (-2.1% q/q)-home to the North Sea oil industry. But this isn't a big surprise-UK oil producers have cut back with oil prices down. Though oil's fall was big enough to drag down total industrial output, the industry is but one nook of the UK's economy. Manufacturing, which is broader and more accurately reflects UK industry, rose 0.1% q/q. Not gangbusters, but growth. More broadly, we caution against drawing too much from this report. The preliminary UK GDP estimate has only 44% of the total data used for the final estimate, and we won't know details like expenditure data and how trade contributed until the second estimate.

That hasn't stopped round 984[ii] of griping about Britain's supposedly "unbalanced" economy. Pundits remain skeptical of service-led growth, fearing it's masking weakness elsewhere, and Britain can't be a true dynamo without robust industry and exports. We suspect this comes partly from the Conservative Party's 2010 campaign pledges, which promised to revive UK manufacturing and exports, and partly from history. Britain spent nearly two centuries as an industrial powerhouse. The Industrial Revolution was born there, after all, and Wales was once home to one of the world's largest coal export hubs. Britain's service sector spent much of the 20th century ascending, but it really popped in the 1980s-around the time of the Big Bang financial reforms and wide-scale industrial privatizations (and the associated job losses). As the UK economy underwent these sweeping changes, big dispersion among regional economies emerged. London soared. Many former industrial and mining hotspots didn't, and the tide took many years to begin turning. Needless to say, we understand the fondness for the good old days when industrial jobs were abundant-and the mentality that heavy industry drives growth. For many British towns, it literally did for much of the 20th century.

Yet economies naturally shift, and even those areas that took the brunt as the 20th century aged are evolving and resurging, finding their new niche. "Silicon Britain" and business growth isn't just regulated to London. South Wales was recently named one of the UK's "fastest growing tech clusters." Tech hubs are popping up in Bristol, Cambridge and Edinburgh. Business activity in West Midlands and Yorkshire & Humber has been accelerating. Wales was the UK's fastest-growing regional economy in March. In some cases the evolution took a generation, but it is bringing opportunities and wider prosperity. Britain today resembles your typical developed-world, service-based economy, and its sectoral makeup is normal and natural-it's quite like the US. We think looking at the broadening growth within Britain, rather than the share of service versus manufacturing, is a better way to assess how far-reaching this expansion is.

Competitive, developed nations growing at a decent clip with broad geographic strength usually don't need helping hands. Governments could tinker at the margins, easing a rule here or an outdated tax there, but in our experience, most changes tend to create winners and losers. We have a hard time seeing anything that wouldn't inflict collateral damage of some sort. As for stimulus, that usually works best when a country is trying to fight a recession. When liquidity is tight and consumers and businesses are hunkering down instead of taking risks, a quick jolt from the government or central bank can jumpstart demand. Further into an expansion, however, the efficacy of fiscal stimulus wanes. We've never seen much evidence cash the feds deploy at that point is spent more effectively than it would have been sans stimulus efforts. Moreover, one slow quarter doesn't indicate the sort of broad, falling demand that would need a kickstart. Neither do data like The Conference Board's Leading Economic Index (LEI), up 0.6% m/m in February and in a longer-term uptrend, suggesting further growth is likely.

So as passionately[iii] as politicians may express their views about the economy, we suggest filtering through the rhetoric. In our view, an incomplete, backward-looking data set that shows a growing Britain just doesn't make a compelling case that the British economy is in trouble-especially when so much other evidence contradicts that notion.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] He Tweeted this. And a little while later, he Tweeted his own name, because April 28 is Ed Balls Day.

[ii] This is not a precise estimate.

[iii] We teased the Right Honourable Mr. Balls a bit in the prior footnote, so it's only right that we tease the Conservatives as well, in the name of fair play: So here, we bring you PM David Cameron's slightly awkward efforts to quiet critics accusing him of lacking passion.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The Golden Paradox2026-03-24

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today