Personal Wealth Management / Market Analysis

Getting Sentimental About Negative Rates

Negative bond yields show investors remain fearful, a sign the bull market is far from over.

Should you approach negative yields with caution? Photo by Alan Schein/Getty Images

If you were a bank, would you pay borrowers for the privilege of extending them credit? Well, lots of investors are doing just that these days. Global sovereign bond yields are at historic lows, with some-even long maturities-dipping into negative territory. Bond buyers are literally paying some governments to borrow from them. This is in stark contrast to the double-digit interest rate world of the 1970s many retirees and investors remember well, and it's understandable some see today's ultra-low yields as an omen of something big, bad and ugly about to happen to stocks.[i] But in our view, yields at generational lows don't mean the world has fundamentally changed. Actually, the widespread pessimism seems like another brick in the proverbial wall of worry stocks love to climb-a sign the bull market likely has further to run.

Last Tuesday, German 10-year bond yields fell below zero for the first time on record. French yields on seven-year debt are -0.07%, slightly higher than Swedish seven-years' -0.16%.[ii] Danish bond yields are in the red through five years. Japanese yields are below zero through 15-year maturities, and Swiss government bond yields win the "prize": 10-year Swiss debt first went negative in January 2015 and yields are now negative all the way through 30-year maturities.

The common narrative on this, and it is partly true, is that negative rates are due to central bank policies. For one, quantitative easing bond buying programs in the eurozone and Japan reduce the supply available to private investors, adding upward pressure to prices, driving yields even lower. On top of that, negative deposit rates in the eurozone and Japan are partly to blame, as some depositors are buying bonds to escape the "tax" of paying central banks to park funds with them. When rates on shorter maturities of sovereign debt went negative, investors seeking high-quality, liquid debt moved into longer bonds-pushing those rates down, too.

But fundamental drivers don't tell the whole story-sour sentiment is also a factor. Lately, investors have been entranced by the uncertainty stemming from things like UK's looming vote to possibly exit the EU and the US election. This fear has caused a classic flight to safety, and many currently see sovereign debt as a safer place to invest than stocks, despite the negative rate. Buying bonds at no or slightly negative yields is a sign many investors are more concerned with the return of their money than the return on it.

Even if the rate isn't outright negative itself, buying bonds at yields below inflation rates achieves a negative real rate of return in exchange for perceived safety. For example, the US 10-year is yielding 1.58% presently, but the US consumer price index excluding food and energy showed prices rose 2.2% y/y in May. Investors willingly giving up purchasing power is a sign fear is running rather high.

For investors today, seeing rates where they presently are may be somewhat off-putting. In the US, rates were last in this territory in 2011 and 2012, but before that, you're talking about rates unseen since the 1940s and early 1950s. Negative yields at long maturities are relatively new. Investors' lack of familiarity with such low rates is likely one reason they believe it means they spell trouble. But ultra-low or negative yields doesn't mean we're living in a new world. There still is no set relationship between rates and market returns. It is still the gap between sentiment and reality that matters. And, on the sentiment front, recent action is telling. For one, the financial media is likely contributing to the fears over negative rates, reporting each further downtick as front page news and couching it as something to worry about.

But also, consider investors' mindsets: You'd have to be pretty darn dour to pay Japan or Germany to lend them money for 10 years. Ditto in the UK or US, where buying a bond means accepting a super-low-occasionally sub-inflation-rate of return! Heck, how pessimistic do you have to be to pay the Swiss government for the fun of lending them money for 30 years? Now, to be sure, some investors are obligated to buy bonds for regulatory reasons. But not all of them, and even they usually have some leeway about the investment they choose.

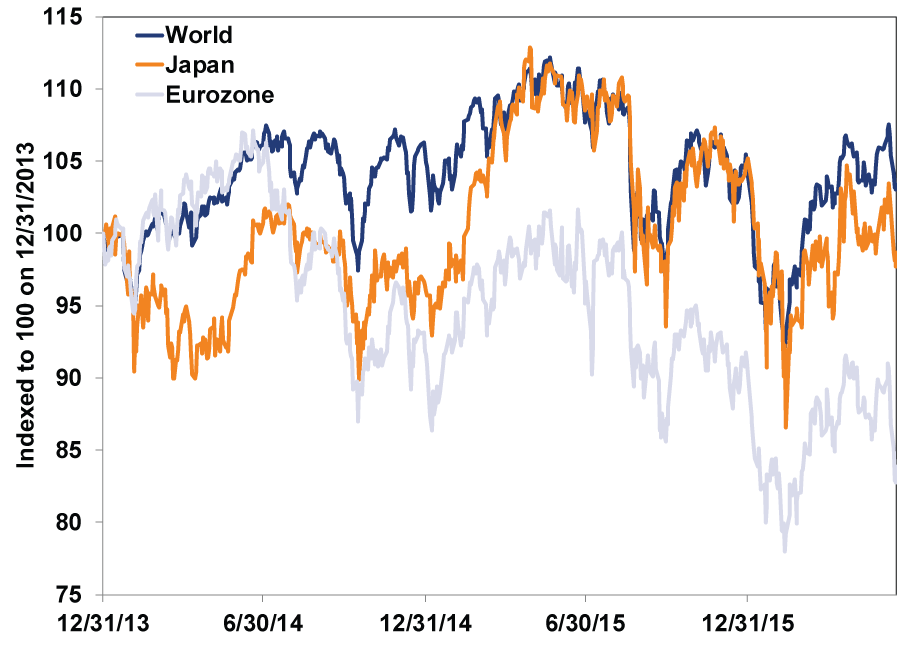

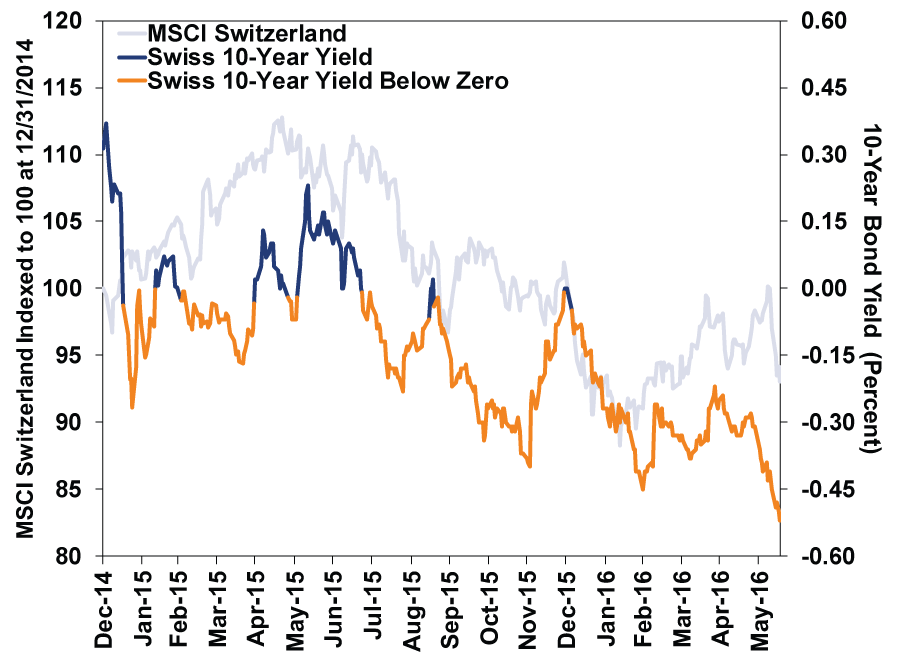

Fortunately for investors, negative bond yields aren't a warning sign for stocks, because bond markets don't know anything stock markets don't. All liquid markets discount all widely known information near immediately. So whatever German, Swiss and Japanese bond investors fear, investors in other markets fear too, and those fears are baked into stock prices. It may not seem that way, especially for US investors, as US stocks have held up pretty well lately relative to foreign equities. But stocks in regions where yields have gone negative, particularly in the eurozone, are weaker. (Exhibit 1) This is strong evidence both bond and stock investors are equally anxious. But the fundamental impact of negative yields isn't likely behind them. As Exhibit 2 shows, there is no set relationship between yields and stocks-Swiss stocks had good times and bad alongside sub-zero yields in the nation that has had them longest.

Exhibit 1: Stocks Where Yields Are Ultra-Low Are Weak Too

Source: FactSet, as of 6/17/2016. MSCI World, MSCI Japan and MSCI European Economic and Monetary Union Index returns with net dividends, 12/31/2013 - 6/16/2016.

Exhibit 2: A Closer Look at Swiss Yields and Stocks

Source: FactSet, as of 6/17/2016. Swiss 10-year bond yield and MSCI Switzerland Index with net dividends, 12/31/2014 - 6/16/2016.

Yields in some parts of the world may be setting new lows, but on its own this has little bearing on where stocks are headed. It doesn't even have any bearing on where yields themselves are headed! It is past, and in markets, past never predicts.

What these rates are doing is adding to the extant uncertainty around other events like Brexit and the US election. These are weighing on sentiment in the near term, and likely contributing to recent volatility-in both bond and stock markets. However, much of this uncertainty is set to bullishly fall. The Brexit vote is this week. The US election is in November, and uncertainty should gradually fall up to then, as investors price in campaign pledges and opinions. Negative yields, unlike those two, have no expiration date. But folks will adapt to them given time, and as they do, expect uncertainty to fall, which is bullish.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03 -

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Analysis Reader Mailbag: June 20262026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today