Personal Wealth Management /

Upside Dow

The Dow Jones Industrial Average will be adding three new stocks—but does it even matter?

No need to grit your teeth over the Dow’s newest additions. Photo by Spencer Platt/Getty Images.

Editor’s Note: MarketMinder does not recommend individual securities; the below is simply an example of a broader theme we wish to highlight.

Stop the presses! The Dow Jones Industrial Average index will undergo 10% turnover, effective end of trading September 20th! Say hello to Visa, Nike and Goldman Sachs! Bon voyage Bank of America, Alcoa and Hewlett-Packard! All of which we respond to with a yawn. The announced changes to the Dow highlight just how broken an index it is.

The Dow’s governing Index Committee announced the changes Tuesday in an effort to better “balance” the Dow, revealing its inherent flaw: price weighting. The three stocks given the boot had share prices the committee deemed “too low.” In a price-weighted index, a low stock price means your impact is reduced. Alcoa (~$8), Bank of America (~$15) and Hewlett-Packard’s (~$22) impact on the Dow’s movements was insignificant. While they’re 10% of the index by number (3 of the Dow’s 30), their combined weight was about 2% of the index. (A figure swamped by IBM alone, which has a nearly 10% weight in the index.) So the committee decided to fix the problem by replacing the low-priced stocks with Visa, Nike and Goldman Sachs, which all have higher share prices. Problem fixed, right? Not quite. The problem is with using price weighting itself. If you have to keep rejiggering your index’s constituents to avoid a heavy concentration or top-heavy skew, your methodology may be a wee bit problematic.

Let’s look at this more closely, comparing two Financials stocks swapping spots in the Dow: Bank of America and Goldman Sachs. As of September 10, 2013, Bank of America’s share price was around $15 while Goldman Sachs was about $165. The Dow weights Goldman’s movements over 11 times as heavily as Bank of America. Yet if we look at market-capitalization (a size measure calculated as the stock price times number of shares outstanding) weighted indexes, we see a totally different phenomenon. In a market cap-weighted index like the S&P 500, the Dow’s script is flipped. Bank of America influences S&P movement much more due to its $156 billion market cap—double Goldman Sachs’ $74 billion. In our view, a company’s market cap size is a much more important consideration in market impact than share price.

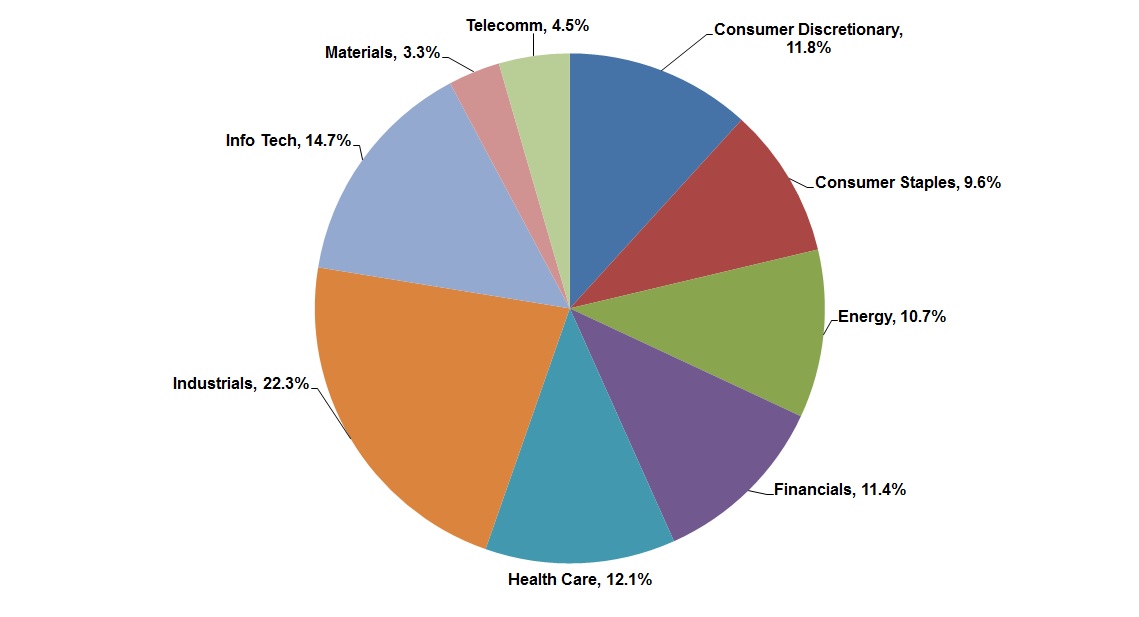

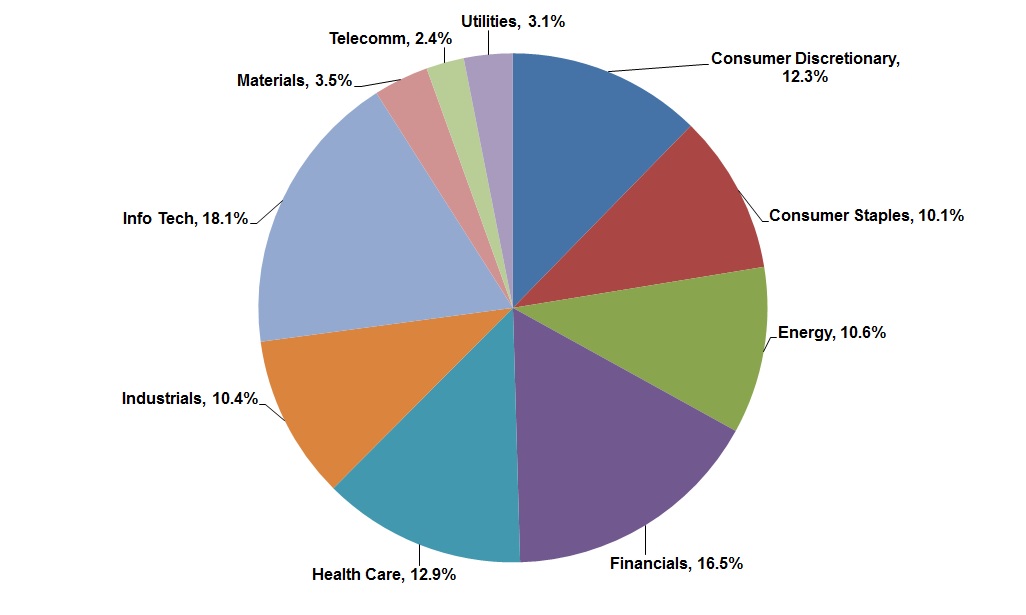

Though price weighting is the Dow’s most egregious flaw as an index, it’s not the only one. Before the change, The Dow had a 22% weight to Industrials—double the market-cap weighted S&P 500 Index’s 10%. And it still has no allocation to Utilities—admittedly, not the largest sector, but a sector. If you consider size a more important factor than price, like us, the Dow’s composition makes little sense. Exhibits 1 and 2 compare the Dow and S&P.

Exhibit 1: Dow Jones Industrial Average Sector Breakdown, as of 9/11/2013

Source: Bloomberg, as of 9/11/2013.

Exhibit 2: S&P 500 Sector Breakdown, as of 9/10/2013

Source: S&P Dow Jones Indices, as of 9/11/2013.

The Dow also only holds 30 stocks—a tiny sliver in the grand scheme of global equity markets (the MSCI World Index, for example, carries 1600 stocks). If you want to look at something US specific, the Dow is still far from diverse—the 30 stocks are 1% of the number listed on the New York Stock Exchange (2800).

Yet Dow performance is continually cited by major news sources, something we won’t be able to change. But in our opinion, the Dow’s importance is mostly a trivial matter, and we’d suggest investors ignore the movements of the heavily flawed Dow altogether. (Speaking of market trivia, which is the only company that has been in the Dow from its inception in 1896 to today? The answer’s here when you’re ready.)

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | Midterm Miracle, US Jobs, Tax Planning

2026-07-07

2026-07-07 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 29 - July 32026-07-07

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03 -

Market Analysis Declaring Fed Independence Fears False2026-07-01

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today