Personal Wealth Management / Economics

Don't Dump on Durable Goods

A -7.3% drop in durable goods isn’t great, but plenty of other evidence suggests demand remains firm.

Astronomers operate a durable good in 1673. Source: Hulton Archive/Getty Images.

Durable goods orders got whacked in July, falling -7.3% m/m. Headlines near-universally bemoaned the apparent demand drop, but in our view, plenty of evidence to the contrary remains. One bad month in a volatile category doesn’t outweigh the countless other signs of growth—and durables gloom just gives the US economy one more way to exceed investors’ expectations looking forward.

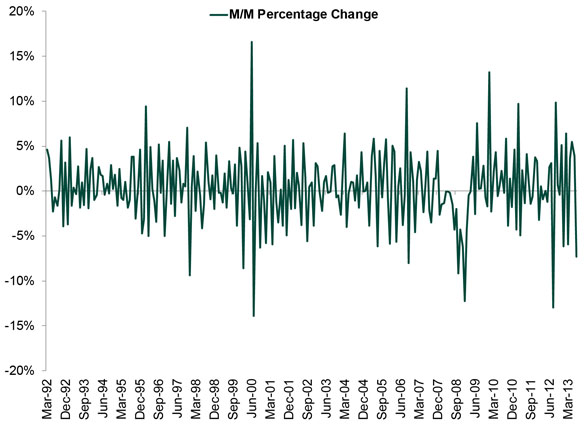

In a vacuum, July’s drop is big—but in proper context, it isn’t. For one, durable goods are one of the most volatile metrics—big swings in both directions are normal, and big drops one month don’t inherently signal further weakness. Orders fell a far bigger -12.9% in August 2012, then bounced 9.8% in September. January 2013’s -6.1% drop was followed by February’s 6.4% rise. As far back as data are available, results have been similarly choppy (Exhibit 1). That isn’t to say orders automatically rebound big next month—it merely seems premature to assume they’ll tank from here on.

Exhibit 1: M/M Change in Durable Goods Orders

Source: Federal Reserve Bank of St. Louis, as of 8/26/2013.

Plus, headline growth doesn’t tell the full story. As is the case with most major economic releases, one must assess the underlying components to get a complete picture. Headline durable goods are typically skewed by transportation orders, which tend to be the most volatile component. Strip those out, and orders declined only 0.6% m/m and are up 5.9% y/y. Even more telling, order backlogs remain elevated, and order levels remain well above shipment rates. This suggests there remains plenty of room for production and shipments to accelerate—especially with sales rising and inventories shrinking in the US and globally.

This brings up an important reminder for long-term growth investors: No one data point, however robust, can perfectly capture the economy’s health. Often, one series can’t even capture its narrow category. Were it otherwise, we probably wouldn’t have multiple means of measuring unemployment, like weekly jobless claims, the ADP and BLS reports, the Job Openings and Labor Turnover survey and others. Nor would we have multiple housing reports from the National Association of Realtors, National Association of Homebuilders and Case-Shiller. And we certainly wouldn’t have competing measures of new manufacturing orders.

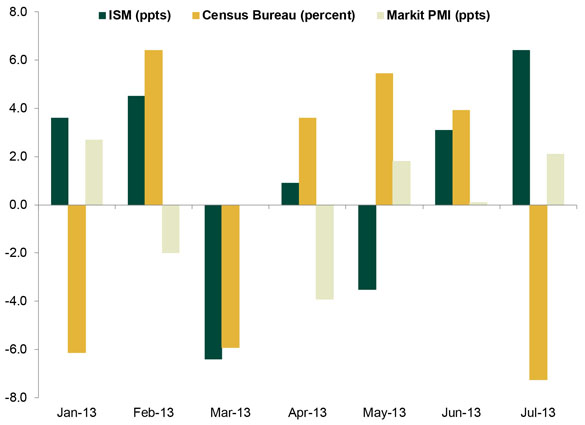

But we do! Three major national reports, to be specific. Along with the Census Bureau’s durable goods report, we have the ISM’s report and the new orders subindex of Markit’s manufacturing PMI, both of which rose just fine in July. ISM’s New Orders Index jumped 6.4 points to 58.3, the highest level since April 2011. Markit’s gauge accelerated too, rising 2.1 points to 55.5 (and, for good measure, added another point in August). The apparent disconnect isn’t unusual—the three regularly leap-frog each other (Exhibit 2). But on balance, they’ve pointed to order growth this entire year.

Exhibit 2: Monthly Changes in New Orders Vary by Index

Source: Federal Reserve Bank of St. Louis, Markit, as of 8/26/2013.

Another recent data release suggests more growth lies ahead: The Leading Economic Index rose more than expected in July. The two biggest contributors? The widening interest rate spread and the Conference Board’s proprietary Leading Credit Index (LCI). The latter aggregates swap spreads, Libor-Treasury spreads, margin debt, investor sentiment, self-reported bank credit availability and security buybacks—essentially a rough proxy of credit supply and demand. A high and rising LCI suggests loans are in-demand and banks are increasingly willing to extend them—and wider rate spreads add further incentive (read: fatter potential profit margins). This means more funds are available for businesses to invest in all sorts of growth-oriented spending—including transportation equipment, factory equipment, electronics and other durable goods. And with the yield curve likely steepening further as the Fed starts tapering QE, this trend could persist for some time.

Not that all is rosy in the US economy—there are always pockets of strength and weakness. But for now and looking ahead, the many areas of strength overwhelmingly outweigh the weaker corners, pointing to further growth.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

-

Interesting Market History Six Years On, Lessons From the COVID-Lockdown Low Endure2026-03-25

-

Market Analysis The Golden Paradox2026-03-24

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today