Personal Wealth Management / Market Analysis

Fisher Investments Research: Why You Should Be Thankful China’s Currency Isn’t Rising

Many decry China’s yuan as artificially undervalued—but China’s currency rising radically would pose far more problems than it would solve.

China’s currency has barely budged this year, and Fisher Investments thinks you should be ecstatic about it. While the yuan’s lack of appreciation tends to get everyone from presidential candidates to the US Treasury Department up in arms, the truth is the world (including the US) would be a lot worse off if China started letting its currency rise radically at this point.

To understand why, we need a quick refresher in macroeconomics. There is a basic concept in economics that free capital flows, a fixed exchange rate and control over monetary policy (i.e., money supply and inflation) are incompatible. It’s sometimes called the “impossible trinity”—you can have two of three but never all three at the same time.

To see why, consider your investment options if you could freely move money into China and invest there. (You can’t, by the way, they have strict controls.) You could borrow money at cheap rates in the US and invest in bonds with higher interest rates in China—known as a carry trade. However, with a fixed exchange rate, unlike most carry trades, you’d have no currency risk. In fact, other than the risk of China’s government defaulting (unlikely at this point), you’d have no risk at all and therefore have endless incentive to continue this until the cows came home. The ultimate free lunch! Everyone would do it. However, as investors poured funds into China, their government would be forced to print unending amounts of currency to offset the upward pressure on the currency and maintain the peg. Inflation would run wild. You can’t control all three at the same time. (For more details on China’s economic structure see Fisher Investments'previous column).

China knows this and therefore has strict restrictions on funds going in and coming out. However, through trade and other (some illicit) means, capital does flow, at least partially. Therefore, China only partially controls its money supply and inflation.

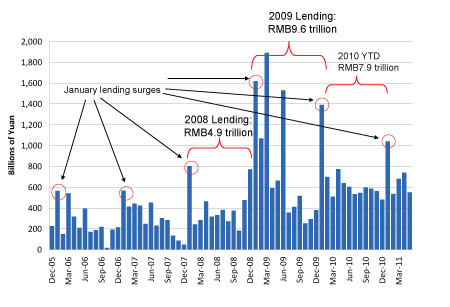

This is why China’s attempts to stop inflation by increasing reserve requirements or interest rates have never been successful. These tools help, but don’t tend to stop inflation’s upward march. Therefore, China has been forced to turn to the cruder tools of controlled currency appreciation and loan quotas. Each year, the government sets an annual loan quota banks are allowed to lend. While less than ideal from an efficient capital allocation standpoint (and one of the reasons China’s banking system has to be bailed out after every period of economic stress—1998 & 1999, 2003, 2010 and rumors of 2011), it does help control the money supply (bank lending is a natural money multiplier). The effects of this policy can be seen in Exhibit 1—lending surges every January to satisfy loan demand constrained at the end of the previous year.

Exhibit 1: China’s New Loans

Source: Bloomberg Finance L.P.

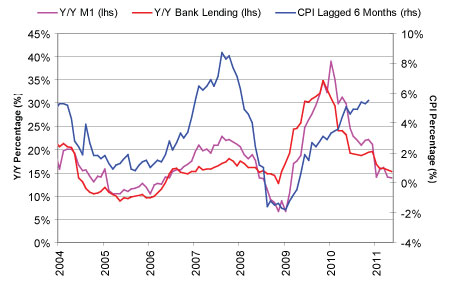

Because loan and currency levels are more powerful tools for controlling money supply, one can see their effects quite easily. Consider Exhibit 2 and the close relationship among the growth in bank lending, money supply, and with about a six month delay—inflation.

Exhibit 2: China Money Supply vs. Loan Growth

Source: Thomson Reuters.

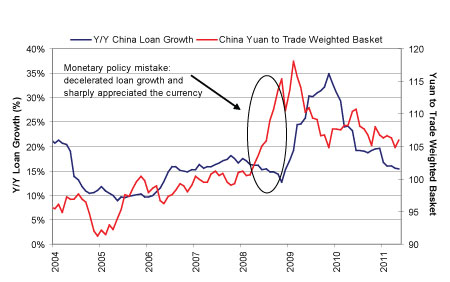

Because China doesn’t have a significant bond market and nearly three-quarters of funding for all enterprises (consumers, corporations and local governments) comes through the banking system, loan growth not only drives inflation, but also is a major tailwind to economic growth. Therefore, to maintain long periods of rising loan growth and economic acceleration without sending inflation skyward (as demonstrated in Exhibit 3), China typically lets its currency rise along with loan growth. Loan growth is generally the more powerful force, but letting the currency rise helps slow inflation.

Exhibit 3: China Loan Growth and Trade Weighted Currency

Source: Thomson Reuters.

Of course, ultimately, China can’t afford extremely high inflation (or a recession) due to its authoritarian form of government. Without the right to express displeasure through voting, social unrest and revolt are historically the means of communication for such a population if its standard of living becomes adequately eroded. Therefore, China has to eventually decelerate loan growth—and when it does, it should stop its currency appreciation or risk hitting its economy with two hammers at once, possibly causing a hard landing. It made this monetary policy mistake in the first half of 2008, which led to a significant slowdown and contributed to the commodity markets’ crash, which began in June—months before the Lehman Brothers-induced financial debacle. Should it make this mistake again and cause the world’s second largest economy to slow dramatically, Fisher Investments believes the world would be worse off.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

-

Market Analysis Pumping Up the Yen?2026-07-17

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today