Personal Wealth Management / Economics

Eurozone Flash PMIs and the Importance of Timing

How the holidays likely exacerbated eurozone flash purchasing managers’ indexes’ weakness.

IHS Markit released its flash December eurozone purchasing managers’ indexes (PMIs) today, and they weren’t exactly full of holiday cheer. The eurozone composite PMI slowed sharply, while Germany plateaued and France contracted for the first time since 2013. While this might seem like storm clouds are darkening on the heels of the eurozone’s Q3 GDP slowdown, this report has more caveats than your typical PMI does, making it a less useful gauge for investors trying to assess eurozone economic fundamentals.

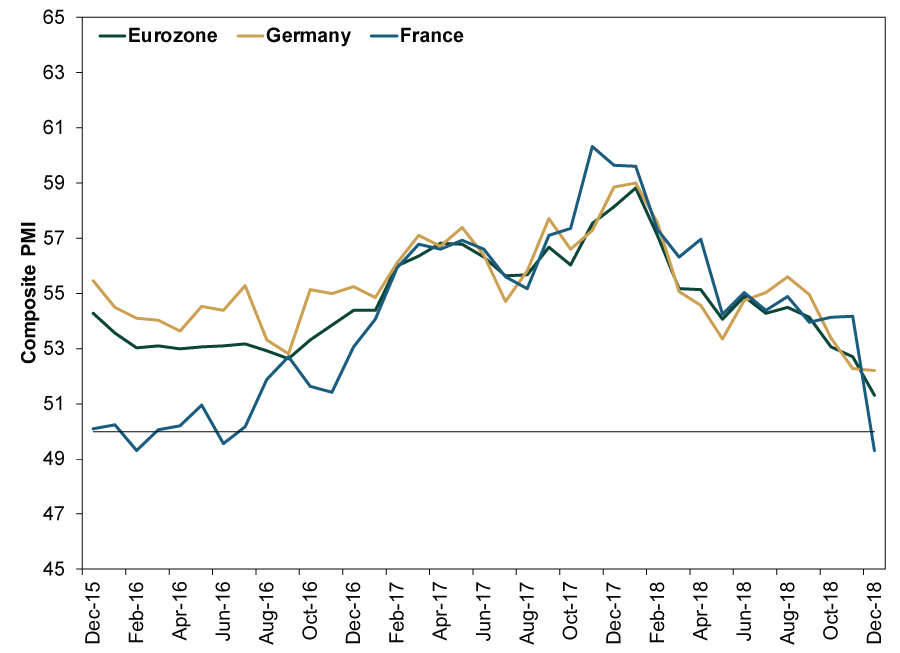

As Exhibit 1 shows, much of the eurozone’s apparent weakness probably stems from France. There is probably stuff going on in other countries as well, but only France and Germany have flash readings, so for now, France gets to shoulder the blame.

Exhibit 1: French, German and Eurozone Composite PMIs

Source: FactSet, as of 12/14/2018. Final composite PMIs, December 2015 – November 2018 and flash composite PMIs in December 2018. Readings over 50 indicate expansion.

The obvious explanation for this is the “Yellow Vest” protests, which the French central bank and others already warned would knock Q4 growth. With protests bringing much of the country to a halt since late November, it is fair to assume there will be some lost economic activity. Yet this PMI may magnify that impact. Typically, flash PMIs come out on the 25th of the month or thereabouts, making this month’s readings much earlier than usual. This isn’t weird or surprising for December, considering many businesses (particularly in Europe) close for an extended holiday break, apparently forcing IHS Markit to survey businesses earlier than usual. But this time, that meant surveying French purchasing managers between December 5 and 12, right in the heart of the protests. So PMIs give you all the downside, without any hint of how businesses fared in the protests’ aftermath. This is a widely known factor, so we are a bit perplexed that consensus expectations—which saw France’s PMI slowing slightly to 54.0 instead of sinking to 49.3—didn’t factor it in.

Protests weren’t the only culprit, of course. Both countries’ PMIs showed some lingering weakness in the auto sector, a well-known sore spot in Europe this autumn. New emissions tests took effect this year—a reaction to the emissions scandal from a couple years ago—and automakers have had some headaches phasing in the new system. That is a big reason German GDP contracted in Q3, and it also impacted output in other auto-making nations. But as firms get up to speed and work through the backlog of cars in need of testing, the GDP impact should fade. In other words, PMIs likely show a temporary hiccup still, um, hiccupping, rather than fundamentally weakening economies.

So take these reports with some grains of salt. Even the French PMI may not translate to contracting GDP, as PMIs are just one month and don’t measure growth’s magnitude. They loosely estimate the percentage of firms reporting increased activity, but not how much that activity rose (or fell). They are quick, blurry snapshots, not carefully focused portraits.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

See Our Investment Guides

The world of investing can seem like a giant maze. Fisher Investments has developed several informational and educational guides tackling a variety of investing topics.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | BRICS Summit, Fed Minutes, Trade Deal Deadline (Jul. 7, 2025)7/8/2025 12:00:00 AM

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 30 - July 47/7/2025 12:00:00 AM

-

Expert Commentary This Week in Review | One Big Beautiful Bill Act, US Jobs Data (July 4, 2025)

7/4/2025 12:00:00 AM

7/4/2025 12:00:00 AM -

Market Insights Ken Fisher on Tariffs and Volatility, Sequence of Return Risk, and More – July 20257/3/2025 12:00:00 AM

Learn More

Learn why 185,000 clients* trust us to manage their money and how we may be able to help you achieve your financial goals.

*As of 6/30/2025

New to Fisher? Call Us.

Contact Us Today