Personal Wealth Management / Market Analysis

Fire the Unemployment Rate

The unemployment rate is a terrible indicator of where the economy and stocks are headed.

People didn't do enough of this to meet analysts' expectations in September. Photo by Jill Ann Spaulding/Getty Images.

In what seemed to us like a blast from 2011 or 2012, Friday's US Employment Situation report disappointed, triggering an avalanche of dour headlines claiming this, "the closest proxy to the health of the economy," confirms worries slower growth (or worse) is at hand. This narrative dominated headlines dozens of times earlier in this bull market, but it has been largely absent since a string of more robust reports started in 2014. This time, stocks seemed to play along with the narrative, with the S&P 500 falling almost 1.5% after the open. But then stocks turned up, foiling plenty of headlines claiming "Wall St. Tumbles After Disappointing Jobs Data" and causing one news provider to delete the story "Dow Tumbles Over 200 Points After Weak Jobs Report" and replace it with "US Stocks Swing to Gains After Jobs-Report Slump, But Eye Weekly Losses," which was also deleted and replaced with "US Stocks Rally to End Week With Gains." But in perusing all these articles, what you won't see are reporters pointing out that whatever direction jobs headed in the prior month, it isn't relevant to where the economy or stocks are heading-jobs data are late-lagging, while stocks look forward.

Friday's report-widely panned as including nothing to like-showed US nonfarm payrolls grew by 142,000 in September, well below the consensus analyst forecast of 206,000. It's also well below the 198,000 average monthly pace this year to date. In addition, July and August were revised down by a total of 59,000 jobs. The two months now show 223,000 and 136,000 hires, respectively. The headline unemployment rate remained unchanged at 5.1%, which many harrumphed at, considering it seems tied to the labor force participation rate's falling from 62.6% to 62.4%.[i]

This alleged thud of a report comes during a correction many attribute to China and global economic weakness. A common media theme among some bullish pundits in the days leading up to Friday held the alleged global weakness wouldn't matter to America-after all, consumers make up 70%-ish of the US economy and jobs were surging. Healthy labor markets, they argued, would create an economic moat around the US and propel the economy higher regardless of what happened abroad. Friday's jobs dud seems to give proponents of this theory pause.

And pause they should! The theory "jobs will save us!" falls into what we call "The Employment Sentiment Trap." The Employment Sentiment Trap is basing a bullish or bearish outlook on jobs data. Many wrongly believe this is a key indicator of where the economy will go. But it isn't. It shows where the economy has already been. Jobs are a late-lagging economic indicator with basically no forward-looking implications. Stocks are forward-looking indicators that aren't serially correlated or influenced by the past. Absent a time machine, you can't use late-lagging indicators to forecast forward-looking ones.[ii]

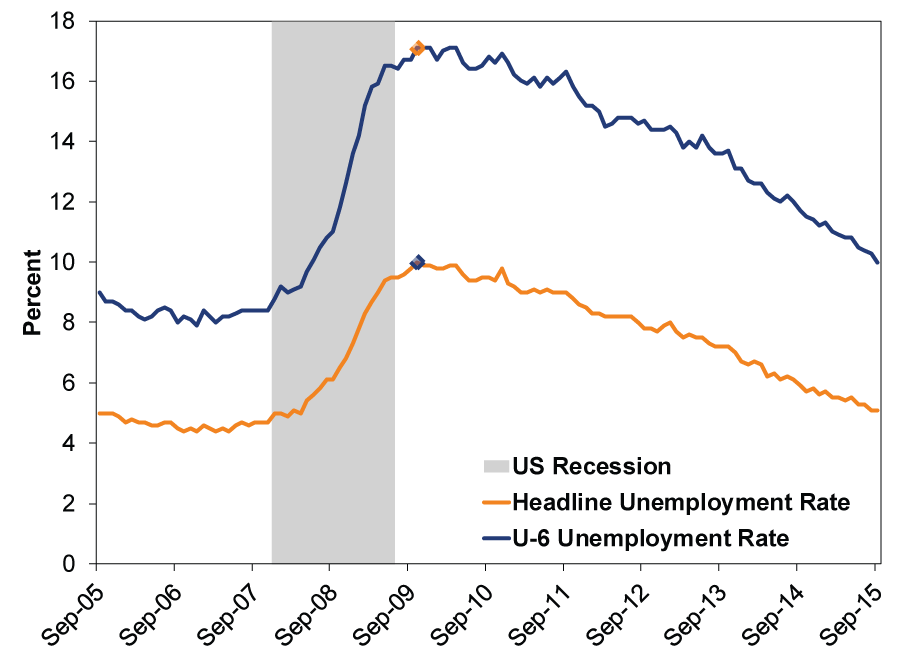

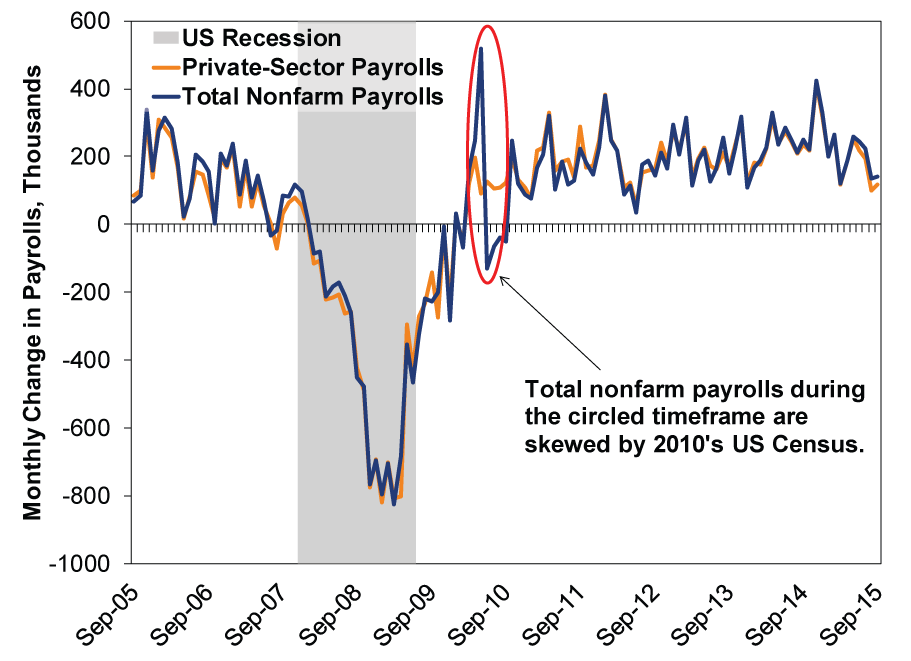

Consider: In 2009, stocks began rallying in March and the recession ended in June. But the headline unemployment rate rose until October. And even this is misleading! The headline unemployment rate excludes workers who are discouraged by economic conditions and aren't actively seeking work. In Exhibit 1, the U-6 unemployment rate-which includes discouraged workers and those working part-time for economic reasons-shows the decline post-October 2009 was initially due to more unemployed workers getting discouraged.[iii] Employers were trimming payrolls into 2010. (Exhibit 2)

Exhibit 1: US Unemployment Rate and U-6 Unemployment Rate

Source: Federal Reserve Bank of St. Louis, as of 10/2/2015. September 2005 - September 2015.

Exhibit 2: US Total Nonfarm Payrolls and Private-Sector Payrolls

Source: Federal Reserve Bank of St. Louis, as of 10/2/2015. September 2005 - September 2015. Census period circled to show skew caused by the government hiring many temporary census-takers.

But just as high unemployment didn't prevent a boom, low unemployment won't prevent a bust. Consider 2000. In April 2000, unemployment reached 3.8%-a very low rate by historical standards. By the time unemployment was a measly 1 percentage point above this cyclical low (August 2001), the S&P 500 was down more than 25% from its peak. Similarly, October 2007's 4.7% unemployment rate didn't shield the economy or stocks from the Global Financial Crisis.

Maybe this all seems counterintuitive and that's why it persists. After all, jobs are a necessity for most Americans, and the biggest contributor to US GDP is consumer spending. But when you think about it from an employer's perspective, it isn't counterintuitive at all. Hiring and training new workers is costly, time consuming and can negatively impact a business's productivity and profitability. Many employers will stretch and make do with current staff as long as they can before hiring. Similarly, many employers will be very reticent to cut workers, knowing the training and experience they have attained will likely have to be replaced someday. This isn't a decision most employers make lightly.

But even so, another reason the dour media take seems over done is hiring was positive in September, it just missed estimates and slowed down a bit. And these data are frequently revised. Sometimes downward, like July and August 2015. But also, sometimes upward. In August 2011, the initial report showed nonfarm payrolls were unchanged. As in no jobs added. Zero. Headlines far and wide proclaimed it a harbinger of looming recession.[iv] But in the second estimate, the Bureau of Labor Statistics found employers actually added 57,000 jobs. And in the third, this was bumped up again-to 104,000. That may not be robust, but it isn't zero either.

We perfectly understand that nerves are running a little high presently, so a report showing a slowdown in jobs growth might rattle some folks. But given how much lag there is in jobs data, September's flop could easily be a result of Q1 2015's temporary, weather-and-West-Coast-ports-labor-dispute-induced slowdown to 0.6% annualized GDP growth. The US snapped back to 3.9% growth in Q2. Monthly indicators published to date point to growth continuing in Q3. And most importantly, The Conference Board's US Leading Economic Index (LEI)-a reliable forward-looking indicator-is high and rising. In the last 50 years, no US recession has begun when the LEI is in an uptrend. If it is the future you care about, these data will help much more than jobs.

[i] The Labor Force Participation Rate is the percentage of Americans above the age of 16 who are not in the military or in prison (or other institution) who are either employed or are unemployed but actively seeking work. Many who decry the present rate as low suggest there are huge numbers of discouraged workers dropping out of the labor force, driving unemployment down for depressing reasons. But in September, it is worth noting only 120,000 of the 579,000 workers who left the labor force did so for economic reasons. And, adding in those who are discouraged or aren't actively seeking work would boost unemployment from 5.1% to just 6.2% (here is a chart of this, which the Bureau of Labor Statistics calls the U-5 rate. These workers are included in the U6 rate depicted in Exhibit 1).

[ii] And then you don't need any indicators. You have a time machine!

[iii] For a discussion of this phenomenon in September 2015, see (lengthy) footnote 1.

[iv] See the preceding 497 words and two charts for why this interpretation is and was wrong.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 11 - May 152026-05-18

-

Behavioral Finance Investing Lessons From the Indianapolis Motor Speedway2026-05-18

-

Expert Commentary 3 Things You Need to Know This Week | Global Inflation, Fed Minutes, US Sentiment2026-05-18

-

In The News Around the World in Tax Policy Talk2026-05-15

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today