Personal Wealth Management / Market Analysis

Calling Time Out on the Payroll Tax Debate

Before leaving for the holidays, Congress gave us all a two-month payroll tax cut debate reprieve. But before they return to politick anew, let’s review what’s at stake.

It looks like Congress now has a deal on the payroll tax “holiday”—for a bit. The two month extension buys time for our fine elected officials to politick more on this issue.

At root in the debate is the potential impact and effectiveness of such an extended holiday. Those supporting extending the holiday say it puts more money into the pockets of workers, giving them more money to spend, (theoretically) stimulating the economy.

Fair enough, and it’s hard to argue against anything letting workers keep more of the money they earn. But such programs aimed at “putting dollars in consumer’s pockets” typically don’t deliver as much stimulation as proponents hope.Why?

Most everyone knows consumer spending is a dominant driver of the US economy—responsible for about 70% of GDP. However, there's a widely held view this spending is hugely volatile—with precipitous drops carrying massive negative economic consequences. Then, too, the belief goes goosing spending higher can have outsized positive economic benefits.

But the reality is, consumer spending just isn’t as volatile as many believe. Most spending is on non-discretionary items: rent, food, utility bills, transportation expenses, insurance, basic necessity household goods, etc. When times are especially good, people typically don't buy more of these things. And when times are not so good, they generally don't have much leeway to buy less of them.

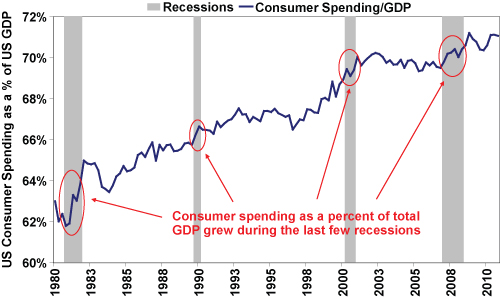

Yes, there are things people spend their money on that aren’t basic necessities—discretionary items like vacations, eating out, luxury goods, etc.—but these expenses represent a relatively small portion of overall consumer spending. Therefore, aggregate consumer spending isn’t so volatile. And during economic recessions, overall consumer spending usually doesn’t fall as much as total output does. In fact, during the last few recessions, consumer spending’s share of total GDP actually grew (see Exhibit 1). So what other factor contributed more to the last economic contraction?

Exhibit 1: US Consumer Spending as a Percent of US GDP

Source: Thomson Reuters, Q4 1980 - Q3 2011.

A relatively smaller economic component (about 11% of GDP) is business investment—but it’s much more volatile than consumer spending. In fact, in the last recession, peak to trough, about half of the contraction came from business investment, which fell roughly -14.7%, as businesses braced to weather the storm. But consumer spending fell only about -1.8% peak to trough. Yes, discretionary spending fell more, but again, because most spending is non-discretionary, it nets out to a fairly stable economic component.

And it works the same on the way back up. Frequently, the media bemoans that “consumers are dead” and the economy can’t recover if consumer spending doesn’t ratchet up hugely. But there’s little historic evidence supporting that view. Typically, consumer spending doesn’t need to recover huge following a recession because it tends to not fall huge. On the other hand, business spending often falls big and bounces back big—helping provide the oomph for a new expansion.

How does this relate to the payroll tax cut? Yes, it’s true extending it gives workers a little more money in their paycheck. And to whatever extent they actually spend this extra money, it could be somewhat stimulative to the overall economy. So extend away! But let’s not assume this is an automatic, huge positive jolt to the US economy.

The last two years’ consumer spending data help illustrate this. In 2010, quarterly change in real personal consumption expenditures were +2.7%, +2.9%, +2.6% and +3.6%, sequentially. That’s pre-payroll tax cut. 2011’s three full quarters reported thus far are all lower: +2.1%, +0.7% and +1.7%.[i] Simply, the economy and consumer behavior are complex, with a variety of inputs. Meaning, the theory pressing a temporary payroll tax cut button assuredly boosts spending is oversimplified, to say the least.

So should lawmakers not extend the holiday again come March, it likely won’t be as disastrous as some argue. It will provide plenty of opportunities to politick, no doubt! While I don’t have any quibbles with politicians letting consumers keep more of their hard-earned cash, it sure seems a more effective means for government to attempt to aid growth might just be focusing on policies that encourage businesses to spend and grow.

[i]Source: US Bureau of Economic Analysis.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 6 - July 102026-07-13

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today