Personal Wealth Management / Market Analysis

Economic Data Checkup

A look at the latest and greatest in economic data!

Eurozone GDP became the latest Q2 stat to get bumped up Tuesday, when growth was revised up from 0.3% to 0.4% q/q-not as striking as the US's Q2 GDP growth revision from 2.3% to 3.7% annualized, but not too shabby! Yet jitters abound that the party won't last, and many fear global growth is slowing, citing the latest Chinese data as signs of a weakening world. (The latest: August imports fell -13.8% y/y-widely feared as plunging Chinese demand, though plunging commodity prices bear most of the blame.) Despite these high-profile iffy numbers, however, there is actually plenty of evidence the world economy is growing just fine and should keep doing so, providing plenty of fundamental support for stocks.

We start with August Purchasing Managers Indexes, better known as PMIs-surveys showing the percent of firms that grew. As we highlighted last Tuesday, most of the world's manufacturing PMIs are above 50, signaling expansion. And the latest numbers show service sectors-the largest segment of most developed-world economies-are in even better shape. Eurozone August Services PMIs topped 50, with even the alleged laggard, France, registering growth. (Exhibit 1) US August non-manufacturing PMI came in at 59.0, with forward-looking new orders hitting 63.4-today's order's become tomorrow's output. Markit's UK August Service PMI clocked 55.6, while new orders slowed but still expansionary for the 32nd straight month. While PMIs measure the breadth of growth, not the magnitude, they show the biggest chunk of economic activity across more than half of global GDP is in fine shape. Strength there more than offsets the weak spots, primarily in commodity-reliant Emerging Markets. Tellingly, JPMorgan's Global Services PMI rose in August, hitting 54.4-up from July's 54.1 and the 35th straight month of expansion.

Exhibit 1: Eurozone August Services PMIs

Source: Markit Economics, as of 9/7/2015.

Since PMIs are surveys, feel free to take the prior paragraph with a grain of salt. But less-squishy statistics also show activity rising around the world. Few news outlets report on air travel, but passenger travel is a good sign of a growing economy. According to the International Air Transport Association, global passenger air traffic rose 5.7% y/y in June, bringing year-to-date growth to 6.3% versus 2014's first six months, with international traffic particularly robust. If the world were truly weakening, we suspect consumers would cut back on pricey discretionary things like splashy vacations. Trade also seems to be on an upswing, judging by North American intermodal rail traffic-shipping containers that move between different modes of transportation (ship, train, truck). Through August 29, intermodal volumes grew 3.3% year to date versus the same period in 2014. Total carloads are down, but this is deceiving: Each car can hold multiple containers, so the number of carloads isn't precisely telling about total shipping volumes. Focusing on intermodal units shows plenty of goods are sailing the seven seas, landing in North America, and traveling the country to reach consumers-and the reverse as containers travel from US factories to ports (and to Canada and Mexico).

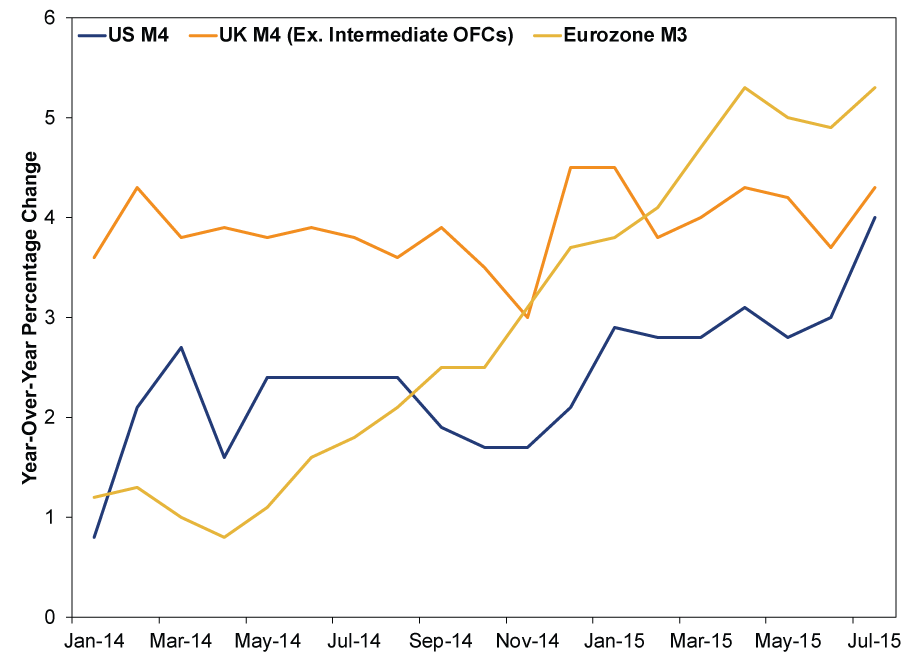

Forward-looking indicators appear strong, too. Broad money supply is growing nicely throughout the developed world (Exhibit 2). The broadest measures of money in the US, eurozone and UK accelerated in July, led by the eurozone at 5.3% y/y. As over a century of data and economic theory show, changes in the broad quantity of money tend to influence economic activity. If broad money supply is growing, that usually increases economic output as firms have more resources to expand and consumers have more money to spend. Rising money supply can also bring inflation, but as long as the quantity of goods and services rises, prices stay in check. This combination of moderate growth and benign inflation is often called a "Goldilocks" economy, and that's where much of the Western world is today.

Exhibit 2: Broad Money Supply Growth

Source: FactSet, Center for Financial Stability and Bank of England, as of 9/8/2015. Year-over-year growth in US M4, UK M4 (excluding intermediate "other financial corporations") and eurozone M3, January 2014 - July 2015.

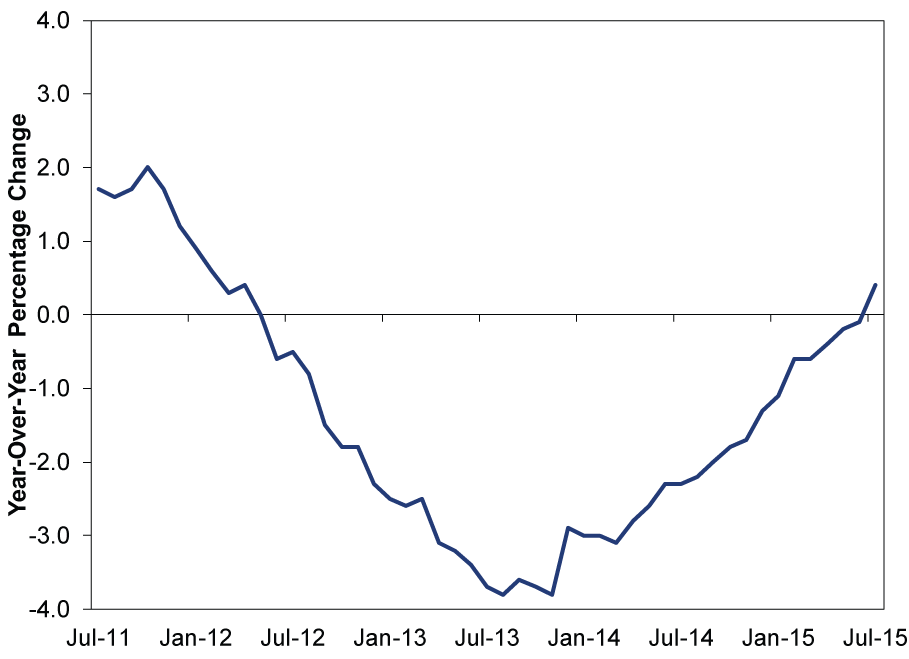

In most of the developed world, banks create the lion's share of new money by lending, which is in a strong uptrend. US business lending has grown 10% y/y or better since June 2014, and weekly growth hovered around 11% y/y throughout August. That means firms have ample financing to build factories, expand vehicle fleets, upgrade computer systems and equipment, launch new projects and research and hire more workers. All support growth. Eurozone business lending climbed 0.9% y/y in July, snapping a long streak of year-over-year contraction. With banks better capitalized after years of deleveraging and loan demand picking up, growth there should continue. (Exhibit 3) UK business lending, another long-running question mark, is also on an upswing as lending to small businesses (excluding overdrafts) rose 0.3% y/y in July-its fourth straight rise after years of decline. Much of that came via the Bank of England's "Funding for Lending" program, which saw strong results for the second straight quarter in Q2.

Exhibit 3: Eurozone Lending to Non-Financial Institutions 2012 - 2015

Source: European Central Bank, as of 9/7/2015. Eurozone lending to non-financial institutions, year-over-year percentage change, July 2011 - July 2015.

Not only are banks lending more, their strong profits position them well to continue supporting economic activity. According to the FDIC, US Q2 bank earnings grew 7.3% y/y as most legal and regulatory costs moved further into the rear view mirror. With costs more manageable and profits up, banks should have more flexibility to take risk and lend even more broadly. Strong profits also lets banks retain earnings to help comply with the higher capital requirements phasing between now and 2019, enabling banks to follow the new rules without mass deleveraging or crimping lending.

That you won't read about most of this on the Business section's front page is pretty telling about where sentiment and expectations are today. Bad news still gets most of the attention, and good news gets mostly overlooked, helping keep expectations low. Even though there are pockets of weakness throughout the world, reality likely exceeds too-dour sentiment, setting the stage for more bull market ahead.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Expert Commentary This Week in Review | Energy Markets, Fed Meeting, Earnings Reporting

2026-03-20

2026-03-20

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today