Personal Wealth Management / Economics

Checking in on US Growth

Recent data suggest the US economy gained speed in Q2.

With Brexit dominating headlines and driving most investors to fixate on Europe, many have likely missed recent US economic data. With that in mind, we thought you might benefit from a little data rundown-a rundown that suggests the economy is humming along just fine, and should continue to looking forward. In our view, these cyclical factors are much more important to stocks than the implications of Brexit, which likely take years and years to sort out and are unknowable today.

In its third estimate of US Q1 GDP, the Bureau of Economic Analysis revised growth upward, from 0.8% annualized to 1.1%, more than double the initially reported 0.5%. Admittedly, this is backward-looking and stocks have since moved on, but the prior estimates sparked fears of sluggish US growth. It turns out growth wasn't quite as sluggish as many previously thought.

More importantly, recent economic data suggest growth is already reaccelerating. Consumption data have been strong. May retail sales rose 0.5% m/m (2.5% y/y). This is a subset of overall consumer spending, but notably, gas station sales contributed on a monthly basis for the third straight month. This suggests gas station sales may soon cease detracting from year-over-year figures-an early sign that oil prices' drop is poised to fall out of economic data in the near future. On a broader level, the Commerce Department reported real consumer spending jumped 0.3% m/m in May (2.7% y/y), after climbing an upwardly revised 0.8% in April (3.0% y/y). As this accounts for about 70% of total output, it's a fairly good sign the economy is stronger than many think.

Beyond consumption, data also show health. The Institute for Supply Management's June Manufacturing PMI-a survey tallying the percentage of firms reporting growth-rose from May's 51.3 to 53.2-the highest level since February 2015. The gauge dipped below 50 from late 2015 into early this year, igniting recession fears, but the rebound since is evidence those fears were overstated. Moreover, the New Orders Index jumped to 57.0 from 55.7 in May, a strong indication the sector will continue growing, as today's orders are tomorrow's output.

Based on these and other economic data reported throughout the last few months, many are now ratcheting up growth expectations for Q2. The Federal Reserve Bank of Atlanta's GDPNow and the New York Fed's Nowcast-two attempts to estimate GDP based on summing up component data as they are released-suggest Q2 GDP growth will clock in at 2.6% and 2.1%, respectively. While these estimates are flawed, as they have limited histories and rely on a combination of incomplete datasets and backward-looking data to forecast future growth, they show Q2 growth is widely expected to pick up from Q1. Separately, 60 economists surveyed by The Wall Street Journal estimate GDP will grow an annualized 2.4% in Q2.

Now, in response to these estimates naysayers may say, "Yeah, but this was before Brexit." And that's true! But while Brexit may impact the US economy down the road to some unknowable, to-be-determined extent, it's highly unlikely to do so in the here and now. For the foreseeable future, US firms will very likely continue to do business with UK counterparts as usual, and besides, the US economy isn't all that dependent on Britain. In 2015, 3.7% of US goods and services were exported to Britain and just 2.6% of US imports came from the UK. Besides, markets sure don't seem to be signaling material economic problems resulting from Brexit are all that likely. That could change! But for now, there is no sign of it.

Looking beyond Q2, growth looks set to continue. The Conference Board's Leading Economic Index (LEI) fell -0.2% m/m in May, but a deeper look into the components suggests the read is stronger than the headline number seems to convey. Of the index's 10 components, only three were negative, and they aren't the economic warning signs they may appear on the surface. Two (consumer expectations and jobless claims) are among the LEI's least predictive components and the third (stock prices) is volatile. Moreover, it detracted in May only because of a calculation quirk: The Conference Board compares the month's average daily S&P 500 closing price to the prior, not the actual return. Using LEI's methodology, stocks fell -0.4% in May. But looking at the actual index level at the beginning and end of the month, stocks rose 1.5%.[i] This highlights the series' occasionally noisy nature.

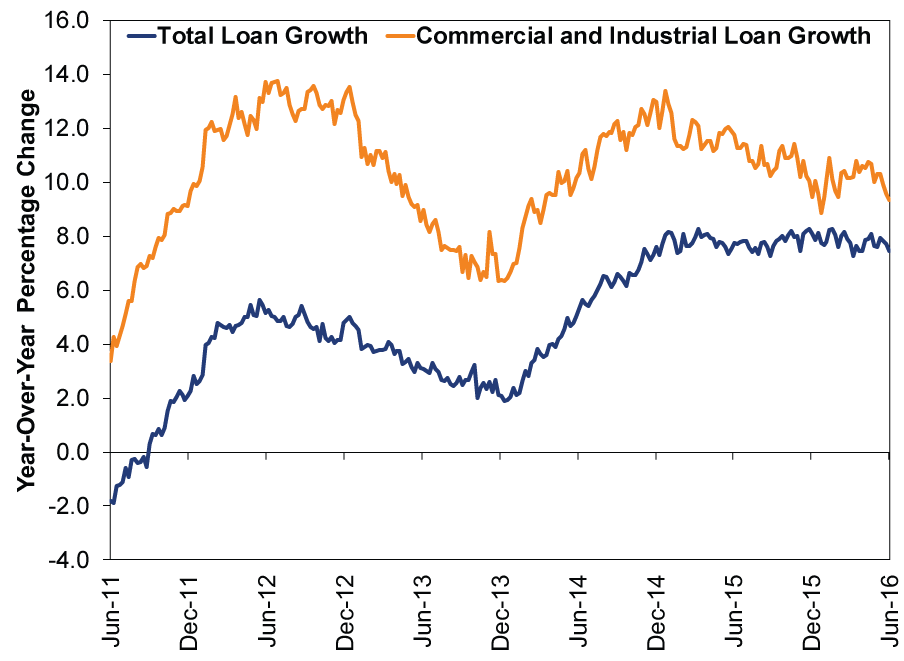

Meanwhile, the contribution of the yield curve-the difference between the fed funds rate and the 10-year Treasury yield-stabilized. This is arguably the most forward-looking of the LEI's components as it's a good proxy for banks' willingness to lend. And lending they are. Total loan growth averaged 7.7% y/y in the four weeks ended June 22, with Commercial and Industrial lending rising 9.8%.

Exhibit 1: Lending is Expanding

Source: Federal Reserve Bank of St. Louis, as of 7/1/2016. Year-over-year growth for all commercial banks, weekly, June 22, 2011 - June 22, 2016.

As a result, the money supply is also growing, another sign banks are lending, as money is created when banks extend loans. M4-the broadest measure of money-grew 5.2% y/y in May and 4.9% y/y in April.[ii] Since economic growth is predicated on businesses' and individuals' access to financing, this is a sign the economy remains on firm footing.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

See Our Investment Guides

The world of investing can seem like a giant maze. Fisher Investments has developed several informational and educational guides tackling a variety of investing topics.

Related Resources

-

In The News Avoiding Summertime Scams6/30/2025 12:00:00 AM

-

Expert Commentary 3 Things You Need to Know This Week | Central Bank Forum, June PMIs, US Jobs Data (June 30, 2025)6/30/2025 12:00:00 AM

-

Expert Commentary This Week in Review | Israel-Iran Conflict, Fed Chair Testimony, Q2 2025 Recap (June 27, 2025)6/27/2025 12:00:00 AM

-

In The News Notes on a Round Trip6/27/2025 12:00:00 AM

Learn More

Learn why 175,000 clients* trust us to manage their money and how we may be able to help you achieve your financial goals.

*As of 3/31/2025

New to Fisher? Call Us.

Contact Us Today