Personal Wealth Management / Market Analysis

China’s Growth: Slower, But Not Slumping

Chinese economic data continue to be in line with longstanding trends, contrary to fears of a sharp slowdown.

Volatility in Chinese domestic A-share stock markets-largely off limits to non-Chinese investors-continues to garner headlines, fanning fears China's economy is about to plunge off a cliff and land with a splat. These fears hit fever pitch in August, when Chinese weakness was widely considered to be the cause of the recent global market correction. However, as we've documented, Chinese stocks aren't a reliable gauge of future economic conditions. One must dig deeper and, with August data starting to hit the airwaves, it seems to have been fear of Chinese weakness that stoked volatility, not reality. Economic data from August aren't showing a sharp slowing.

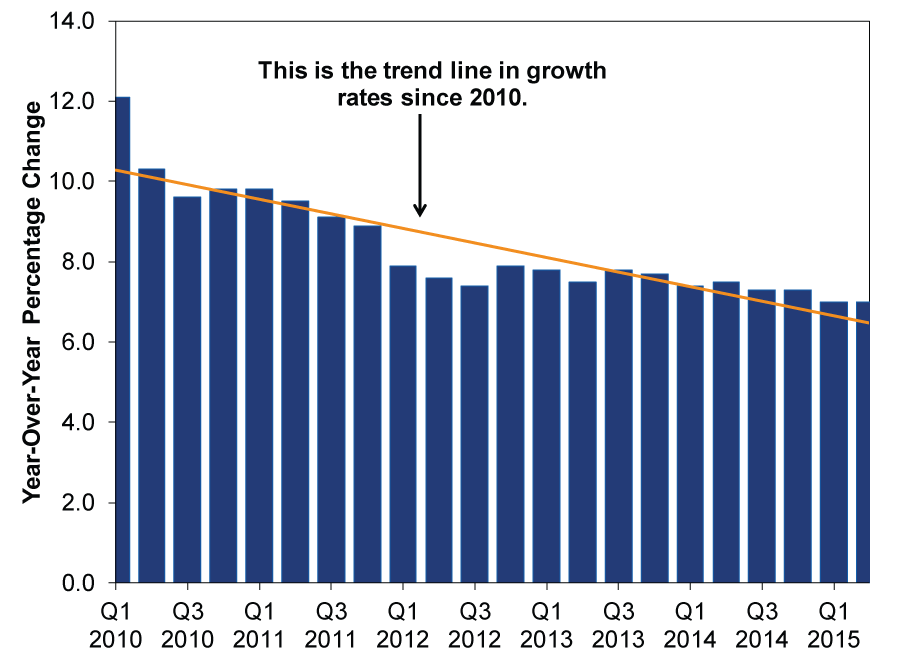

To be sure, China's economy isn't growing at the rapid, double-digit rates of 2010. But there is a reason we called them the "rapid, double-digit rates of 2010." That was the last time they happened. Since then, Chinese growth has gradually slowed amid the government's planned shift from a heavy industry- and infrastructure development-led model to a services- and domestic consumption-led one. Exhibit 1 shows GDP since Q1 2010, illustrating the slower-growth trend.

Exhibit 1: China GDP Q1 2010 - Q2 2015

Source: FactSet, as of 9/15/2015.

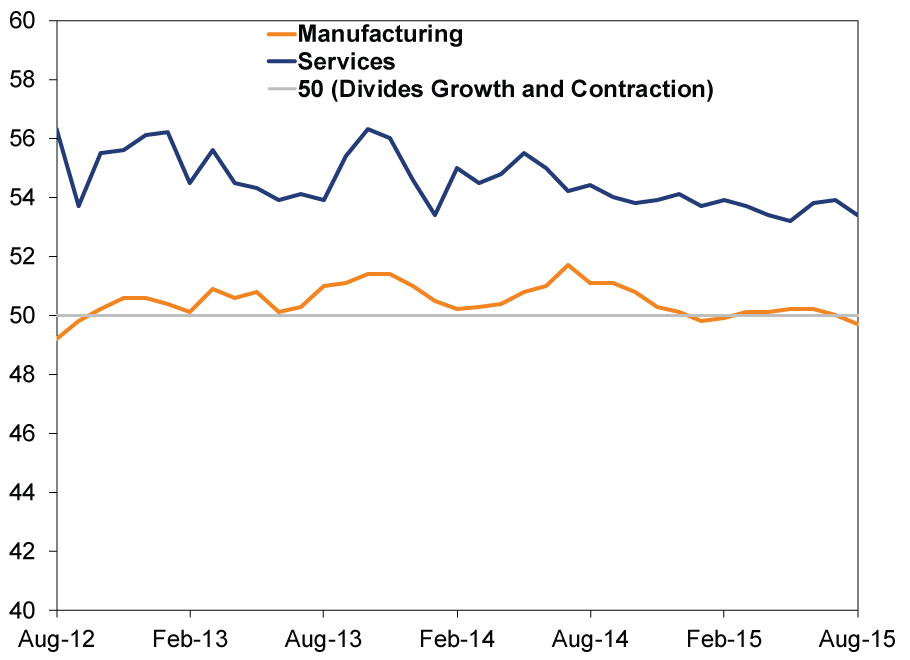

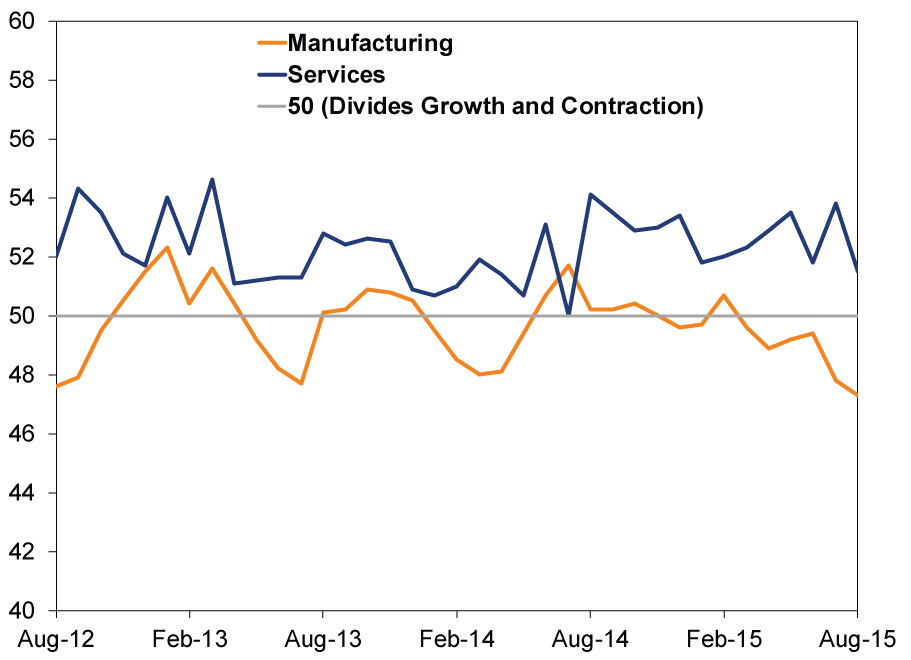

This echoes the longstanding slower-growth trend in other economic series, like both China's Official Purchasing Managers' Indexes (Exhibit 2) and the Caixin/Markit Purchasing Managers' Indexes (Exhibit 3). Recent readings aren't showing growth diverging from established trends.

Exhibit 2: Official China Purchasing Managers' Indexes

Source: FactSet, China National Statistics Bureau, as of 9/15/2015.

Exhibit 3: Caixin/Markit China Purchasing Managers' Indexes

Source: Bloomberg, as of 9/15/2015.

Monday, China released its slate of August data, and here too the figures were overall in line with long-established trends.

While it missed expectations, industrial production ticked up slightly to 6.1% y/y growth from July's 6.0%-right in line with where it's been all year. Fixed asset investment (a gauge of capital expenditures, notably including infrastructure investment) slowed to 10.9% y/y from 11.2%. This figure, which you would expect to be heavily influenced by China's shifting growth strategy, has slowed markedly over the course of the last three years (it's down from 16.5% a year ago), but recent downshifts don't show sharp or sudden deceleration. Retail sales grew 10.8% y/y in August, slightly beating estimates and accelerating from July's 10.5%. Trade data were mixed, as exports fell less than estimated but imports fell sharply (-13.8% y/y). That said, imports' decline seems mostly a function of commodity prices, a point underscored by data showing July apparent gasoline consumption and refiners' output rose 17.0% y/y and 6.5% y/y, respectively. None of these data seemingly suggest a economic conditions are markedly and suddenly deteriorating.

That said, these are all Chinese economic data, which many in the press lately have noted are questionable, like this roundup of skeptics The Wall Street Journal gathered Monday. And some skepticism seems fair, particularly considering the widely publicized mismatches between regional and national figures. Last week, China's National Statistics Bureau announced it would amend its calculation method to match the IMF's preferred methodology for calculating GDP, possibly targeting these concerns. Who knows if the skeptics will be placated, but from our perspective, there are plenty of ways to assess China beyond official data. For one, you can hear it from executives of firms doing business in China. Second, from a trade perspective, you can look to data published by their trade partners-like recent data from Australia's Port Hedland, a major commodities export hub. August exports to China from the terminal rose nearly 6.0% y/y to a record high.

To us, there are few signs recent weakness in Chinese domestic stocks is signaling material trouble in the world's second biggest economy. Stocks have long since dealt with notion of a slower-growing China, and there isn't anything we've seen lately that suggests to us a sharp deterioration has arrived.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Fed Rate Decision, US-Iran, Inflation in Europe

2026-06-19

2026-06-19 -

Market Analysis Reviewing Q1 Earnings and What Q2 Expectations Say2026-06-18

-

Market Analysis Kevin Warsh and the Magical Delete Button2026-06-17

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today