Personal Wealth Management / Market Analysis

The Return of a Chinese Ghost Story

Worries about Chinese bond markets are all part of the same ol' yarn.

China fears kicked off 2016, and after the relative quiet[i] following the tumultuous start, some old ghosts have returned. This time, Chinese bond markets are grabbing headlines, spurring questions about potential financial system stresses. In our view, this is the latest in a litany of overstated fears about China-there is little sign the most recent feared problems are a real risk to the world's second-largest economy.

When the Fed hiked rates on December 15, sovereign debt yields rose globally-yet China got special attention after its 10-year bond yield hit a 16-month high of 3.4%. Rising government and corporate bond yields mean higher borrowing costs, which amplified fears over Chinese corporate debt. Toss in angst over wealth management products (WMP)-which some fear banks use to speculate on bond prices-and this adds another dimension of risk if things turn south.

If you feel like you've heard this before, your thoughts aren't betraying you: Headlines about Chinese bonds and WMPs have popped up before, related to that oft-feared, though never-seen, economic "hard landing." Worries about Chinese debt in general have been commonplace since 2011. WMP concerns? Those were so 2013. It isn't just debt and financial products, either. Questions about Chinese property arise constantly: 2009, 2011, 2014 and even today. Manufacturing had its times in the headlines, and there is even a Chinese auto bubble feared ready to pop! We aren't outright dismissing these stories as non-issues. They reflect a still-developing nation where the government, rather than the market, determines winners and losers-creating bloat and excess in certain sectors. However, these issues alone haven't derailed China's economy yet. Nothing about the country's economic prospects have radically changed, so we find it unlikely the same issues trigger problems now.

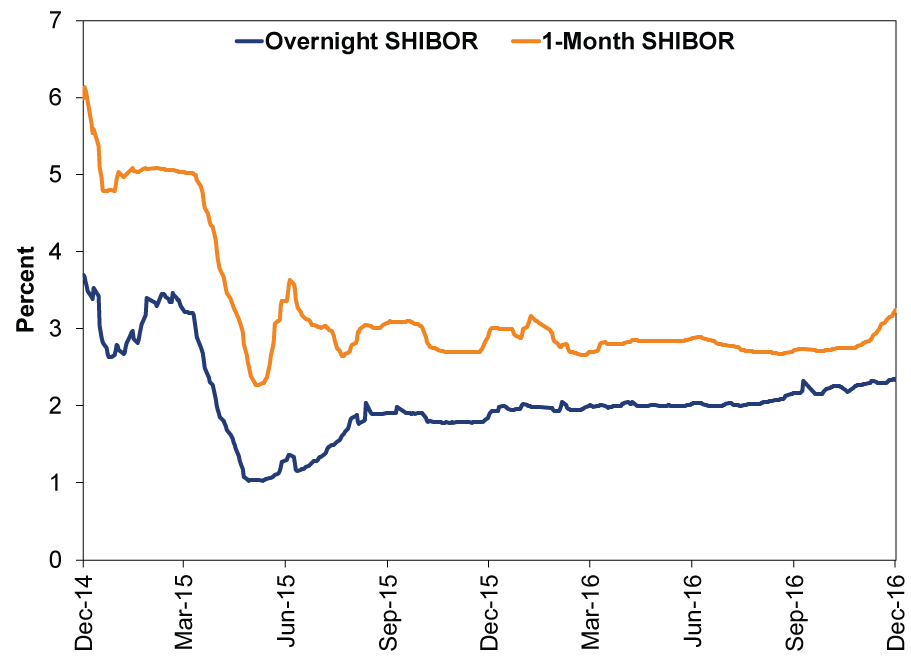

A lot of the coverage of this homes in on SHIBOR, HIBOR and other short-term measures of bank funding rates, claiming this shows banks are under stress. In a developed market with a liberalized financial system, that could be a telling sign of trouble. But China isn't one, and its $3 trillion in reserves and historical willingness to recapitalize banks suggest fears over what amounts to a fairly small wiggle by historical standards isn't the telling sign of trouble some think. Exhibit 1 shows the last two years' wiggles. We'd take it back further, but the swings get so much larger that these moves are obscured.

Exhibit 1: Overnight and One-Month SHIBOR Rates in Perspective

Source: FactSet, as of 12/23/2016. 12/22/2014 - 12/22/2016.

From a broader perspective, China's 10-year yield's recent rise isn't an isolated phenomenon-sovereign debt yields are rising globally.

Exhibit 2: 10-Year Yields on Sovereign Debt From October 24 - December 23

Source: FactSet, as of 12/23/2016. "Today" yields are as of 12/23/2016.

Which brings up another important point: The bond market, just like the stock market, can be volatile in the short term too. The movements aren't always as dramatic, but they can bounce around on a day-to-day basis. This is particularly true in a non-free-market nation like China, which frequently seems to struggle with growing pains.

And while rising yields pressure struggling firms-see one brokerage firm that missed a bond transaction earlier this week-defaults in China aren't exactly new news. The government has been dealing with them ever since a solar company couldn't make an interest payment back in 2014. Though letting these lagging firms fail would positively allow for greater market influence, the government has preferred helping out struggling businesses instead. That's a minor setback for China's stated long-term goal for greater economic liberalization, but the point is economic, and hence, social stability-always the Communist Party's goal.

China has plenty of resources to support that goal, too. One major tool: providing liquidity. China's central bank, the People's Bank of China, injected a net $6.5 billion into the interbank market last week to address potential liquidity issues. It also lent about $57 billion to 19 financial institutions via its medium-term lending facility (MLF) in mid-December. For the year, the PBOC has injected a net $221 billion into money markets, dwarfing the $1 billion from 2015.

Providing liquidity and using targeted stimulus measures have been China's preferred methods to spur growth and maintain economic stability, and this doesn't look likely to change any time soon. At China's annual Central Economic Work Conference, officials reiterated this emphasis. As one government adviser said, "The top priority is on maintaining growth while controlling risks. The promised restructuring of the economy will be carried out, but only when overall stability is ensured." While this suggests reforms have been deemphasized a bit, they probably continue at a slower pace and are more dependent on the broader economic outlook.

However, maintaining the status quo hasn't been bad for China, let alone the broader global economy. Yet folks seem to hold that weakness in certain sectors or parts of the economy portend huge negatives that will cause China's economy to finally crash. Call us optimists, but reality isn't nearly that dire. Firms delaying bond offerings seems more like disciplined restraint rather than zealous, reckless behavior. Even if some firms miss some bond payments and default, that needn't set off broader troubles. Despite its tough talk, the government has quietly lent its support when needed. So while headlines continue fretting China through the present holiday season, we suggest investors pay little heed to this particular ghost of the past.

[i] Or perhaps some votes in the UK and US overshadowed things?

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30 -

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today