Personal Wealth Management /

GDP Goes Up in Smoke?

US Q1 GDP just got revised down, but EU GDP is about to get, um, higher.

Dr. H.A. Thomas demonstrates the workings of an electronic calculator. We suspect GDP inputs take a similar path. Photo by Jimmy Sime/Central Press/Getty Images.

“The US Economy Had a Hiccup, Not a Heart Attack, This Year” “US Economy Stumbles in First-Quarter, but Prospects Brighter” “Why the GDP Drop Is Good for the US Economic Outlook” That was the primary media reaction to Q1 US GDP, which recorded what seems like a contraction after the Commerce Department’s first revision. All of which seem like fairly rational reactions, in our view—nothing in this GDP report signals bad news to come for the economy or stocks.

Yes, it now appears GDP fell at a -1% annualized rate in Q1. Yes, by some arbitrary overly technical definitions, it’s “one quarter away from recession.” Then again, one could have said the same thing about Q1 2011’s 1.3% drop, or the initially reported 0.1% fall in Q4 2012 before it was revised away. One-off drops during expansions aren’t unprecedented.

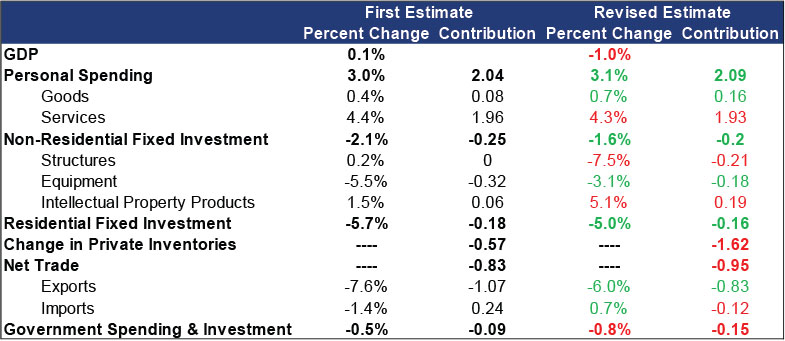

Nor are they inherently bad news. If output were down big across the board, there would be cause for concern. But that wasn’t the case in Q1, as shown in Exhibit 1. Consumer spending was revised up, driven by sales of physical goods (a counterpoint to those who claimed big spending on utilities during the harsh winter was our only saving grace). Business investment was revised up, led by a big gain in spending on intellectual property (including software and R&D). Exports got only a bit less lousy, but imports did a full 180—the revision reversed a fall to a rise, a strong showing of domestic demand. But in GDP’s wonky math, domestic demand for imports detracts from growth. Net trade (exports less imports) subtracted nearly 1% from growth in Q1. The biggest single detractor was the change in private inventories, a logical side effect of the weather. It largely goes without saying that if demand is strong, but factories are shut by blizzards and power outages and snowdrifts are blocking highways and train tracks, businesses will have to deplete stock piles to satisfy customers.

Exhibit 1: Initial and Revised Estimates of GDP and Its Components

Source: Bureau of Economic Analysis, as of 5/29/2014.

In short, while the headline growth rate suggests Q1 was a dud, the components say otherwise. If you’re a long-term growth investor, you can file this under “interesting observations”—stocks have long since moved on. They’re looking at where the world is going over the next 12-18 months, not at how one imperfect measure of US output did between two and five months ago. What’s ahead is what matters, and with the Leading Economic Index (LEI) still high and rising—up another 0.4% in April—it would be unheard of for the US to lapse into recession now. No recession in LEI’s 55-year published history has started while LEI is on an upswing. That tells you most everything you need to know about where the economy is headed in the near term (but if you need more, there are rising retail sales, strong services and manufacturing gauges, another rise in durable goods and resurging real estate).

In our view, the Q1 GDP report is most telling about ... GDP! GDP’s quirks and shortcomings, that is. Yes, it has its uses—it’s about the most all-encompassing economic indicator we have. But it’s not perfect. Q1 shows it can fall even if businesses and consumers show plenty of life. Recent recessions have featured big drops in imports, boosting the headline growth rate since GDP subtracts imports. But falling imports means falling demand. Call us crazy, but any reading of the economy that would count a drop in demand as a positive is at least a touch wackadoodle.

There is also some activity GDP just doesn’t capture, like the millions of artisans and crafters selling their wares on websites like Etsy or providing services through UberX, Airbnb and the like. These people work, produce, engage in commerce and pay their taxes, but it’s a virtual certainty they aren’t all registering as small businesses and filing sales totals with the Small Business Administration. Their economic contributions aren’t small. But they aren’t in GDP.

The folks who maintain National Accounts get this—they know GDP isn’t perfect. The series is regularly refined and revised over time as the economy evolves, we get better data and the world’s thinking changes. Last year, GDP was revised back decades to account for intellectual property and R&D. EU officials, bless ‘em, handed every member state marching orders to round up as much sales data as they could for drug dealing, smuggling and even, um, the world’s oldest services industry. Preliminary UK data show these and other illegal activities would have added about £10 billion to GDP in 2009—more than twice total construction output! Italy estimates its criminal sector will boost output at least 1.3% a year. Greece could be 2% bigger.

The obvious questions this raises cut to the heart of GDP’s shortcomings. One, in addition to counting imports backward, European GDP will now count shortcomings in governance and law enforcement as a positive. The days of “Crime Doesn’t Pay” as a slogan, apparently, are over. Now, some could argue that while money spent on drugs, smuggled wares and ladies of the night is money spent illegally, there is a multiplier effect—maybe the criminals go buy iPads, and the money makes its way to the legitimate economy. Fair enough, but those legal spends are already in GDP. Inflating the total with criminal behavior isn’t necessary. Two, we have our doubts about the quality of the data. The UK’s Office for National Statistics admitted it isn’t exactly collecting little black books and receipts from drug runners. They used assumptions and estimates extrapolated from Dutch data, police records and “a variety of sources” and advised users to take it all with a big grain of salt. You don’t say.

But it’s a sociological debate, not an economic one. Stocks look past GDP’s weirdness. Stocks aren’t even GDP! They’re a slice of ownership in publicly traded companies. Part of GDP, not all of it. So while we wouldn’t suggest folks ignore GDP—we certainly don’t—we’d just encourage investors to bear this in mind: GDP isn’t the be all, end all indicator of an economy’s robustness. It’s just one stat. One backward-looking, imperfect stat.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis New Tax Year, More British Business Tax Fear2026-04-08

-

Market Analysis Quick Hit: What to Make of Jobs Data’s Persistent Swings2026-04-07

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

-

Expert Commentary US Inflation, Fed Minutes, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-06

2026-04-06

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today