Personal Wealth Management / Market Analysis

China’s 18th Party Congress

China’s power transition this week is an important event, but it’s unlikely to surprise markets or mean much in the way of change ahead.

On November 8, China began its 18th Party Congress. Held every five years, the Party Congress sets new policy directives and “elects” new leaders. The event usually lasts roughly a week, with major political appointments announced the last day, including the makeup of the Politburo, the Politburo Standing Committee (PSC) and the General Secretary. Thus, by mid-November, investors should definitively know China’s next leaders. While obviously important, the event is unlikely to surprise markets one way or the other, given how broadly telegraphed key decisions have been the past several months.

China’s government structure is unique—a closed, one-party system led by the Chinese Communist Party (CCP), which assumed power in 1949 following a civil war with Chiang Kai-shek’s Nationalists (who invaded and established a government in exile in Taiwan after defeat). The CCP dominates all aspects of state and society, including the military, political appointments, state-owned enterprises (which control the stock market and economy), the media and the judiciary.

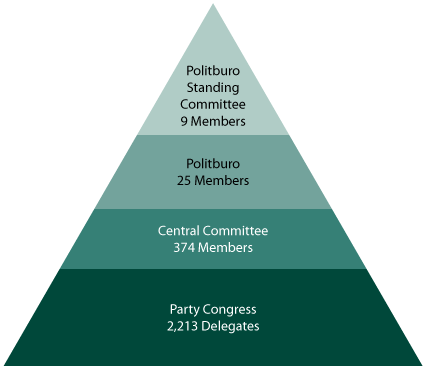

The pyramid in Exhibit 1 illustrates the CCP’s distinct hierarchy. The Politburo Standing Committee (PSC) is the country’s most powerful decision-making body, currently consisting of nine members, each responsible for a specific portfolio of government (e.g., military, trade). Each member of the PSC belongs to the broader Politburo, whose 25 members represent the most important senior group of Communist Party officials.

Exhibit 1: Chinese Communist Party Hierarchy

Source: Fisher Investments Research.

Within the PSC, the General Secretary (currently Hu Jintao) is the highest-level position and the de facto leader of the CCP, serving as the head of the military and head of state. The Chairman of the National People’s Congress (currently Wu Bangguo) is the second-ranked official and head of the country’s law-making body. The Premier of the State Council (currently Wen Jiabao) is the third-ranked official, appointed by the President but overseen by the NPC, and is the de facto functional head of state power.

Even though we won’t know with certainty until the end of the Congress, the country’s new leaders have been widely telegraphed. Xi Jinping (pronunciation: Shee Jin-ping) is expected to replace Hu Jintao as General Secretary, while Li Keqiang (pronunciation: Lee Kuh-cheeyahng) is expected to replace Wen Jiabao as Premier of the State Council.

The CCP is dominated by two factions, the “princelings” and the “Youth League,” each equally powerful but representing different constituencies. The factions are typically balanced within the PSC to ensure stability.

Princelings: The princelings are from long-time prominent families and tend to be more liberal on market reform but conservative politically. Former General Secretary Jiang Zemin, Hu Jintao’s predecessor, is primarily associated with this camp, as is incoming General Secretary Xi Jinping.

Youth League: This faction comes from much humbler backgrounds, having worked their way through the power structure of the Youth League, a junior political organization affiliated with the Chinese Communist Party. Supporters tend to be more liberal on the political front but more conservative on market reform. This is the camp of current General Secretary Hu Jintao and likely incoming Premier Li Keqiang.

Despite the individual differences between the leaders, however, China’s political model is built on consensus building and collective leadership. Even the General Secretary must gain the consensus of the PSC to implement major decisions. This is one reason not to expect quickly implemented significant reform from the new government—there likely be a period of horse-trading and bargaining.

Beyond the announcement of the new PSC, investors will also pay close attention to the Political Report, which is essentially a manifesto of the government’s policy agenda. There is broad consensus surrounding the immediate challenges facing the government: structural reform to address current economic challenges and political reform following the crisis of legitimacy raised by Bo Xilai, the recently ousted Politburo member. Many believe reforms will accelerate under the new leaders as they are younger, well-educated and have grown up in a world where China wasn’t an isolated, inward-looking monolith. Moreover, structural problems have reached a point where they may begin to endanger social stability—perhaps the CCP’s biggest fear. On the economy, this is most likely to include policies promoting the private sector and liberalization of the financial system.

Ultimately, despite the handover of power, we don’t expect much change ahead—the agenda of the new regime isn’t likely to be much different than that of the old.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today