Personal Wealth Management / Market Analysis

Charting the Future

With all the recent market volatility, can the charts tell us what to expect next?

Can chart formations tell you the future? Photo by Mario Tama, Getty Images.

With 2014 off to a bumpy start, it seems every chart-watcher has a theory about what the volatility means for future returns. The Dow is below its 200-day moving average, a sell signal. But wait, the VIX is high, so is it time to buy? The S&P 500 crashed through its “support,” another sell signal. Support now pivots to resistance, and technicians suggest rising back above it is a bullish sign to look for. (Of course, if you’re a very short-term investor, you might want to catch the ride up past that new resistance level, but we digress.) We’d understand if you have trouble following all of that—taken in concert, the universe of technical indicators seemingly recommends day trading your entire portfolio—a wee bit of bad advice for a long-term investor, in our view. Here’s the encouraging news: You don’t need to master candlestick charting or Fibonacci retracements. Chart patterns don’t determine stock returns. To assume they do assumes past performance dictates future returns. That statement is not mere legalese—stocks aren’t serially correlated, so it’s a fallacy to think today’s movement begets anything tomorrow. None of the technical charts circulating today tell us where stocks will be tomorrow, next week, next month or six months from now (or ever). Moreover, short-term swings are impossible to predict and time with certainty—volatility could very well continue, but for long-term growth investors, what matters more is stocks still appear well-positioned for a good year.

To see why charts lack power, consider a long-time favorite of many chartists: an index’s 200-day moving average. Many believe if an index’s current level has exceeded this average for a while, stocks will keep rising, but if they fall below, more downside is in store. The (broken) Dow fell below its 200-day average on Monday, and chartists are eyeing the S&P 500 to see if it does the same. But think about what this indicator implies, and you’ll likely find it doesn’t hold up. In happy times, it says rising stocks beget rising stocks. In a downturn, it says a sizable drop begets another drop. But that isn’t how markets work! Trends aren’t self-perpetuating—and markets are volatile. They can turn on a dime, for any or even no apparent reason. Were it otherwise, folks wouldn’t get fooled time and again.

The rug doesn’t get pulled out from under stocks simply because some arbitrary line gets crossed on a chart—there is no magic threshold at which a downturn automatically gets deeper. Sure, the S&P has crossed below its 200-day moving average during bear markets, but coincidence isn’t causality—this is just an interesting observation and something that largely goes without saying in a deep, long downturn. Not every cross has coincided with a bear market. Plenty were corrections! The S&P 500 crossed below its 200-day average during the corrections of 2010, 2011 and 2012—but the bull market continued. It also crossed below during the corrections of 1998, 2003 and 2006. More bull market followed.

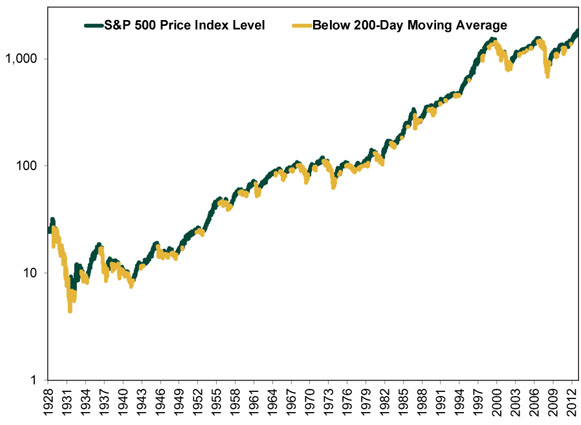

Many instances are false reads—plain old volatility! The S&P crossed below the 200-day average in October 1992—six months after a correction—and dipped below in 1996. Yet the 1990s bull raged on! It also spent time below the magic line in October 1985 and September 1986—smack in the middle of the 1980s bull. The S&P was below its 200-day moving average at many points during the 1974-1980 bull—yet stocks achieved a 126% return.i If an investor jumped out of stocks during any of these false reads, they could have left significant returns on the table—after all, the indicator doesn’t tell you when to get back in! Stocks can stay below their 200-day average after the upswing begins. (Exhibit 1)

Exhibit 1: S&P 500 Price Level Since 1928 (Logarithmic Scale)

Source: FactSet, as of 02/04/2014. Dataset from 1/3/1928 – 2/4/2014. Yellow line shows when the S&P 500 Price Index was below its 200-day moving average.

If the S&P crosses below its 200-day average this time around, what does it tell you? Nothing! It might be a blip. Maybe it turns into a correction. But breaking this arbitrary “threshold” doesn’t automatically mean more downside is ahead. It simply means stocks are down a bit NOW. That doesn’t affect markets’ direction—forward-looking economic, political and sentiment drivers do.

The past doesn’t determine the future: Past returns don’t determine future returns, and past volatility doesn’t determine future volatility. Where stocks go tomorrow has nothing to do with what they did yesterday. Volatility could very well continue in the near term, but not because stocks slid last month—just because markets are volatile.

Bumps and jumps are normal, and they’re impossible to predict—volatility is driven by emotions, and emotions swing from one day to the next. As Ben Graham said, in the short term, markets are voting machines. But in the long term, they’re weighing machines, and markets have plenty of positives to weigh over time. The global economy, overall and on average, continues performing better than many expect. Leading Economic Indexes are high and rising, suggesting the current global expansion has plenty of fuel. Competitive developed countries like the US and UK have gridlocked governments, lowering the likelihood of radical change that could spook markets, and free market reforms continue throughout the developing world. And of the extant risks, most are widely discussed, and the less-appreciated negatives aren’t big or likely enough to upend all the positives at work. This is a great backdrop for stocks. With sentiment still skeptical, few realize just how strong the world is. So while stocks might hop around in the near term, over time, they have plenty of reasons to keep rising for the foreseeable future.

i S&P 500 Price level return from 10/03/1974 – 11/27/1980. Source: FactSet, as of 12/2/2013.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Bourse : pourquoi l’impact de la guerre en Iran sera moins important que prévu – par Ken Fisher2026-04-01

-

Market Analysis Countertrends and Corrections: Banks in 2026’s Early Selloff2026-04-01

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-01

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 4/1/2026

New to Fisher? Call Us.

Contact Us Today