Personal Wealth Management / Market Analysis

China’s False Choice

Addressing financial sector risks needn't imperil Chinese growth.

2017 has had a lot going on, but until recently, one thing had been missing: China hard landing fears. They've taken center stage annually during this bull market, but all was quiet on the China front earlier this year as GDP growth beat expectations and capital markets didn't do anything wacky. But now, this is changing. First April economic data disappointed as credit tightened, sparking fears China can't have it both ways. Then the folks at MSCI, who are weighing whether to include mainland Chinese stocks in Emerging Markets benchmarks this year, gave the country's capital markets a dismal progress report. Capping it off Wednesday, credit ratings agency Moody's downgraded Chinese debt for the first time since 1989. Aaaaaaaand, cue hard landing fears! If anything, however, a notoriously late-to-the-game ratings agency's acknowledgment of China's question marks should be a sign that markets have already considered all of this and more over the last eight years of hard landing fears. In our view, there aren't material, negative fundamental changes in China this time around-the hard landing is unlikely as ever.

Those widely bemoaned April numbers did show decent growth, but industrial production (6.5% y/y), retail sales (10.7% y/y) and fixed investment (8.9% year-to-date compared to the same period in 2016) all slowed. The likely culprit: the government's efforts to curb junky debt, which include interest rate hikes, a crackdown on refinancing distressed debt and new curbs on opaque high-yielding debt investments. Meanwhile, the MSCI China A Index-which tracks most mainland stocks-slid -7.5% from early April to early May,[i] which some interpret as a sign the economy can't take the pressure.

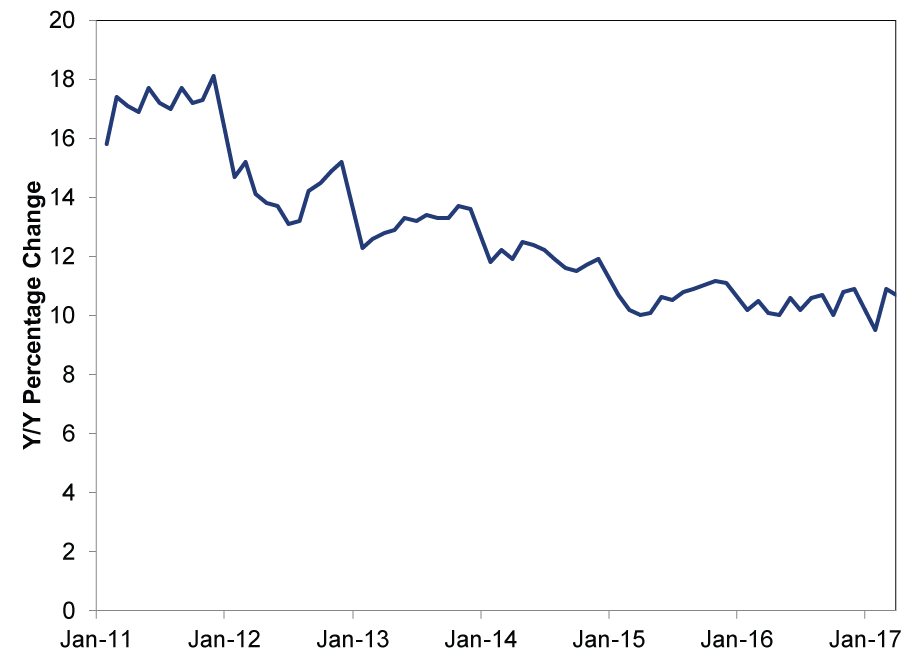

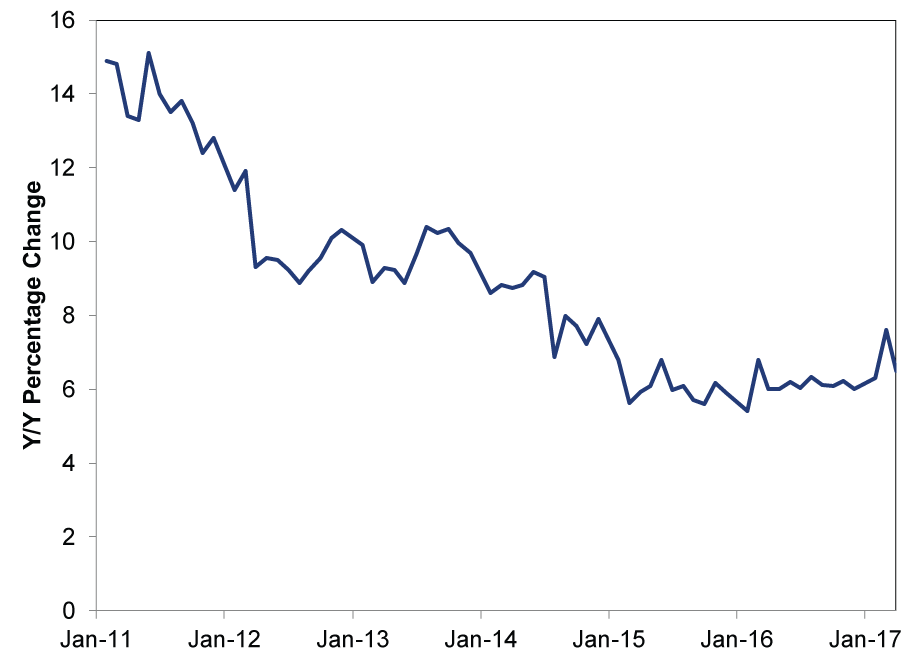

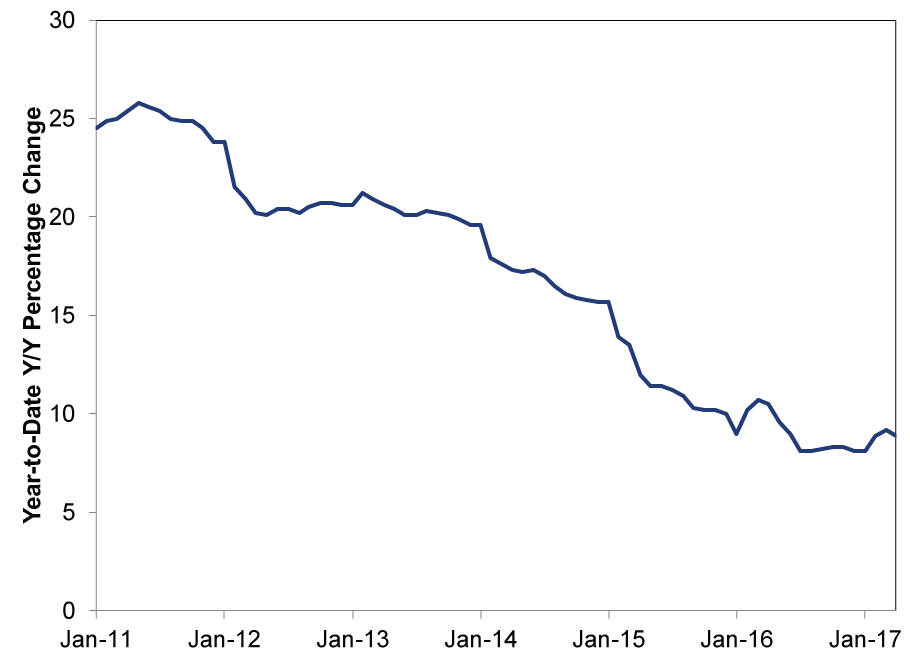

Despite the slowdown, we don't think April's data should ring alarm bells. As Exhibits 1 - 3 show, industrial production, fixed investment and retail sales growth rates have zig-zagged lower for years. April's figures actually exceed most 2016 - 2017 figures. Monthly data volatility is normal.

Exhibit 1: April in Perspective - Retail Sales

Source: FactSet and National Bureau of Statistics of China, as of 5/19/2017. China Retail Sales, January 2011 - April 2017. January - February figures combined to remove Lunar New Year skew.

Exhibit 2: April in Perspective - Industrial Production

Source: FactSet and National Bureau of Statistics of China, as of 5/19/2017. China Industrial Production, January 2011 - April 2017. January - February figures combined to remove Lunar New Year skew.

Exhibit 3: April in Perspective - Fixed Asset Investment

Source: FactSet and National Bureau of Statistics of China, as of 5/19/2017. China Fixed Asset Investment, January 2011 - April 2017.

That said, there is some evidence the government's efforts to reduce financial sector risk are having an effect. Borrowing costs are up, debt issuance is down, and banks are issuing fewer wealth management products-risky, high-yielding alternatives to traditional deposits. All are efforts to combat the issues Moody's highlighted Wednesday-overrated fears, in our view, though it is fair to say China's efforts to stoke growth in years past carried some side effects like supply gluts and a build-up of municipal debt. These are manageable, however, and industrial production's lengthy slowdown is a testament to that. If the government's assault on easy credit is knocking output somewhat now, it wouldn't surprise. Sometimes, the impact is deliberate. This is the same government that blew up blast furnaces in 2014 to battle a steel supply glut, demonstrating its willingness to inflict collateral damage in the name of longer-term stability. Small pinches like this are normal for China and don't mean a hard landing is in store.

Even with the crackdown and slower growth, China is still, you know, growing, and officials have plenty of wiggle room to keep it that way. There are some signs they've already started loosening the spigots to ensure growth stays steady heading into the Communist Party's November leadership shuffle, including a big liquidity infusion in May. Vast foreign currency reserves provide further firepower. This might sound like kicking the can, but China has always had the ability to withstand some corporate and municipal defaults. It just hasn't wanted to. Should that change, markets might welcome a less interventionist approach as an important step in China's long-term evolution.

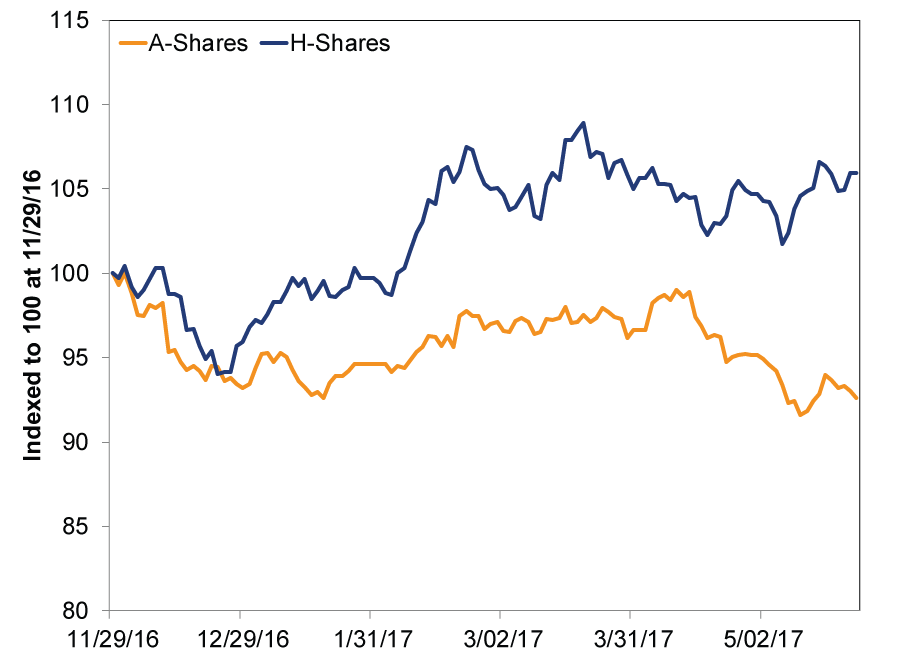

As for mainland stocks' pullback, we think it is a mistake to presume they are pricing in economic troubles. While stocks generally are leading economic indicators, China's domestic market is a special case. It is largely off-limits to most foreign investors, so it swings hard on Chinese investors' whims, and their primary information sources are state-run media and local rumors-hence MSCI's reluctance to include it. Echoing US investors before 1929, Chinese investors have shown a tendency to treat stocks as gambling or get-rich-quick opportunities, not long-term investments (preferring real estate). Hence, mainland shares are very prone to boom and bust as folks trade on fear and greed. Conversely, shares of Chinese companies listed in Hong Kong (known as H-Shares), where foreign investors trade regularly, seem to more accurately reflect fundamentals. While A-shares are down -7.4% since hitting a high on November 29, 2016, H-shares are up 5.9%.[ii]

Exhibit 4:Mainland Shares Lag Freely Traded Alternative

Source: FactSet, as of 5/24/2017. MSCI China A and H (in yuan) with gross dividends, 11/29/2016 - 5/23/2017.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The Golden Paradox2026-03-24

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today