Personal Wealth Management / Market Analysis

Eurozone Earnings Are Soaring

It's a bird, it's a plane, it's MSCI EMU earnings!

Throughout the eurozone's four-years-and-counting expansion, one thing has been missing: rip-roaring corporate earnings growth. But it is missing no more! Eurozone earnings soared in Q1, and analysts expect the party to last through 2017, with profits in the once-beleaguered currency bloc outstripping other markets. Accelerating earnings growth is not only great for stocks but, with revenues also rising, it's a sign the economy is on the right track. Mounting evidence suggests the Continent is healthy and likely to stay that way, which we believe sets up eurozone stocks for further outperformance.

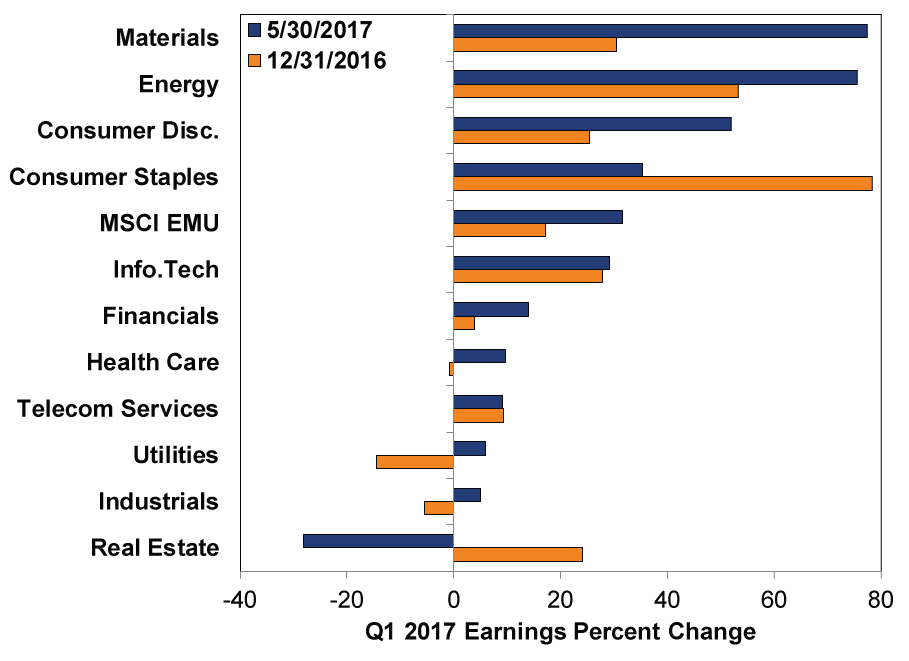

While eurozone stocks underperformed in recent years as earnings lagged, 2017 looks to be a turnaround year. And a gangbusters one at that. With 232 of 241 companies in the MSCI EMU[i] Index reporting, Q1 earnings growth is clocking in around 31.5%.[ii] That's up from the 17.1% analysts expected at 2017's start. (Exhibit 1) The sector breakdown shows Materials (77.4% y/y) and Energy (75.4%) earnings leading-similar to the US-mostly reflecting commodity and oil prices' brief bounceback from last year's Q1 lows. But excluding these sectors still reveals double-digit earnings growth in Consumer Discretionary (52.0%), Consumer Staples (35.3%), Information Technology (29.1%) and Financials (13.9%). Those don't look quite as impressive given the chart's scale, but they are all at or better than the S&P 500's 13.9% Q1 growth rate (9.8% excluding Energy). And with Health Care and Telecommunication Services earnings close to 10%, eurozone earnings growth is not only big, but broad-based.

Exhibit 1: First Quarter Eurozone Earnings

Source: FactSet, as of 5/30/2017. Q1 2017 year-over-year earnings growth estimates for the MSCI EMU Index and its sectors on 5/30/2017 and 12/31/2016.

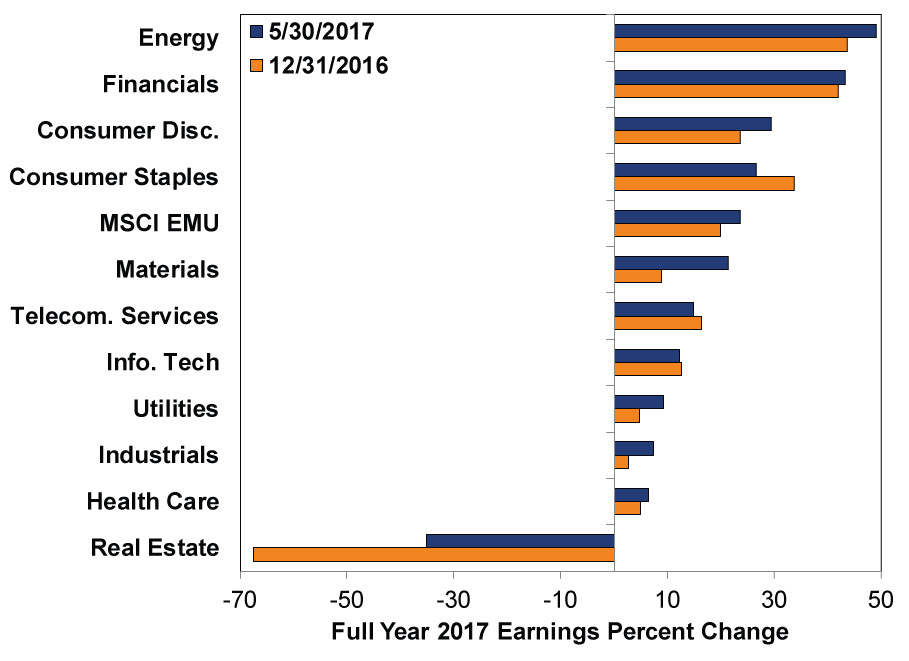

Meanwhile, full-year earnings estimates have risen to 23.6% from 19.8%. (Exhibit 2) Excluding Energy and Materials again, leading the charge are Financials (43.2%), Consumer Discretionary (29.5%), Consumer Staples (26.6%), Telecom (14.8%) and Tech (12.3%). Although there are still three quarters to go and these estimates are subject to revision, if earnings come anywhere close to these projections, that would be a powerful positive suggesting a rockin' year for eurozone stocks. But it isn't just analysts' expectations-which are often (too) optimistic-that suggest strong earnings. Sustained and broadening eurozone economic growth also indicates higher earnings ahead.

Exhibit 2: Full Year Eurozone Earnings Expectations

Source: FactSet, as of 5/30/2017. 2017 year-over-year earnings growth estimates for the MSCI EMU Index and its sectors on 5/30/2017 and 12/31/2016.

The eurozone's earnings surge puts the focus squarely on Continental economic improvement. The dominant media narrative on both sides of the Atlantic continues to emphasize a eurozone overburdened by debt and plagued by sclerotic institutions, economic stagnation and populist uprisings-with Germany the sole pillar of stability at the core. But this hasn't been true for a while. Eleven of 19 eurozone members are officially out of recovery-above their 2007 - 2008 GDP peaks-and notching new highs. Nations bailed out during the crisis are logging some of Europe's fastest growth rates and have been growing nicely for a long while. Portugal is the fastest-growing eurozone nation of those to report Q1 growth thus far. Spain is right on its heels. Pockets of weakness (ahem, Greece) persist, but overall and on average, growth is broader and faster than most give it credit for.

Even non-euro countries in Eastern Europe are rapidly expanding. (Exhibit 3) Though often overlooked and underrated, they're thriving members of the European Union common market, engaging in robust trade with the rest of Europe and driving demand for goods and services from the eurozone. With eurozone corporate earnings finally bouncing high, widespread economic strength is rightfully gaining more attention.

Exhibit 3: Even Eastern Europe Exceeding Expectations

Source: FactSet, as of 5/18/2017. All figures year-over-year.

Forward-looking indicators suggest eurozone economic growth should continue supporting earnings and stocks. The latest eurozone purchasing managers' indexes (PMIs) indicate overall business activity is at six-year highs and beating expectations. (Exhibit 4) Meanwhile, the Conference Board Leading Economic Index (LEI) for the Euro Area is accelerating-up 0.7% in April (the eighth straight rise) and 3.7% over the last six months, the fastest rise this year. This strongly suggests more robust expansion ahead. The eurozone's yield curve-the difference between long rates and short rates-is also bolstering financial conditions. It has steepened over the last year, boosting private sector loan growth as lending becomes more profitable (banks borrow short and lend long, pocketing the difference). Faster loan growth in turn has lifted money supplywithout increasing inflation, which remains modest, implying a Goldilocks economy firing on all cylinders. Credit is flowing and consumers are spending.

Overly cautious sentiment remains prevalent, despite four years of growth that looks to be strengthening. This was clear once again Wednesday, when headlines greeted April's slower inflation with another round of handwringing about the ECB needing to extend QE, rather than appreciating its Goldilocksiness. In our view, sentiment's badly lagging reality argues for eurozone outperformance continuing.

Exhibit 4: Eurozone PMIs at Six-year Highs

Source: FactSet and Markit, as of 6/1/2017. *Final May figure, not preliminary flash estimate.

Earnings are a primary stock driver and in the eurozone they're starting to accelerate, underscoring the Continent's healthy expansion and burgeoning economic strength. With such favorable earnings and economic tailwinds-paired with sentiment that doesn't seem to grasp this bullish backdrop-we think eurozone stocks likely have much further to rise.

[i] Economic and Monetary Union, aka the eurozone.

[ii] Source: FactSet, as of 5/30/2017.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10 -

Market Analysis Trim Your Angst on Economic Measurement Tweaks2026-07-09

-

Politics Long-Term Forecasts and Court Verdicts: The Latest in British and French Politics2026-07-09

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-07-08

2026-07-08

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today