Personal Wealth Management / Market Analysis

Fisher Investments on Rising Commodity Capital Expenditures

Rising demand from Emerging Markets consumers has had downstream effects on agricultural commodities. This bodes well for commodity capital expenditures.

Emerging Markets income growth has fueled demand for agricultural commodities, and production is struggling to keep up. The resulting shortages have led to surging prices, and production—already well above its ten-year average—is expected to reach record highs next year as farmers take advantage. Fisher Investments believes record farm receipts will likely follow, along with increased capital expenditures on farm equipment, boosting manufacturers.

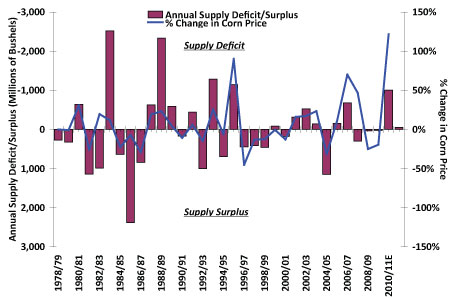

Though all grains face production shortfalls and rising prices, corn is especially tied to Emerging Markets demand growth. As developing world’s burgeoning middle class consumes more and more meat, more livestock eats more corn—much of which is supplied by the US. Current USDA estimates for the 2010/2011 harvest (roughly 65% of the US’s agricultural output) point to a more than 1 billion bushel production deficit, causing prices to more than double over the last year. The USDA also forecasts a roughly 55 million bushel deficit for 2011/2012, which should keep prices firm.

Figure 1: US Corn Surplus/Deficit’s Impact on Price

Source: USDA, Thomson Reuters, Fisher Investments Research.

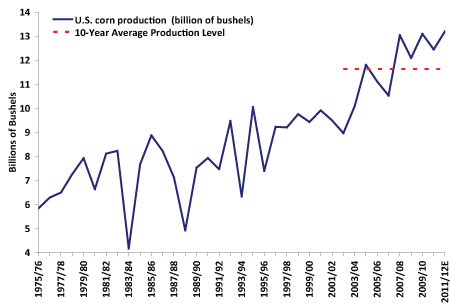

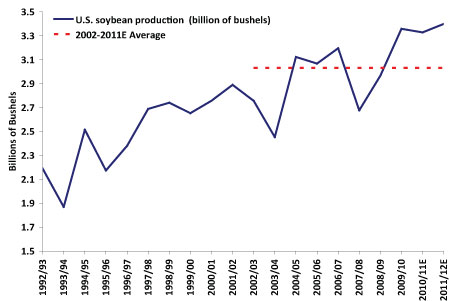

As farmers seek to capitalize on higher prices, the USDA estimates both US corn and soy production will achieve all-time highs.

Figure 2: US Corn Production

Source: USDA, Fisher Investments Research.

Figure 3: US Soybean Production

Source: USDA, Fisher Investments Research.

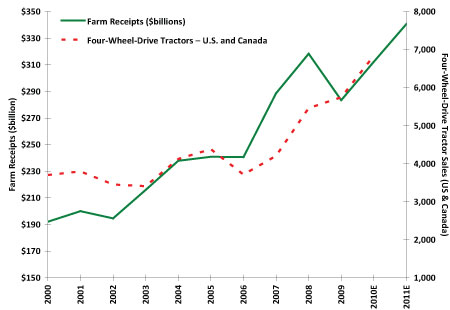

Elevated production, multiplied by record commodity prices, should bring record-high US farm receipts in 2011, according to USDA estimates. Farm receipts and purchases of agricultural equipment like four-wheel-drive tractors tend to move together, which suggests robust capital expenditures on agricultural equipment are likely in 2011.

Figure 4: US Farm Receipts and Tractor Sales

Source: USDA, Association of Equipment Manufacturers, Fisher Investments Research.

Of course, some headwinds remain. Weather can significantly impact production estimates, depending on farm economists' opinions on the damage to yields. If estimates overstate bad weather's impact, crop prices will likely decline (assuming production significantly exceeds expectations). On the demand side, Congress is debating the future of ethanol production credits. Since roughly 35%-40% of US corn production goes toward ethanol, eliminating credits could dampen demand and prices. Yet even if credits are eliminated, substantial ethanol production mandates remain in place, and removing credits would likely cause production to revert to mandated levels.

Still, rising Emerging Markets appetites seems to be the most important factor for crop prices, and Fisher Investments believes this trend won't likely abate any time soon. GDP growth in many developing nations remains robust, and as this continues, demand for corn, rice, wheat and soy should keep growing nicely.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 9 - March 132026-03-16

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today