Personal Wealth Management /

Growth Abounds All Around

Economic growth is all around us, which seems likely to continue, too.

Q2 GDP is trickling in from around the world, and the early results shatter the notion of a weakening world. Forward-looking data show growth likely continues-and continues supporting the bull.

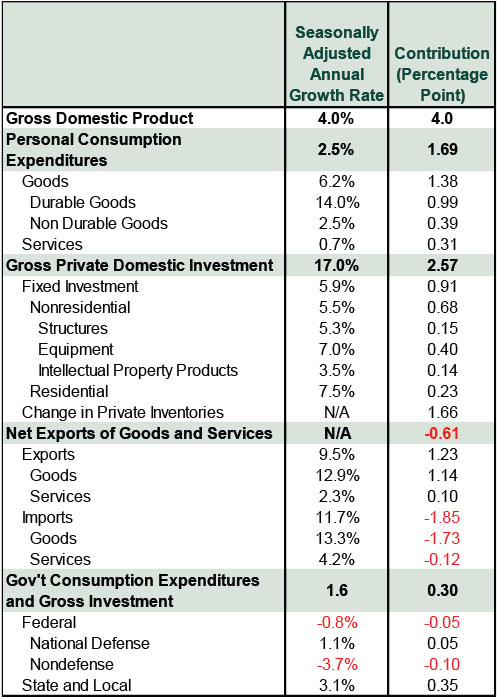

US Q2 2014 GDP grew at a 4.0% seasonally adjusted annual rate, rebounding from Q1's (revised) -2.1% weather-driven drop. Growth was broad-based-as Exhibit 1 at the bottom of this page shows, every major category except net exports contributed positively, and even that dip isn't bad news (more on that momentarily). Most welcomed goosy growth, but a loud minority pointed to the 1.66 percentage points inventories added to growth and claimed the feat is unlikely to repeat-growth isn't sustainable. Perhaps inventories' rise doesn't continue. It likely was partly a reversal of Q1's weather-related slide. If factory power outages and iced-over shipping routes force firms to strip shelves to meet demand in one quarter, they'll probably restock the next. That isn't weakness-just logic. If this were the only factor driving growth, we'd be iffy. But even if you subtract inventories, growth was fine.

To see this, consider Q2 trade. Yep, we know, net exports detracted 0.61 percentage point. But that skewed measure treats rising imports, a sign of healthy demand, as a negative. In the quarter, imports rose a whopping 11.7%, shaving 1.85 percentage points off headline growth. Demand! Export growth wasn't too shabby, either, at 9.5%. This may be revised-trade data are incomplete in the first read. But consumption may be revised, too-health care spending was noted as adding only 0.08 percentage point in Q2-small, considering Q1 showed Affordable Care Act policy subscriptions and associated medical treatment were likely pushed back by technical difficulties (and this wasn't apparent until the third reading).

Spain logged its fourth straight quarter of growth, with Q2 GDP up 2.4% annualized (0.6% q/q)-topping estimates and accelerating from Q1. Headlines were skeptical, with some lumping this news in with deflation fears-pointing to July's -0.3% m/m consumer price index drop. Some fear Spain's growth will make more radical ECB action seem unnecessary, preventing measures (like quantitative easing, QE) pundits seemingly believe are necessary to "combat" deflation. But the eurozone overall actually isn't in deflation. They're in disinflation-prices are still rising, just more slowly. Spain logged one deflationary month in July, but it's one data point. Plus, deflation has little history of being a leading economic indicator. These fears also presume more radical ECB action would help, when less radical regulatory action (stress tests) seem more beneficial-particularly compared with QE, itself deflationary in our view.

Across the Channel, UK Q2 2014 GDP, released last Friday, grew 3.2% annualized (0.8% q/q). This early read includes only output components (spending data come in the second estimate), but it's in line with the recent trend-GDP rose 3.2% annualized (0.8% q/q) in Q1 and 2.8% in Q4 2013 (0.7% q/q). Production and services grew 0.4% and 1.0%, respectively-contributing 0.1 and 0.8 percentage point to growth. Smaller sectors fell-agriculture and construction fell -0.2% and -0.5%, respectively. But the bigger components drove growth, and services-the biggest sector of the British economy-led in Q2. This pushed GDP above the pre-recession peak. Some groused about still-lagging per-capita GDP, calling the return to expansion a population-growth mirage, but that's irrelevant for stocks. Markets just need a growing economy to support corporate earnings, and the UK easily has that.

Emerging Markets also climbed. Chinese GDP rose 7.5% y/y-matching its growth target and beating Q1's 7.4%. Still no hard landing in sight. Some point to slowing housing as a canary in a coal mine, but we'd caution against hasty conclusions. Perhaps the property market does fall more-a supply glut, iffy credit access and housing restrictions will do that. But cities are easing up and loan growth is solid. Moreover, China's overall economy is strong-housing isn't likely to cause big problems. Case in point, the industry fell in Q2, yet China grew. Even if bad loans did flood banks-which there are few signs of-China has trillions in foreign currency reserves it could use to recapitalize state-owned banks to avert a crisis. It has done so before.

In South Korea, Q2 2014 GDP rose +0.6% q/q (2.4% annualized), slower than last quarter's 0.9% q/q. The first drop in private consumption since Q1 2013 drove the slowdown-possibly a side effect of the Sewol ferry disaster. Either way, the government is already pushing measures to boost future growth, which may or may not succeed, but the discussion is at least timely.

Growing GDP is nice, though backward-looking. However, forward-looking data like The Conference Board's Leading Economic Indexes (LEI) suggest the future is bright. US LEI rose in five of six months (January is the exception). Chinese and UK LEIs have run the table, growing the entire year to date. Spain's LEI rose in four of the last five months, including the most recent (May). Korea's LEI is the weakest, rising in three of the last five months and falling in May-not wonderful, but the preceding three months rose and isolated LEI dips don't tell you much. One month does not a trend make.

LEI and GDP alone can't forecast stocks. But strong GDP dispels fears the world was weakening, and LEI show it isn't likely to start weakening any time soon. Stocks likely don't face a headwind from a slower globe ahead.

Exhibit 1: Q2 2014 GDP Breakdown

Source: Bureau of Economic Analysis, as of 07/30/2014. Component-level Q2 2014 GDP contributions and growth rate.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary US Inflation, Fed Minutes, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-06

2026-04-06 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

-

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03 -

Market Analysis A Forward-Looking Lesson One Year After Liberation Day2026-04-02

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today