Personal Wealth Management / Market Analysis

Cash Is a Fickle King

Cash may have been king last year, but it lags longer term—hunkering down now likely means missing greater upside later.

Cash topped some versions of 2018’s “periodic table” of asset class returns, beating both stocks and bonds for the first time since 1994 on a calendar-year basis.[i] Combine this feat with US stocks’ worst December since 1931, and cash may seem like an appealing option for 2019.[ii] Why risk more volatility when some banks are finally starting to pass Fed rate hikes on to customers? Yet history argues against this move. Not only do stocks typically do well following the rare period when cash beats all, but for anyone needing some level of long-term growth to fund retirement expenses, cash-like returns over time probably won’t get you there. So whether you see a potential jump to cash as a short-term refuge or a long-term move, we suggest thinking carefully about how such a move could impact your goals and needs.

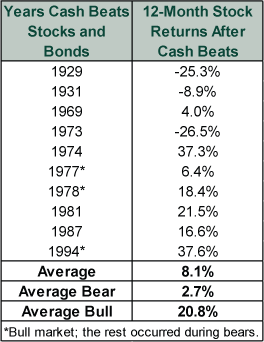

While the desire to avoid sharp swings is understandable and human, the trouble is that avoiding these short-term moves can create greater jeopardy through earning returns that are too low. Cash rarely returns more than stocks or bonds. Since good US stock market data begin in 1925, cash beat stocks and bonds in 10 other calendar years. Over the following calendar year, stocks rose 7 of 10 times, averaging 8.1%.[iii] (Exhibit 1) Of the three negative occurrences, two occurred during the Great Depression, after 1929 and 1931. The third occurred after 1973, during the second year of a big bear market. Only three years when cash was king didn’t occur during bear markets—1977, 1978 and 1994. In the first two, interest rates were historically high! And moreover, stock returns in the following year were 6.4%, 18.4% and 37.6%, respectively.[iv] As a result, to expect cash to lead again next year would be to either argue against history or expect a deep recession and one of history’s longest bear markets, considering global markets peaked nearly a year ago.

Exhibit 1: Cash Seldom Reigns for Long

Source: Global Financial Data, Inc., as of 12/17/2018. S&P 500 calendar-year total returns in 1930, 1932, 1970, 1974, 1975, 1978, 1979, 1982, 1988 and 1995.

Volatility often makes folks seek changes to the mix of stocks, bonds, cash and other securities they use. If this is driven by a shift in your investment goals or needs, that is understandable and something you should discuss with your financial professional. And if you have near-term income needs, then yes, keeping cash on hand to cover them is prudent. Any money with a very short time horizon, like money earmarked for an upcoming home purchase, remodel, near-term tuition costs and the like, should probably be in cash or cash-like securities. That applies regardless of recent market conditions. But if you have a long time horizon and need equity-like returns to fund your goals and future needs, increasing cash may raise risk, not mitigate it. If you don’t get the growth you need, you can run out of money late in life. Stocks have historically returned 10.8% annualized since December 1925,[v] which includes all corrections and bears along the way. Unless you see big negatives ahead others miss, the best tactic is usually staying patient.

Historically, markets have always recovered from downturns. Moving to cash after markets fall only locks in a decline. Timing a re-entry presents its own problems. There are no reliable all-clear signs—often the best time to buy is when things seem darkest; when you are least likely to buy. By the time things don’t seem as scary, stocks have usually already bounced. It is impossible to know when this recovery will begin, but that is why an all-cash strategy doesn’t seem optimal to us. Widening our dataset from calendar years to rolling 12-month periods, there are 26 distinct periods in history where cash outperformed for 12 months or longer. Those periods ranged from 12 to 37 months.[vi] That is a big range! While not pleasant, history shows gritting your teeth and sitting tight gets you through most unscathed.

Now, if there is a recession around the corner that most don’t see—and markets therefore haven’t priced—getting defensive may make sense. But with the amount of coverage a potential recession has received in financial media lately, we think there is a high likelihood stocks have already discounted that possibility. Thus, even if a recession does occur, it may not lead to further, prolonged market declines. Stocks usually start rising long before economic growth returns. With that said, forward-looking economic indicators—like The Conference Board’s Leading Economic Index, global yield curves, purchasing managers’ new orders, private lending and money supply growth—point to expansion ahead.

Ultimately, we anticipate markets rebounding as sour sentiment subsides. The times cash is king are fleeting. While alluring, it isn’t a crown that should impress long-term investors.

[i] Source: FactSet, as of 1/3/2019. Statement based on calendar year 2018 total returns of the S&P 500 index, BofA Merrill Lynch US Corporate & Government (7 – 10 year) index and Bloomberg Barclays 3-Month T-Bill, which represents cash.

[ii] Source: Global Financial Data, Inc., as of 1/2/2019. Statement based on S&P 500 monthly total returns since 12/31/1925.

[iii] Ibid., as of 12/17/2018. S&P 500 calendar-year total returns in 1930, 1932, 1970, 1974, 1975, 1978, 1979, 1982, 1988 and 1995.

[iv] Ibid.

[v] Ibid. S&P 500 Total Return Index, December 1925 – November 2018.

[vi] Source: Global Financial Data, Inc., as of 12/18/2018. S&P 500, US 10-year government bond and US 3-Month T-Bill total return indexes, 12/31/1924 – 11/30/2018.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Market Analysis Rounding Up Odds and Ends From Global Energy Developments2026-03-11

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

-

Economics Pain at the Pump Won’t Hurt the Global Economy2026-03-10

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today