Personal Wealth Management / Behavioral Finance

Dollar-Cost Averaging Doesn’t Pay

Taking the lump sum and putting it to work right away is far more effective.

If you have a sum to invest, what is the best way to go about it: All at once, or more of a drip feed? In recent days, we have seen a couple of articles arguing that, while historical data give the lump-sum approach the edge, it is still more beneficial to invest slowly, using a method called “dollar cost averaging.” Their argument? While investing a lump sum at once may work best overall and on average, you can’t know whether it will work this time, so do a little at a time to reduce volatility’s impact on your returns. Appealing as this might sound, we think it risks leading investors astray and ignores some key factors. As the old saw goes, time in the market, not timing the market, is what matters. Since short-term volatility is unpredictable, and reaping bull market returns requires being invested during bull markets, we think the lump-sum approach is wisest.

Now, if you are contributing steadily to a 401(k), you have no choice but to dollar-cost average (presuming you make steady, automatic contributions). So no need to change your approach. We are talking solely about folks who have a lump sum ready to invest now (or ever) and are deciding whether to pour or drip.

For these folks, dollar-cost averaging “works” primarily only in very specific circumstances—namely, when markets endure a deep, lasting downturn during the period you are gradually investing the funds. This is why some argue it is a better way to take advantage of potential market volatility than just buying in. According to their logic, it gives you the benefit of being invested if/when the market rises and being able to buy at a relative low if it falls more. Trouble is, volatility isn’t predictable. If you use dollar-cost averaging in a great year without a deep drop, like 2013 or 2017, it is a setback. Plus, volatility moves in both directions. Cutting out the downside can easily mean missing out on the upside, especially if you are putting money to work during a bull market. Besides, dollar-cost averaging also drives up transaction costs and makes tax prep nightmarish after you sell if you aren’t investing in a tax-deferred account. If you are using individual stocks, then it can also impede diversification. Splitting up available cash makes it difficult for most folks to buy a sufficient number of individual stocks to get broad exposure and reduce company-specific risks.

In our view, unless you have sound reasons to believe a bear market is underway, if you have cash and need equity-like results for some or all of your portfolio, the best time to invest is always “now,” not “later” or “slowly over the next year or two.” Over decades-long time horizons, gains missed during the period when you are dollar-cost averaging can limit your total return. According to one study weighing the pros and cons of “immediate” (lump-sum) vs. “systematic” (dollar-cost averaging) investment, investing immediately in a 60% stock and 40% bond portfolio outperformed by 2.4 percentage points on average over a rolling 12-month basis. In terms of frequency, 68% of the time lump-sum returns outpaced investing in 12 equal monthly installments. Over a 36-month window, lump sum outperformed 92% of the time. Now, this study’s 2.4 ppt lump-sum advantage is a historical lookback (January 1926 – December 2015) using US equity and bond benchmarks. For the UK it was 2.0 ppts during January 1976 – December 2015, and for Australia it was 1.5 ppts during January 1984 – December 2015. In a separate study using an all-equity portfolio benchmarked to the S&P 500, lump-sum investing’s average annual returns were 1.1 percentage points higher than using dollar-cost averaging between 1926 and 1990—cutting out the 1990s’ decade-long bull—but with a similar two-thirds beat rate. While these figures may seem negligible, small differences add up over time.

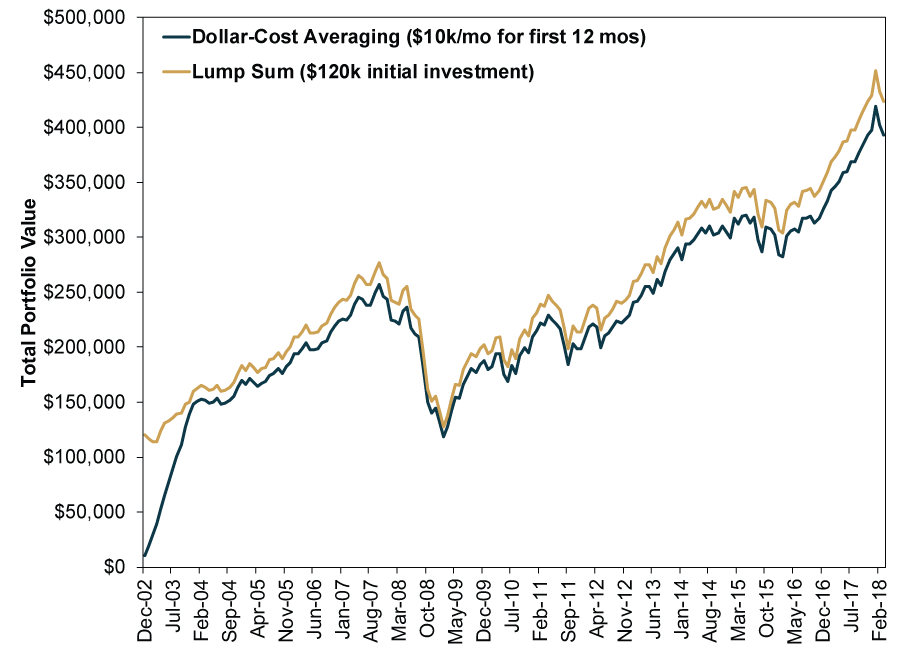

To show this, Exhibit 1 displays two hypothetical portfolios belonging to two imaginary investors who had $120,000 to invest in global stocks on December 31, 2002. At the time, the global bear market had been over for nearly three months, but stocks were about to retest the low with a steep early-2003 correction that ended in mid-March. Lump-Sum Sally bit the bullet and invested her entire $120,000 on day one. Dollar-Cost Danny decided to be more careful and invest $10,000 on the last day of each month—12 installments, with the first on New Year’s Eve 2002 and the last on November 31, 2002. We will assume each bought the MSCI World Index, reinvested dividends, and stayed perfectly disciplined through every correction and even the 2008 bear market, enduring the full pain but participating in the rebound.

Exhibit 1: Hypothetical Comparison of Lump-Sum Investing and Dollar-Cost Averaging

Source: FactSet, as of 4/24/2018. Based on MSCI World Index monthly returns with net dividends, 12/31/2002 – 3/31/2018.

By the end of last month, Lump-Sum Sally was ahead by $30,683.97—that is a hefty price for Dollar-Cost Danny to pay for feeling careful in a volatile stretch. Note, too, how the margin got wider over time due to compounding. If we were to extend the comparison out from here, presuming an 8% annual return (below world stocks’ long-term annualized average since 1926) for every year from 2018 through 2028—ridiculous straight-line math with no real-world bearing, but illustrative—the gap would widen to $72,518.62. Missed returns add up. The lesson: Lump-sum investing likely leaves more in the piggybank if you have a lengthy time horizon, take a diversified approach, have the discipline to keep at it and some patience.

The market—and the power of compounding—can’t work for you unless you are invested. The longer your money isn’t invested during a bull market, the further you will likely be from reaching your financial goals. If the volatility you are trying to mitigate never arrives, then you have shot yourself in the foot. There are times you don’t want to just buy in—but that is when you expect bear. And in that case, we would suggest dollar-cost-averaging isn’t a great solution either.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Upcoming IPOs, US Jobs Data, Credit Card Delinquencies

2026-06-05

2026-06-05 -

Market Volatility Seek Perspective Instead2026-06-05

-

Market Analysis No Flowers for the May Jobs Report?2026-06-05

-

Expert Commentary The US Midterm Campaign Trends Ken Fisher Is Watching

2026-06-04

2026-06-04

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today