Personal Wealth Management / Economics

Cozying Up to Negative Yields

Uncertainty tied to negative yields has fallen.

Familiarity might breed contempt in some cases, but as it pertains to negative interest rates, it seems more like it is reducing uncertainty.

In early 2016, following the Bank of Japan's announcement it would cut its main overnight rate below zero, negative interest rates (curiously) became one of investors' primary sources of angst. As was often noted, there is little history of central banks cutting rates below zero, so there isn't much precedent to guide one's expectations. Hence, uncertainty.

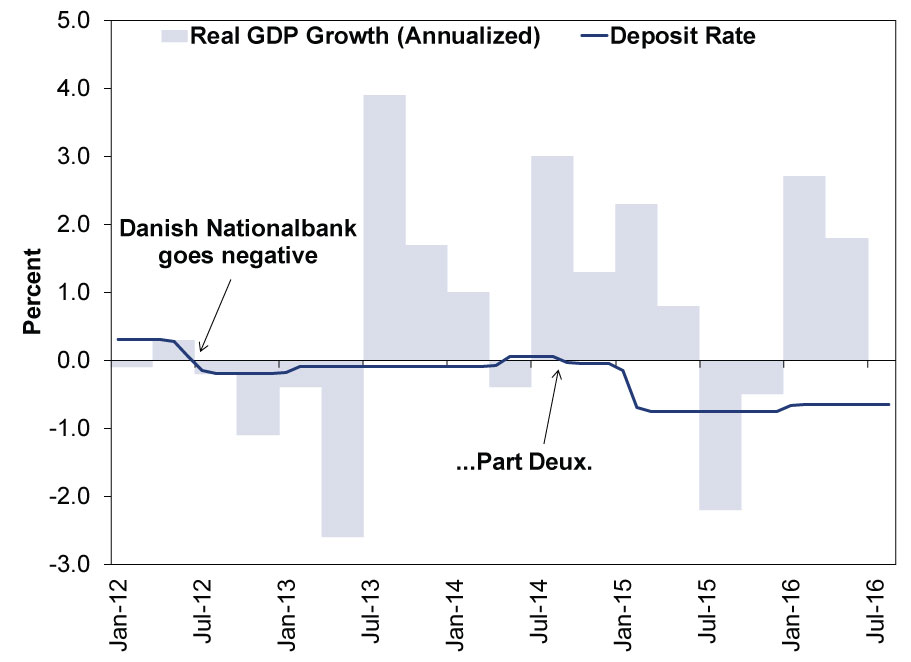

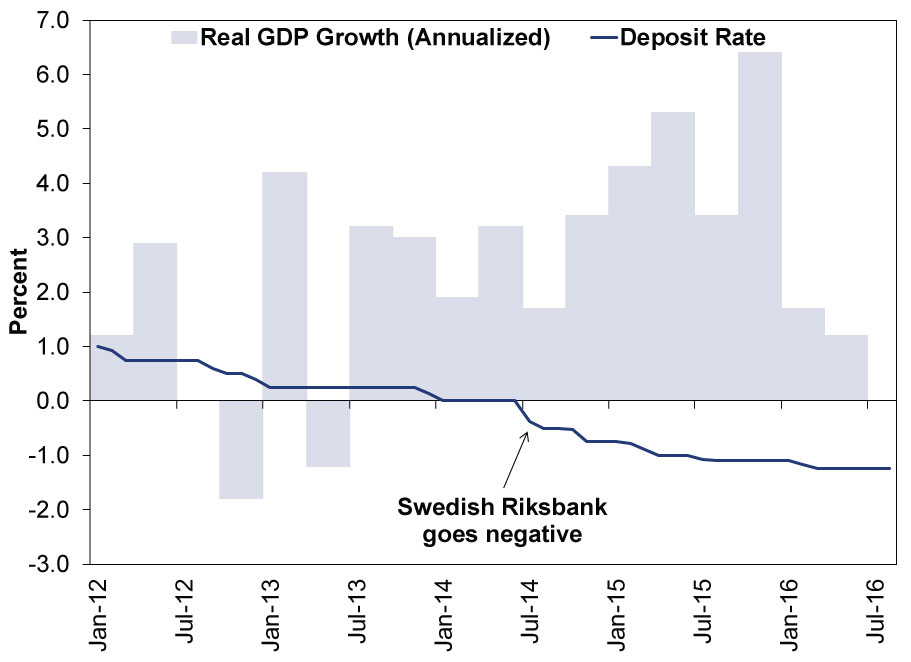

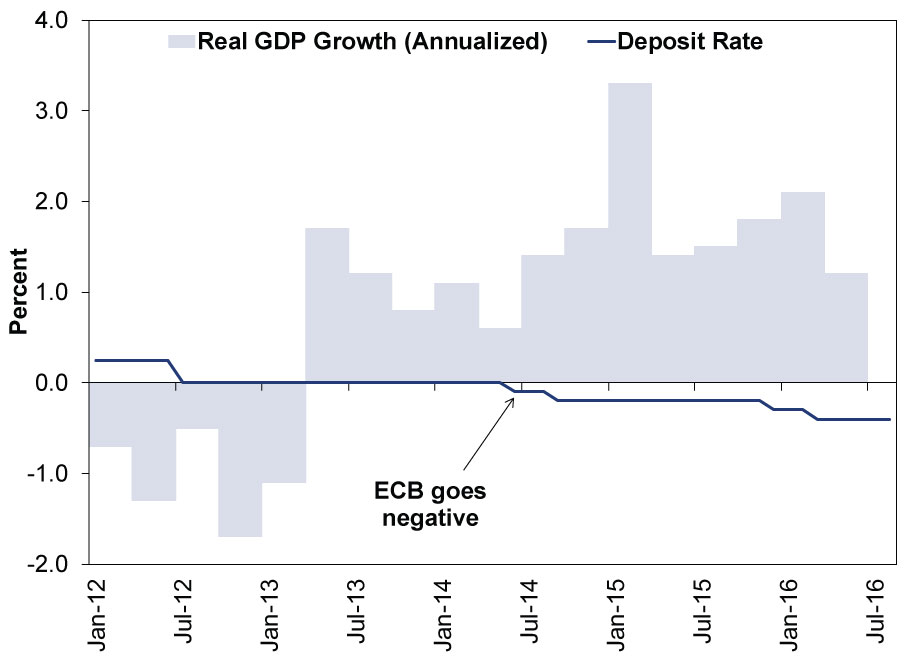

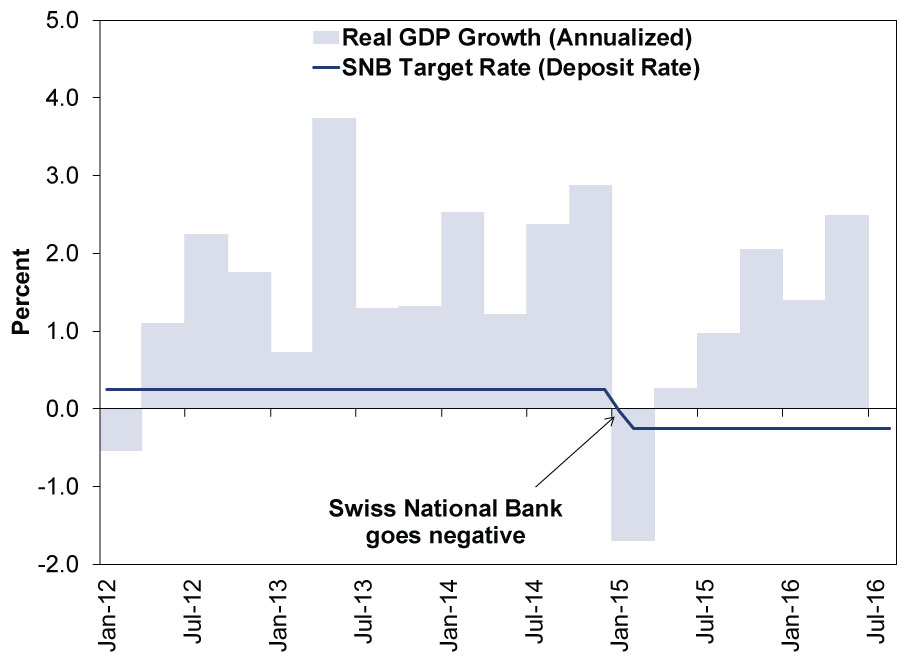

Now, that is all understandable enough except the timing, which is why we say it "curiously" drew investors' ire. Japan wasn't the first country to implement negative rates. It wasn't even the second, third or fourth. After all, Denmark first cut deposit rates into negative territory in July 2012. After briefly returning to positive territory in early 2014, Denmark again went negative that September. The ECB cut rates into the red in June 2014 and Sweden followed suit a month later. In early 2015, Switzerland announced a negative interest rate policy (NIRP). Yet none of these moves seemed to garner the media furor that accompanied Japan's moves this year.

That would perhaps be understandable if there were evidence negative rates, when tested in Europe, had directly attributable negative consequences. However, there isn't. Exhibits 1 - 4 show GDP growth since these central banks went negative.

Exhibit 1: Denmark Deposit Rate and GDP Growth (Annualized)

Source: FactSet and Eurostat, as of 9/8/2016. January 2012 - August 2016. Q3 2016 growth isn't out yet because Q3 isn't over.

Exhibit 2: Sweden Deposit Rate and GDP Growth (Annualized)

Source: FactSet and Eurostat, as of 9/8/2016. January 2012 - August 2016. Q3 2016 growth isn't out yet because Q3 isn't over.

Exhibit 3: Eurozone Deposit Rate and GDP Growth (Annualized)

Source: FactSet and Eurostat, as of 9/8/2016. January 2012 - August 2016. Q3 2016 growth isn't out yet because Q3 isn't over.

Exhibit 4: Switzerland Target Rate and GDP Growth (Annualized)

Source: FactSet and Swiss State Secretariat for Economic Affairs, as of 9/8/2016. January 2012 - August 2016. Q3 2016 growth isn't out yet because Q3 isn't over.

Denmark's initial move in 2012 occurred amid the broader euro crisis (which predated negative rates) and, given the country's tight trade ties to the 19-nation bloc, it's unsurprising GDP was contracting at the time. Hard to pin that on the Nationalbank's move. Excluding that, economic growth has been mixed since negative rates were enacted. In Sweden and the eurozone, economic growth has been consistently positive since the Riksbank and ECB went negative. Swiss growth did dip into negative territory coincident with negative rate implementation in early 2015, but there is an additional factor that seems potentially responsible: The country surprisingly broke the euro/franc peg in January 2015. In the five quarters since, growth has been positive.

Now then, just because growth has been overall fine doesn't mean negative rates are positive.[i] They are negative![ii] But a small negative. You see, central banks conjured them up as a means to goad banks to lend excess reserves-a tax on idle funds parked at central banks. The theory is these moves would stimulate growth by encouraging banks to lend excess funds, hence avoiding the charge. But that isn't banks' only option. They could buy bonds-sovereign bonds, foreign sovereign bonds and more. And that seems to be what happened, weighing on longer-term interest rates globally.

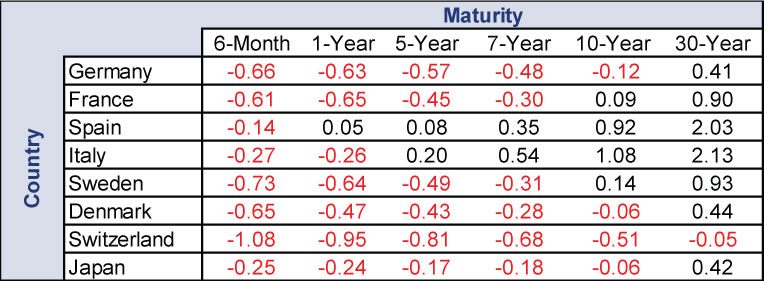

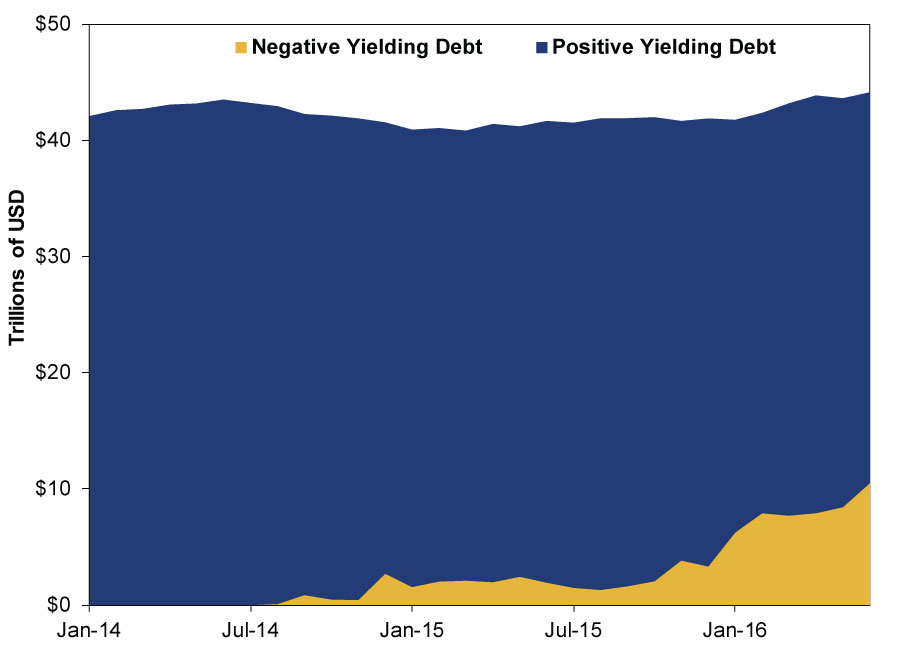

As a result of these policies, many sovereign bonds (and a couple high-grade corporate issues) have fallen into negative territory as well! German sovereign debt is currently "paying" a negative rate through 10-year maturities. French through seven years. Swiss sovereign yields are negative through 30-year maturities! While Japan has had negative yields since early this year only, sovereign bond yields are broadly negative there, too. Exhibit 5 shows selected bond yields across countries with central banks that have implemented NIRP. As Exhibit 6 shows, the amount of negative-yielding sovereign debt exceeding one year maturities has grown substantially since 2014.

Exhibit 5: Selected Interest Rates in Nations with Negative Yield Policies

Source: FactSet, as of 9/8/2016. All rates as of 9/7/2016 and in percentage points.

Exhibit 6: Negative Yielding Sovereign Debt Becoming More Common

Source: Fisher Investments Research, Bloomberg, as of 7/15/2016. January 2014 - June 2016. BofA Merrill Lynch Global Fixed Income Markets Index, monthly breakdown of yields on bonds exceeding one year in maturity.

The media and punditry frequently approach this increasing occurrence of negative yields with alarm, as though it's a gathering storm. But their (often loudly expressed) opinions help markets gain familiarity. If this were a calamity, liquid asset classes outside bonds would likely already reflect that. Yet they don't.

It seems more likely to us the increasing familiarity, combined with the lack of a negative-yield driven disaster, has reduced uncertainty and fears tied to them. After all, many feared negative rates for their newness. Now, they're less new.[iii]

[i] In the good or bad sense, not the above or below zero sense.

[ii] Ha!

[iii] PS: Many seem to fret the implementation of negative yield policy in the US, although this seems rather out of step with economic data and fedspeak, which suggest rates heading up not down. In addition, Fed head Janet Yellen didn't even mention negative rates as a potential crisis-fighting tool in her recent Jackson Hole address on the subject of the Fed's toolkit. Doesn't mean they'd never do it, but we wouldn't bet on the Fed going negative any time soon.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today