Personal Wealth Management / Market Analysis

Evaluating Valuations

An uptick in stock valuations doesn’t mean the bull market’s end is nigh.

Are stocks overvalued? Lately, it seems in vogue to suggest they are. Some claim valuations are too far above their long-term averages. Others say they look eerily similar to past peaks. In our view, all that chatter suffers a fatal flaw: assuming valuations somehow predict future returns. But they don’t! Valuations can be a useful sentiment indicator, but that’s it—no level is inherently bullish or bearish. Today’s valuations simply tell us what other, qualitative sentiment indicators would suggest: Investors are starting to become more optimistic.

Most recent valuation chatter centers on the price-to-earnings ratio (P/E), which compares a stock or index’s price level to trailing or estimated future earnings. Most interpret P/Es thusly: High valuations mean the market is overvalued and a big drop is nigh, while low valuations mean stocks are underpriced and it’s time to buy, buy, buy!

But in our view, P/Es don’t provide much value for forecasting future stock trends. For one, they’re backward looking. (And the sometimes-cited cyclically adjusted price-to-earnings ratio—which averages 10 years of E—is even more so, as discussed in depth here.) The numerator—current price—doesn’t predict future return. The denominator—earnings—doesn’t predict future profitability. Even if you’re using forward P/Es, it’s a rough estimate at best—and usually an estimate based on analysts’ assessment of past earnings and economic data. Many associate high P/Es with later-stage bull markets, when investors typically bid up stock prices—the numerator rises faster than the denominator. But high P/Es can also occur early in bull markets, when stock prices jump before earnings recover from recessionary levels. Stocks are forward-looking—they move before earnings, which tend to follow along with economic growth. 12-month trailing P/Es were off the charts in March 2009, when this bull market began—stocks bounced even though profits were depressed. Then valuations fell back through summer 2011 as earnings caught up—P/Es fell even though the bull continued.

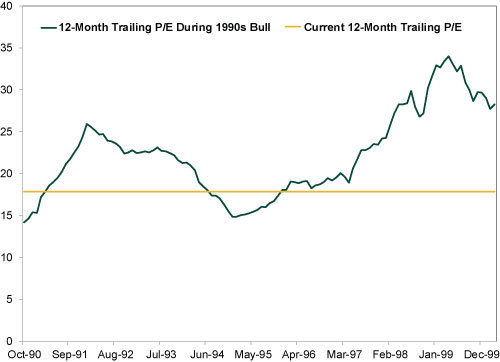

Valuations have ticked up since then, and the current S&P 500 12-month trailing P/E is indeed above its long-term average, as pundits point out. But this doesn’t mean much. It’s normal for P/Es to rise throughout a bull market—especially during the second half. That’s typically when sentiment starts becoming more optimistic and investors become willing to pay more for future earnings. Maturing bulls are also often when earnings growth is harder to come by as year-over-year comparisons become more difficult to beat and firms can’t cut costs for a quick boost. Then, earnings growth becomes a scarcer commodity, and investors compete more for a share in it, driving valuations higher—particularly high-quality mega-cap stocks. P/Es have spent significant chunks of many a bull above both current levels and the long-term average. In the 1990s bull, for example, the S&P 500’s 12-month trailing P/E exceeded today’s level for most of the bull’s second half—and hit 34 nearly a year before the bull ended. (Exhibit 1) That today’s valuations are nowhere near that—and only about 4.5 points higher than the 2011 low—merely tells us we haven’t seen that typical late-bull multiple expansion yet.

Exhibit 1: 12-Month Trailing S&P 500 P/E During the 1990s Bull

Source: Multpl.com, as of 1/22/2014.

But even that factoid doesn’t tell us much more than where sentiment is—pretty much the only thing P/Es are useful for. That we haven’t yet seen meaningful multiple expansion tells us investors haven’t started bidding up stocks in earnest—optimism is budding. Sentiment hasn’t yet become uniformly sunny, never mind euphoric. P/Es’ sentiment signal squares with other, more qualitative evidence of a tug-of-war between budding optimism and lingering skepticism. Rising equity mutual fund net inflows and the occasional high-flying IPO suggest sentiment is brightening, but many see those very things as signs of euphoria! That’s a very skeptical interpretation—not unlike the skeptical interpretation of today’s P/Es.

With investors just starting to become more optimistic, sentiment has a ways to improve before it hits a bull market’s typical euphoric heights. Which means valuations could very well rise much higher from here before the bull ends—just don’t expect valuations to tell you exactly when that end is.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Expert Commentary This Week in Review | Energy Markets, Fed Meeting, Earnings Reporting

2026-03-20

2026-03-20 -

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today