Personal Wealth Management / Politics

Debt Ceiling Episode CXI: Return of the Revenge of the Son of the Debt Ceiling and the Temple of Doom Strikes Back, Part Deux

Congress might not repeal the debt ceiling, but they'll almost certainly raise it for the 111th time.

Summer is here, which means it's time for bad movie sequels and clichéd analogies likening various things to bad movie sequels. So you can count on your friendly MarketMinder editors-with tongue firmly in cheek-to bring you an article about the debt ceiling, everyone's favorite bad sequel, which is back in the news thanks to Treasury Secretary Steve Mnuchin's June testimony to Congress and lawmakers' loose plans to vote on an increase before their summer recess. We've gone through this song and dance-err, sorry, seen this movie-many times before. First politicians play hardball, then administration-types warn about the risk of default, then the media has a conniption fit about default, and on they go until finally they kick the can. We've already had the first and second steps, but interestingly, the media commentary this time around has a different flavor: We've seen a raft of editorials arguing for the debt ceiling to go the way of the dodo. Seems like a good idea to us! The debt ceiling has always been symbolic. It doesn't actually limit debt (which isn't a problem anyway) in practice, and failure to raise it doesn't do all the terrible things people fear it will. Might as well formally acknowledge it is an annoying heap of nothingness.

In the old days, Congress had to authorize every new debt increase. It worked for a while, but then a little thing called World War I happened, and Uncle Sam needed to mobilize. To speed the war effort, Congress allowed the Treasury to issue new debt at its discretion, without going to lawmakers for approval, as long as debt stayed below a certain amount. When debt reached whatever arbitrary limit they set, they'd simply raise it, and everyone would carry on as usual. The US did not borrow itself into oblivion, the Allies won the war, and all was good.

For a few decades, raising the debt ceiling was a boring procedural matter. But in the mid-20th century, politicians-ever the politickers-figured out voters weren't big on debt, and that positioning themselves as anti-debt crusaders allowed them to use the debt "limit"[i] as a tool to win concessions. And thus began the time-honored tradition of holding the debt ceiling hostage to use as a bargaining chip in other fights. Both parties-and pretty much all factions within them-are guilty of this, and we suspect you aren't invited to the "cool" parties on Capitol Hill until you can claim responsibility for setting off a debt ceiling fight. As a result, almost every time it comes around, we are all treated to a political circus. And when everyone is satisfied with whatever symbolic victory they can peddle to their constituents and lobbyist friends, they kick the can and go home.

This wouldn't be so annoying if, every time this boomerang comes around, they didn't make all those dire warnings about default. You know, "If we don't raise the debt ceiling, the Treasury won't be able to pay its bills, and we'll default and destroy America's creditworthiness and it will be the end of us, we tell you, the END!" If that statement were actually accurate, it would be one thing, but it isn't. In this context, "the Treasury won't be able to pay its bills" means "the Treasury will have to give IOUs to vendors, contractors and government pension plans." But Uncle Sam's failing to pay the cable guy for a month isn't a default. Default means one thing, and one thing only: failing to make principal or interest payments on government debt. That's it.

Failing to lift the debt ceiling will not force America to default. Actually, most evidence suggests it can't. The 14th Amendment, as interpreted by the Supreme Court, requires America to pay its debts above all else. As long as the Treasury has money coming in, it can't say "welp, sorry, can't pay the interest this month, we gotta pay the cable guy instead."

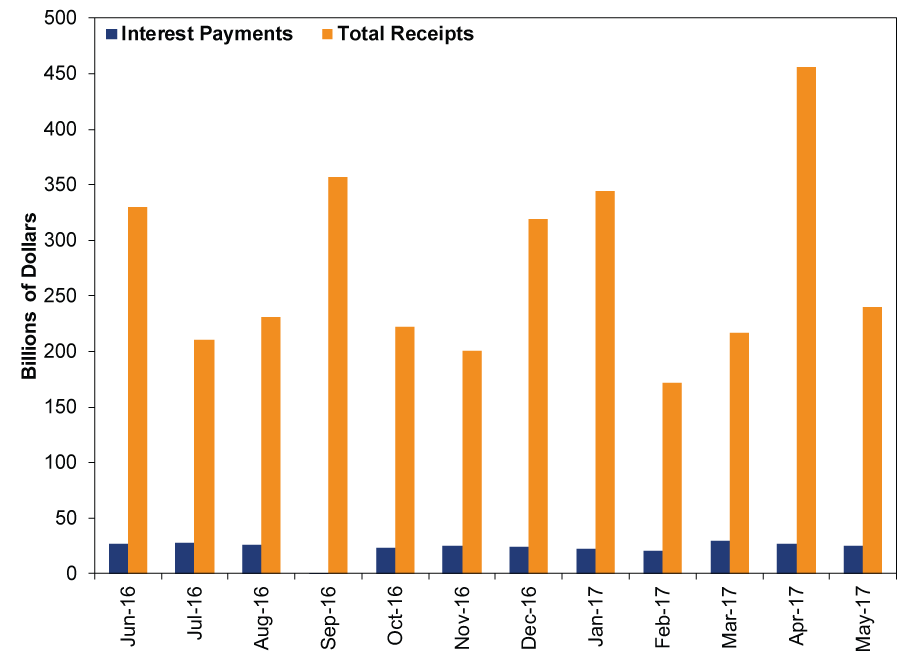

Repaying principal when debt matures is easy: Hitting the debt ceiling doesn't preclude the Treasury from issuing new bonds to replace maturing ones. Those cancel. So the key question is, does monthly tax revenue cover interest payments? The answer, as Exhibit 1 shows, is yes: Monthly revenues are so far above monthly interest payments that the Treasury can cover bondholders, pay all Social Security and Medicare benefits, and still have plenty left over other expenses (though they might stiff the cable guy in order to pay civil servants).

Exhibit 1: Monthly Tax Revenue Dwarfs Interest Payments

Source: US Treasury, as of 6/28/2017. Due to some accounting quirks, the Treasury reported paying -$17 billion in interest in September 2016, which would look very weird on a chart, so we chose to display it as zero.

Deleting the debt ceiling won't change anything for the US economy or fiscal situation. It might, however, improve sentiment by removing a regular source of uncertainty. After all, when Congress's debt ceiling fighting (and a math error) inspired Standard & Poor's to downgrade America's credit rating in 2011, it didn't change a doggone thing (interest rates fell, which tells you all you need to know), but the world collectively freaked out. It's probably fair to say it was a contributing factor to that summer's stock market correction-sentiment is the driving force of such sharp, fast moves. We favor relieving investors of one source of angst.

But we aren't holding our breath or anything. While sentiment seems to be drifting in favor of throwing the debt ceiling down a reactor shaft with Emperor Palpatine, politicians really seem to like it. They are generally loath to surrender anything they think they can use to score points. So we're mostly resigned to living with it. But still, wouldn't it be nice.

[i] Ha!

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13 -

Market Analysis Due Diligence and the DOL’s DOA Fiduciary Rule2026-03-13

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Market Analysis Rounding Up Odds and Ends From Global Energy Developments2026-03-11

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today