Personal Wealth Management / Behavioral Finance

Dry Powder Doesn’t Pay

Waiting for a correction to buy stocks is a fruitless exercise.

For nearly two years, pundits argued a correction was overdue and investors should keep powder dry to wait for a better buying opportunity. That theoretical opportunity technically arrived Monday and Tuesday, when world stocks and the S&P 500 officially entered correction territory, falling more than -10% from their most recent peak. After the Dow plunged 1,000 points in Monday's opening minutes, a rush to trade caused outages at a couple big online trading platforms. Yet anecdotal evidence suggests more folks were clamoring to sell than buy, illustrating a valuable lesson: Waiting for stocks to go on sale might sound like a winning tactic, but it is exceedingly difficult to execute in the heat of the moment, when emotional instincts will likely work against you.

Unlike the last time global markets corrected (in 2012), many seasoned analysts and observers have come forth and proclaimed stocks are on sale right now. But still, even with waiting for one and with analyst counsel, it seems investors overall just don't react to a 10% discount at the NYSE the way they would at Bullock's or Woolworths. Consumers love low prices. So in theory, investors with idle cash should welcome stock market declines. But instead of lining up for door-busters, many flee. They don't see it as a temporary discount. Recency bias, presently fed by 2008 recollections, makes folks extrapolate the recent past forward, believing even worse times are ahead. For all the sage "stay cool" advice out there, many analyses of recent activity explore whether this is September 2008 or October 1987 all over again. Some claim China's selloff is a financial crisis in the offing and warn markets can go far lower. Others noted stocks still aren't cheap. Even where the verdict was inconclusive, the tenor and ghosts raised would have lured investors to some very fearful places. And with fear comes fear of more losses, something humans are hard-wired to feel much more acutely than gains. Thus the drop turns into a classic "fight or flight" moment, and for many, flight (or paralysis) wins. Hence, the paradox: The very sale many investors said they wanted arrived, but it still doesn't appear they wanted in.

This behavioral pattern is fairly typical of corrections. Fear and stock prices are negatively correlated. The further stocks fall, the more fears rise, turning it into a missed opportunity. Consider the scary stories circulating as this bull market's five prior corrections bottomed. The first ended on 2/8/2010, one day after former Fed head Alan Greenspan told "Meet the Press" stocks' quick drop was "more than a warning sign." Employment was still plunging, and most feared a double-dip recession. Greece was reeling, fueling fears it would take down the euro and maybe the world. Greece was also the word on 7/5/2010, the second correction's final day. Double-dip fears persisted as UK unemployment soared. In the US, analysts warned the charts resembled the Great Depression.

2011's first correction ended October 3, with pundits warning we were in or close to recession, with a catastrophic Greek default imminent, and encouraging investors to defend their portfolios. The second ended on November 25, amid more recession warnings and euro collapse dread as Spain teetered. When the bull's fifth correction ended on 6/4/2012, investors had to grapple with Chinese hard landing fears, warnings the Fed would be out of ammunition if the eurozone crisis triggered "a Lehman-like banking crisis," and worries tepid jobs growth foretold another dip.

Faced with all those headlines, and without the benefit of hindsight, what would you have done? Gritted your teeth and bought stocks? Or waited a couple weeks, just to make sure they would recover? For as much as investors know pullbacks are temporary, when they strike, they rarely feel temporary. So folks typically wait for confirmation.

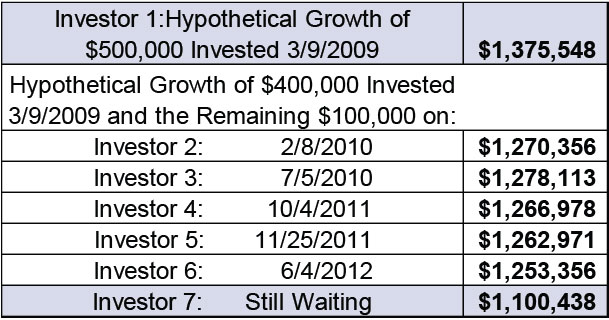

Waiting might feel better at the time, but it comes with a cost: Missed returns. Stocks often rebound quickly, and the sale can easily be over by the time you're ready to shop. Smarting from the missed opportunity, you might find yourself waiting for yet another pullback, vowing to play it better next time. Some folks end up with permanently sidelined cash they never feel ready to deploy. This opportunity cost is money lost, and it adds up over time. Heck, even timing these things perfectly isn't always worth the effort. Exhibit 1 tracks seven hypothetical investors starting with $500,000 when the bull market began on March 9, 2009. The first went all in-no dry powder. The second kept 20% in cash, then put it to work precisely when correction #1 bottomed. Investor number three deployed their dry powder at the second correction's trough, and so on-all the way to investor #7, who is still waiting. It may make investors feel better to keep some cash on hand to plow into stocks after they pull back-fulfilling part one of the mantra, "buy low sell high"-but much more often than not, this tactic diminishes your returns over time. Now, we know perfectly nailing the bottom of a bear market and corrections, as our scenario presumes, is unrealistic .[i] But this illustration does show waiting for clarity is costly!

Exhibit 1: Dry Powder Doesn't Pay

Source: Factset, as of 8/28/2015. MSCI World Total Index returns with net dividends. 3/9/2009 - 8/27/2015. Current value assumes $400,000 invested on 3/9/2009 and the remaining $100,000 invested on the date indicated and held until the present with no changes.

In our view, the solution is to think long term, and tune out the little voice promising dizzying returns if you hold back now in order to make a killing later. Reality rarely cooperates. Either the better buying opportunity never comes, or emotions prevent folks from recognizing it. Because human nature pulls us away from buying at exactly the time we should, for most it's likely best to keep it simple: Own stocks in a bull market, and accept that holding big sums of cash can make your goals that much harder to reach.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Expert Commentary This Week in Review | Energy Markets, Fed Meeting, Earnings Reporting

2026-03-20

2026-03-20 -

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today