Personal Wealth Management / Economics

Dousing the Flame?

Has the UK’s Olympic torch been put out before the games officially commence? By some media accounts, yes—but Wednesday’s GDP print merits further examination.

This year was supposed to be one of celebration in the UK—from the Queen’s Diamond Jubilee to hosting the 2012 summer Olympic Games. Yet Wednesday may have dampened the mood some ahead of Friday’s Opening Ceremonies as it brought news the UK’s economy contracted -0.7% in the second quarter.

And not too surprisingly, the news tipped off an avalanche of media trepidation. For example, some bemoaned Britain’s longest double-dip recession in over 50 years. Others mused the UK’s apparent struggle to return to growth bodes ill for the rest of Europe (if not for the rest of the globe). After all, one would typically presume the UK is at least a bit removed from eurozone woes given its independence from the currency zone. So if the UK is struggling so much, what hope can there be for truly troubled nations like Spain or Italy?

Yet others used it as another opportunity to question austerity measures’ efficacy. A train of thought something along the lines of: “Well, if this is the outcome of significant government budget tightening and tax increases, the UK surely needs to hold off on any further such measures—and indeed reverse course some and loosen the belt a few notches.” (An analysis which surely applies by extension to other countries, like the US, to prevent a similar fate.)

But as ever, the devil is in the details—a particularly apt adage whenever discussing GDP—which merit further examination. According to the UK’s Office for National Statistics (ONS), part of the miss may be attributed to both bad weather in April and June and the fact the Queen’s Jubilee removed one working day from the quarter. The ONS also ascribed part of the decline to the services sector—but digging beneath the surface, it seems while private-sector services certainly shrank overall, the government recorded positive growth during the quarter. So much for that damaging austerity.

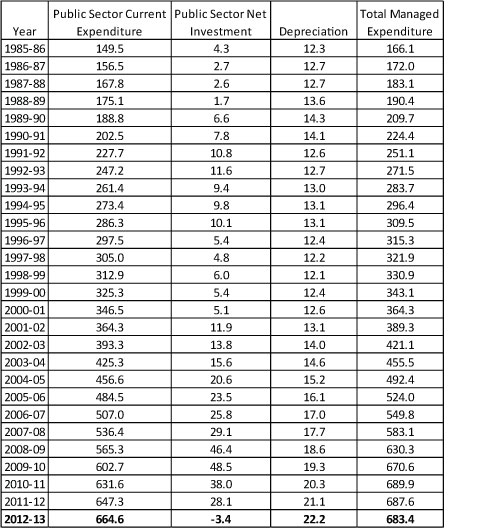

And indeed, going back further, it appears all the talk about austerity might exceed the reality by quite a margin. According to Her Majesty’s Treasury, government spending hasn’t shrunk once since 1985 (see Exhibit 1). To see austerity, one must include depreciation—and even then, total government expenditures were expected to shrink a very modest £2.3 billion between 2011 and 2012—making it near-impossible to attribute the recent contraction to any overwhelming decrease in government expenditures.

Exhibit 1: UK Public Expenditures (in billions of GBP)

Source: HM Treasury. Bold indicates projected numbers.

All of which makes suggestions “austerity” measures caused the UK’s double dip slightly head-scratching, to say the least. It seems, rather, the UK has yet to truly try austerity as typically defined—which usually involves some combination of government spending cuts and tax increases. Now to be sure, it’s not uncommon to hear politicians (of all stripes) discuss “spending cuts” when in fact they mean cuts in the rate of spending increases—an entirely different government action. And maybe UK politicians have been playing a similar game to curry political favor. Regardless of the motive, though, it seems hard to argue anything akin to draconian cuts often alleged by the punditry has been deployed in the UK.

Which would also seemingly suggest the UK (and others) could try austerity measures—granted, by a slightly different definition—and possibly see different results. Rather than seeing (thus far, non-existent) government spending cuts as the enemy, perhaps countries like the UK could actually rein in some government spending in an attempt to shift productive efforts to the private sector—which throughout history has proven itself the far more efficient economic engine. Maybe it could also consider measures reducing regulatory burdens on the private sector; maybe some tax cuts.

Essentially, we believe the goal of struggling economies globally should be spurring private sector activity by what means they can. Because despite the fact the government contributes to GDP, overall and on average, it is by far the junior contributor compared to the private sector.

So while the UK’s GDP print for Q2 is inarguably disappointing and the country struggling to regain its economic footing, it’s important to avoid being swept up in media proclamations it’s quite such dire news. On the contrary—the UK’s torch is still burning, and with appropriate steps, it can undoubtedly ultimately find its way to the podium’s top step.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Putting Negative Equity Risk Premiums in Proper Perspective2026-05-27

-

Economics A May Global Economic Check-In2026-05-26

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 18 - May 222026-05-26

-

In The News How to think about the Iran war — and what it means for oil and stocks2026-05-25

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today