Personal Wealth Management / Market Analysis

Deflating Chinese Housing Bubble Fears

Chinese housing bubble fears have seemingly surfaced again. However, such fears fail to recognize the unique characteristics of the Chinese property market, make too-direct comparisons to US housing and underestimate the Communist government’s resolve to prevent a housing market bubble from bursting.

Chinese housing bubble fears have seemingly surfaced again, as they occasionally have the past few years. (For example, we addressed this topic in early 2011.) In our view, such fears fail to recognize the unique characteristics of the Chinese property market, make too-direct comparisons to US housing and underestimate the Communist government’s resolve to prevent a housing market bubble from bursting. As a result, we expect recent fears to subside without incident, as they have in the past.

By international standards, China's housing market does seem relatively overvalued. However, many Chinese citizens use homes (often second, third and fourth) as a sort of savings account. Strict capital controls, a lack of significant property taxes (until recently), negative real interest rates (inflation is higher than bank deposit rates) and limited alternatives make housing an attractive investing option. This is despite Chinese law, which requires a 30% down payment on first homes, 60% on second homes and no mortgages on third homes in many provinces.

But a big drop in Chinese housing values likely doesn’t have the huge knock-on effects many investors fear. Even though real estate’s been a popular investing option, the mortgage market is estimated to make up roughly 15% of total bank loans in China. With such high down payment levels and limited mortgage markets, Chinese banks estimate they have capital to adequately handle at least a 40% decline in home prices. What’s more, should capital levels prove insufficient, the government would likely recapitalize the state-owned banks (the bulk of the Chinese financial system) with some of its roughly $3 trillion in foreign currency reserves, as it has done in other periods of stress (in 1998 and 1999 following the Asian Contagion, 2003 following the Tech Bubble, and 2010 following the global financial crisis).

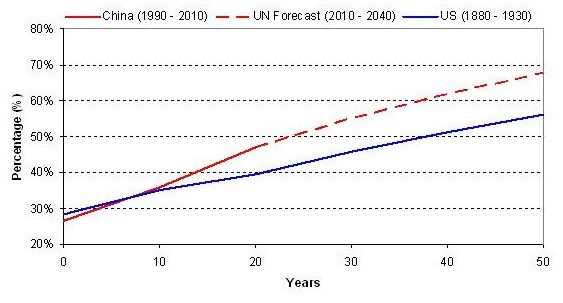

Of course, the most attention-grabbing examples of misallocated capital in Chinese real estate are ghost towns, empty housing units and vacant malls. But some perspective is in order to help frame the size and scope of China’s infrastructure, housing and urbanization initiatives. According to UN estimates, China will have urbanized roughly 260 million people from 2000 to 2015—arguably the world’s largest human migration accomplished in a relative blink of an eye. Exhibit 1 shows China’s urbanization rate compared to the US’s rate from 1880 to 1930.

Exhibit 1: Relative Urbanization Rates—US (Historical) v. China

Source: United Nations and US Census Bureau.

Government spending is often inefficient and invariably, centrally planned spending on this scale brings ample capital misallocation—inefficient construction and/or periods where it takes time for migration to fill new construction. Yet, over time, some previously reported vacant cities, buildings and shopping centers have filled. Those that may never fill are likely offset by productivity gains brought by improved infrastructure and industrialization. Since the government owns roughly two-thirds (estimated) of the country’s assets, it can afford some unsold, empty buildings. To the Communist party, government-owned vacant property is also a means to meeting their massive push to increase low-end housing supply. Targeting lower prices and increased urbanization rates, the government is planning to build 36 million low-end housing units from 2011-2015—a move to reduce social tension and stymie the possibility of uprising.

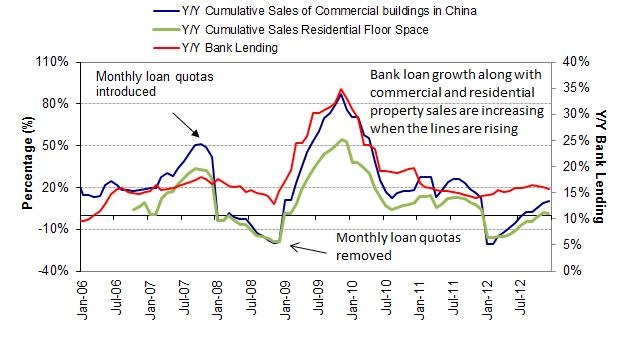

The country’s Communist leadership fears an uprising by the poorer rural masses could destabilize the country and unseat the party from power. Typically, the party relies on high levels of economic growth and low inflation to quell social tensions—the government can exert great influence over economic conditions on the ground. Simply, a housing bust and/or recession does Chinese new leadership little good, and it’s likely they could enact a number of monetary and/or fiscal measures to avoid one. In fact, the 2007-2009 financial crisis demonstrated just how fearful China is of such an event, as it massively increased loan growth and investments to stave off a recession (See Exhibit 2).

Exhibit 2: China Bank Lending and Property Sales

Sources: Thomson Reuters.

At some point, China will have to begin transitioning away from its infrastructure-dependent productivity growth model and adequately relax its capital account—which could cause housing prices to fall. In this sense, China’s current economic model is unquestionably unsustainable. With that said, the transition needn’t happen overnight and needn’t entail some sudden disaster. A slow, measured approach to transition the economy from its infrastructure dependent model towards one with higher levels of capital productivity, domestic consumption, investment and freer markets (with more investment options) is certainly possible—many nascent signs of which we’re just beginning to see today.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Oil Prices, UK Politics, Tech Stocks

2026-06-26

2026-06-26 -

Market Analysis Excess Fear Over ‘Excess’ Profits2026-06-25

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-23

-

In The News What ‘IPO’ really stands for — and whether you should be buying SpaceX and the AI giants2026-06-23

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today