Personal Wealth Management / Market Analysis

Europe’s Great Policy Mistake

European tax hikes amount to repetition of a decades old error, potentially stirring unrest and extremism.

Ironically, Europe’s plan to save the eurozone could actually push it towards an eventual breakup at some point in the future. Of course, the irony goes even further, given the eurozone’s post-World War II birth was rooted in an attempt to avoid conflicts. Yet European policy makers today are making the same basic mistake made with Germany after World War I: Implementing cross-border economic policies that potentially foment anger, spurring the rise of extremism. Should the eurozone hope to hold together and avoid the rise of extreme nationalist parties—and the potential conflicts that follow—it needs to cut (rather than raise) taxes designed to impose “austerity.” Cutting taxes likely helps drive a more vibrant, competitive peripheral European economy. Hiking taxes in a bid to lower debt just for the sake of lowering debt likely results in the opposite: more stagnancy.

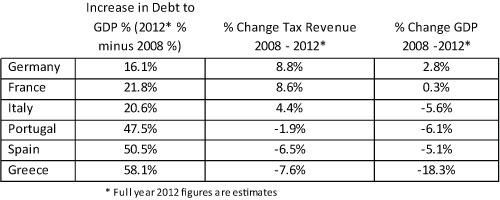

Just like Germany after World War I, Southern Europe now has extremely large debts with foreign creditors relative to the size of its tax revenue and GDP. Unfortunately, one aspect of the eurozone’s debt reduction plan is tax hikes. This is the reverse of what they should do, and instead of raising tax revenues, it’s exacerbating their relative debt loads as it hampers economic growth. And it weakens economic competitiveness, a core issue in peripheral Europe. (Exhibit 1 shows Southern Europe’s worsening debt-to-GDP ratios.)

Table 1: Declining Tax Revenue and GDP in Southern Europe

Source: International Monetary Fund.

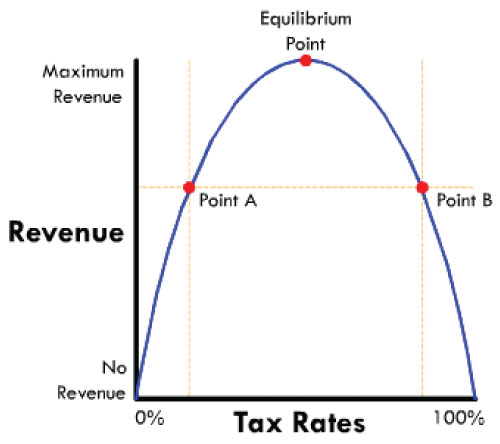

Economic theory perhaps best describes the current policy mistakes through the Laffer Curve. The Laffer Curve states there are always two tax rates (taxes in this case including both explicit taxes as well as regulatory obstacles) and corresponding levels of economic growth that generate the same tax revenue. The government can take a large percentage of a limited amount of economic output (point B in Exhibit 2) or a small percentage of a large amount of economic output (point A). The equilibrium point is where a government would maximize tax revenue.

Exhibit 2: The Laffer Curve

Source: Finance Society of the College of Business Studies.

Ideally, an economy would always be at or to the left side of the equilibrium point, generating a larger amount of economic output for a given level of tax revenue. However, Europe’s tax-raising austerity policies have clearly moved Southern Europe’s economies to the right of the equilibrium point—reducing both economic output and tax revenue. Refer back to Exhibit 1, which shows the economies being forced to undergo the most severe austerity measures (Greece, Spain and Portugal), showing negative GDP and tax revenue growth rates along with the largest increases in debt to GDP.

Instead of moving further right on the Laffer Curve, Europe should head left by cutting taxes and regulations. The more Europe implements higher taxes and greater regulatory burdens, the further Southern Europe’s economies and tax revenues appear likely to decline, reducing their ability to pay off their debts.

And as the economic contractions worsen from these policies, the populace undergoes further economic stress. And, pinning its stresses on the interference of the IMF, EU and ECB, it could sow seeds of discontent. Perhaps the populace first elevates a socialist party to increase the redistribution of funds, and then a nationalist party.

To understand why this happens, consider a single village composed of just three families. If one temporarily loses their ability to make a living, the others must decide whether or not to support them. If they do not share, the suffering family, facing potential extinction, may be forced to steal from or even attack the others in to confiscate their goods. In most cases, the rational response is to temporarily support the suffering family (socialist platform of redistributing income). It’s typically the least costly response.

However, if this doesn’t adequately help those unable to make a living, the suffering populace often looks to more extreme and even violent methods to defend and support themselves (extreme nationalist platform). Of course, this process only happens if the suffering populace makes up a large enough percentage of the total population to realistically threaten those with income. Thus, it typically takes a prolonged depression to trigger such events.

Post-World War I Germany exemplifies this well. Policies, some imposed on the Weimar Republic, others self inflicted, caused a decline in economic output and tax revenues. Then, the left leaning Social Democratic Party and Communist Party of Germany went from 21.7% and 2.1% of the vote, respectively, in 1920 to 29.8% and 10.6% of the vote by 1928. Unfortunately, they were unable to reverse the policies causing declining economic output and tax revenues, and in 1930 Hitler’s extreme nationalist party jumped to 18.3% of the vote from just 2.6% two years prior.[i]

Clearly, things are far from so extreme at this juncture in Europe today and they may never get there, since choices to avert these outcomes are clearly possible. But there are worrisome signs of rising extremism. Greece, hit hardest by the combination of economic dislocations brought by competitiveness issues, elevated debts and Europe’s tax-hiking fever, is most noteworthy. In Greece, the Coalition of the Radical Left (SYRIZA) party is now the second largest party in parliament, surging from 4.6% of the vote in 2009 to 27.1% in 2012. The extreme nationalist Golden Dawn party has also suddenly jumped from the fringe with 0.3% of the vote in 2009 to 6.9% in June’s parliamentary election. Furthermore, polls from September show Golden Dawn’s support continuing to increase, predicting the party would now garner 12% of the vote.

Should the current direction of economic policies continue, Golden Dawn and nationalistic parties in other Southern European countries could continue rising in prominence. If they gain the power to separate from the eurozone, one can only hope conflict does not follow.

[i]Dieter Nohlen and Philip Stover, Elections in Europe: A Data Handbook, Nomos Verlagsgesellschaft, May 2010.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

-

Market Analysis Rounding Up Odds and Ends From Global Energy Developments2026-03-11

-

Market Analysis Stablecoins Didn’t Eat the Treasury Bill Market2026-03-10

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today