Personal Wealth Management / Market Analysis

Britain’s Boom Can Still Zoom

Don't overthink the disconnect between strong UK GDP and wobbly UK stocks. Economic fundamentals should win out.

The UK economy sped up in Q2, with GDP growing 0.7% q/q (2.8% annualized), powered by the mighty service sector and a North Sea oil rebound. Per-capita GDP surpassed its pre-recession peak, a nice (though backward-looking and arbitrary) confirmation of how far the UK has come since the crisis's depths. All in all, the UK's run as one of the developed world's strongest economies continues. But someone apparently forgot to tell UK stocks, which trail most of the developed world and are roughly flat year to date. Some fret this is a sign of things to come, but stocks and the economy aren't joined at the hip.[i] We suspect UK stocks are simply enduring a sentiment-driven wobble, and we think they'll resume reflecting the isle's strong fundamentals soon enough.

Economic fundamentals matter to stocks, but so do politics and sentiment. In the short run, sentiment can easily overpower long-term drivers. This is why bull markets have corrections. The UK's economic and political drivers still look strong. Data and leading indicators remain largely upbeat, and Conservative Party infighting should promote gridlock, easing the risk of radical legislation-something stocks prefer. But sentiment is rocky these days. Investors worldwide are skittish over Greece and China, where domestic markets resumed sliding Monday. UK investors are further bogged down with rumblings over the Labour Party's leadership contest and the eventual referendum on EU membership, which gave "Brexit" fears a jolt.

Neither issue is terribly relevant for stocks at the moment. The EU referendum is at least a year or two away, and PM David Cameron hasn't even started renegotiating the UK's role in the EU yet-and a new deal is a prerequisite for the referendum. Stocks move on probabilities, not possibilities, and the likelihood of "Brexit" is impossible to handicap for now. As for Labour leadership, euroskeptic leftist Jeremy Corbyn might have a whopping poll lead, but we're skeptical UK polling has improved much since May's election, and regardless of who leads Labour for now, the next election is five years away. Stocks don't look that far out, and we rather doubt the UK goes all Syriza between now and then. But sentiment is tricky sometimes, and nervous headlines can weigh on stocks in the short term.

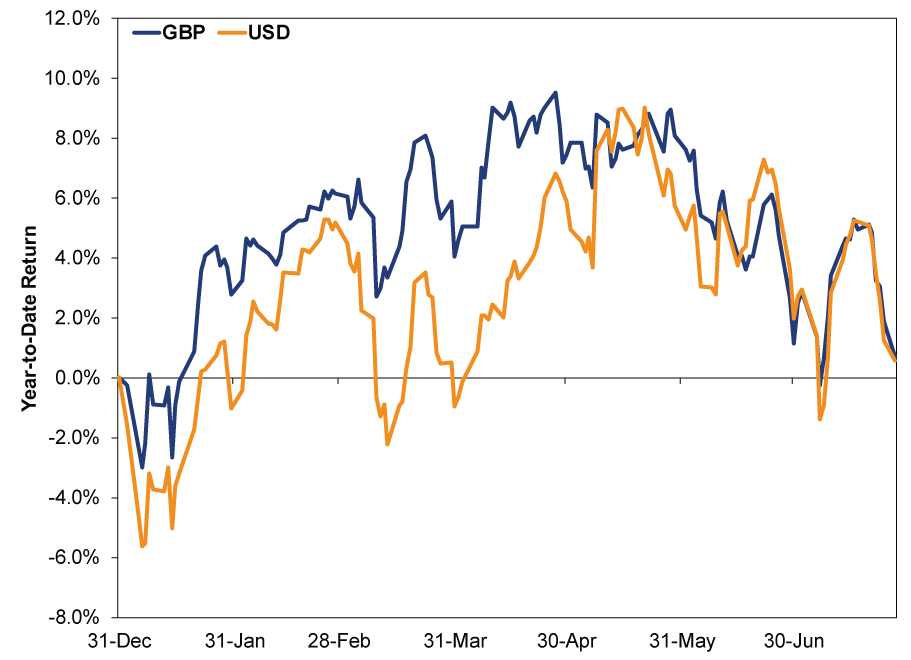

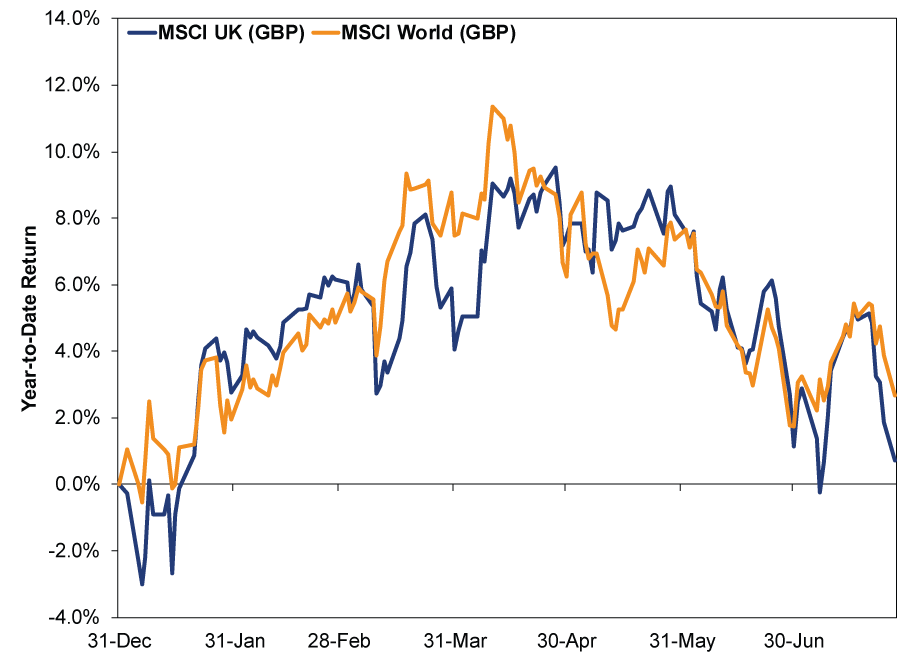

But don't confuse short-term wobbles with long-term malaise. UK stocks were actually having a darned good year until recently. In sterling, they were up nearly 10% on April 27 and still holding up fairly well (and beating world stocks) by late May. (Returns for US-based investors followed a similar track but trailed the world a tad-such is the nature of currency conversions.) Stocks move fast, and it wouldn't take much upside volatility for UK (and world) stocks to regain prior highs and soar even higher. A great year is still in sight.

Exhibit 1: MSCI UK Index

Source: FactSet, as of 7/28/2015. MSCI World Index total returns in GBP and USD. GBP returns are gross of withholding taxes; USD returns are net of withholding taxes.

Exhibit 2: UK and World Stocks

Source: FactSet, as of 7/28/2015. MSCI World and UK Index total returns in GBP. World returns are net of withholding taxes; UK returns are gross of withholding taxes.

Sentiment-driven wobbles aside, fundamentals make a strong case for a strong year. UK and US earnings (excluding the Energy sector) remain fairly resilient to strong currency fears. Broad money supply is growing throughout the US, UK and eurozone. US bank lending remains strong, UK lending is growing again, and eurozone lending is stabilizing. Global growth continues, and leading indicators mostly point to more growth ahead. Gridlock in competitive developed nations (most notably the US, UK and Germany) keeps legislative risk low. False fears like Greece and China prove stocks still have more "wall of worry" to climb. Global (and UK) markets should have plenty left in the tank.

So don't overthink short-term wobbles, in Britain or wherever. Sentiment has simply swung down since June. It can easily swing up again.

[i] We feel compelled to point out what a bizarre inversion this is from earlier years, when rising markets in the UK, US and elsewhere were often seen as euphorically disconnected from the "real" economy.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | Midterm Miracle, US Jobs, Tax Planning

2026-07-07

2026-07-07 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 29 - July 32026-07-07

-

Market Analysis Can Germany Engineer Faster Growth at Last?2026-07-07

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today