Personal Wealth Management / Politics

China Check-Up

Spotty data over the course of Q1 have worried some about not only China’s chances for growth this year, but also the world’s. So what do the data have to say?

A common storyline thus far in 2012 has been China’s likely economic trajectory—whether its officials step too hard and fast on the brakes in their inflation fight, causing growth to fall sharply (hard landing); or whether they intentionally ease growth off, only to reaccelerate it in the wake of this year’s election. As we’ve said before, we believe the latter scenario likelier, given there’s some historical precedent for that course of action.

But recent data have admittedly been less than reassuring—from mixed and contradictory PMI to weak industrial production, hugely volatile import growth and decreased export growth and retail sales (among other data points), some have feared China’s slowdown would hurt chances for global growth this year, too.

Thursday’s news brought a surprise, though—China unexpectedly announced one trillion yuan in new loans in March, handily beating analysts’ expectations. That’s the highest monthly lending rate since January 2011 and the strongest loan growth for the month of March since 2009. Further, the monetary base increased 10.6% year over year, accelerating from 8.8% growth in February. Money supply growth is one of several mechanisms the Chinese government has to help it control the economy—and it seems this time, they previously let money supply growth fall to an extreme cyclical low (to rein in inflation), only to potentially begin loosening those reins in March (possibly to goose growth with lower risk of juicing inflation).

Now, this doesn’t necessarily mean China suddenly starts registering straight-line, torrid growth rates from here—indeed, China’s as subject to economic data volatility as any other country, and monetary adjustments can take time to register in data. But it does seemingly signal the government’s quiver is not empty when it comes to spurring economic growth.

Friday, China is expected to release industrial production, retail sales and investment data for March, as well as GDP for the first quarter. The consensus expects deceleration across the board—and that’s entirely possible, given the aforementioned weaker data China’s generated over the last couple months.

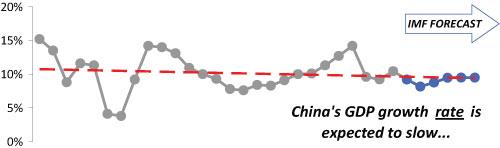

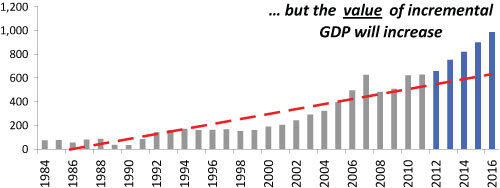

But keep in mind China doesn’t necessarily need to churn out a red-hot growth rate to contribute significantly to global GDP growth—after all, China’s currently the world’s second-largest economy. So even growth considered sub-par relative to recent gangbusters rates would add significantly to global GDP (see Exhibits 1 and 2).

Exhibit 1: China Real GDP Growth

Exhibit 2: China’s Incremental Real GDP in Dollars

Source: Thomson Reuters, IMF; as of 03/05/2012. Dollar GDP growth is measured in 2011 dollars with the current exchange rate held constant.

Thursday’s loan growth data are admittedly a single brushstroke in what will ultimately be this year’s global economic picture. And thus far, China’s contribution has seemingly hinted at an economic slowdown (which is still growth)—at least domestically. But even without drawing any big conclusions, these recent data indicate a government that hasn’t run out of tools to spur China’s growth this year—and if it’s even modestly successful, that has the potential to aid global growth pretty significantly.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Fed Rate Decision, US-Iran, Inflation in Europe

2026-06-19

2026-06-19 -

Market Analysis Reviewing Q1 Earnings and What Q2 Expectations Say2026-06-18

-

Market Analysis Kevin Warsh and the Magical Delete Button2026-06-17

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today