Personal Wealth Management / Market Analysis

How Real Is China’s GDP?

Whether or not China's 6.9% y/y Q3 growth estimate is artificially high, the country should still contribute just fine to global GDP.

Downtown Shanghai, still bustling. Photo by Tomohiro Ohsumi/Bloomberg via Getty Images.

Chinese GDP beat expectations in Q3, growing 6.9% y/y and-in an odd twist-prompting a "hey, that's fast!" reaction from the financial media. Even though it's the lowest growth rate since 2009. But this wasn't a cheery "hey, that's fast"-it was laced with questions on the accuracy of China's data. Many suspect China's "real" (inflation-adjusted) GDP isn't all that, well, real. To us, the hubbub seems misplaced. It shouldn't be breaking news that a GDP report might not be airtight, regardless of the country producing it. Moreover, whether China grows 7-ish% or more like 5-ish%, it still contributes mightily to global growth and developed-world firms' revenues.

China's official economic figures often get a bad rap-partly because of the government's reputation for opacity, and partly because an infamous Wikileaked quote from current Premier Li Keqiang called China's GDP "manmade" and urged observers to use alternate stats like electricity generation, rail freight and loan growth. That 2010 leak spurred a veritable cottage industry specializing in "how fast is China really growing," and every quarter the analysts weigh in with their own estimates. Never mind, as Anatole Kaletsky recently pointed out at Project Syndicate, that the IMF's in-house estimates are largely in line with China's official figures.

The disbelief in China's GDP smacks of a behavioral error called confirmation bias: people's tendency to latch onto data that supports their belief and shun evidence that contradicts them. Kaletsky writes:

Many Western analysts, especially in financial institutions, treat China's official GDP growth of around 7% as a political fabrication - and the IMF's latest confirmation of its 6.8% estimate is unlikely to convince them. They point to steel, coal, and construction statistics, which really are collapsing in several Chinese regions, and to exports, which are growing much less than in the past.

But why do the skeptics accept the truth of dismal government figures for construction and steel output - down 15% and 4%, respectively, in the year to August - and then dismiss official data showing 10.8% retail-sales growth?

What's more, disbelieving pundits could very easily consult commentary from Western firms actually doing business there. We have, and their commentary doesn't suggest a marked slowdown is in the offing.

No GDP report anywhere in the world is perfectly accurate. It is simply impossible to record every last dollar[i] spent. US GDP for example, misses most of the so-called "sharing economy," informal transactions (like cash payments for some services), and many freelancers and self-employed folks. Kitchen-table entrepreneurs sold about $2 billion on Etsy last year, and GDP caught none of it. GDP is also subject to a fair amount of scrubbing from seasonal and inflation adjustments. Several years' worth of GDP were recently revised to fix some seasonal adjustment errors that understated wintertime growth. Heck, sometimes GDP is revised decades after the fact as statisticians change their minds about what should and shouldn't be included.

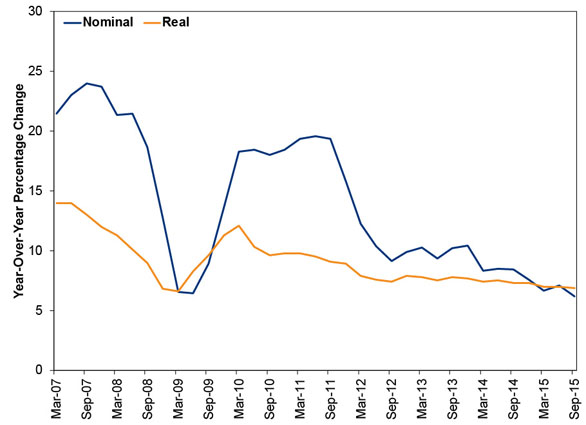

In China's case, most of the scrubbing comes from the inflation adjustment. Most agree China's nominal GDP figures are reliable, but they believe the "real" figures look a little too steady. (Exhibit 1) Q3's figures attracted extra scrutiny because real GDP exceeded nominal GDP, which grew just 6.2% (the lowest in 25 years). When real GDP exceeds nominal GDP, it means statisticians adjusted for deflation, which many consider odd since China's consumer inflation was positive all quarter, ranging from 1.6% y/y to 2.0% y/y. But producers' prices plunged more than -5% y/y all quarter, and the adjustments are supposed to account for price changes at all levels of the supply chain, so this isn't all that brow-raising. When you view sector-level GDP, only heavy industry got a bump up from the deflation/inflation adjustment. Agriculture and services were adjusted downward, which all seems fairly consistent with the divergence between consumer and producer prices.

Exhibit 1: Chinese GDP Growth

Source: FactSet, as of 10/19/2015. Year-over-year change in nominal and real GDP, Q1 2007 - Q3 2015.

Nor is it unusual for inflation adjustments to over- or under-state growth in general. Several prominent economists believe the US's GDP deflator has overstated inflation for decades, failing to appreciate how technology has improved the overall value of goods and services. As Martin Feldstein wrote in The Wall Street Journal in May , if a hospital stay is more expensive today, but the treatment is far more robust and effective, is it fair to look only at the nominal price increase? In China's case, statisticians are trying to track prices and development across a gigantic country with over 1 billion people, a rapidly developing service sector and a big informal sector. We'd find it more shocking if the inflation adjustments weren't fuzzy.

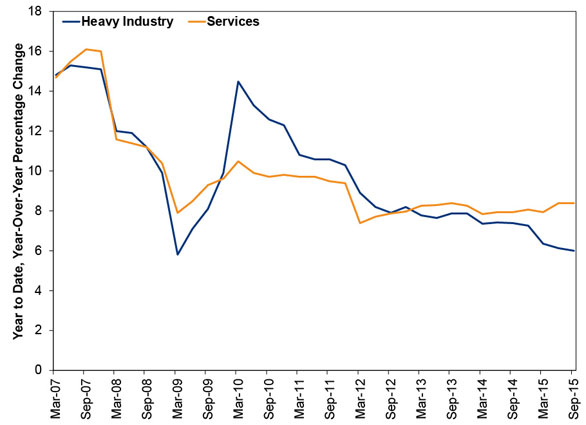

Viewing China's growth at a sector level offers an alternate, perhaps more illuminating perspective. As Exhibit 2 shows, service sector growth eclipsed heavy industry in Q1 2013 and never looked back. Through Q3, the service sector grew 8.4% year to date from 2014's first three quarters, compared to just 6.0% for heavy industry.[ii] This is yet another strong indication that China's slowdown stems from the ongoing shift away from investment, construction and factories to consumption and services, a point President Xi Jinping underscored after the GDP release. Slower growth is a function of economic reform, not a sign of fundamental weakness, and the widely feared hard landing remains as unlikely as ever.

Exhibit 2: Sector-Level Chinese Growth

Source: FactSet, as of 10/19/2015. Year-over-year growth in the year-to-date value added of the China's secondary (heavy industry) and tertiary (services) industries, Q1 2007 - Q3 2015.

Some fret China's services-led growth won't support the global economy as much as factory-led growth did, but that seems overstated. Yes, China's pure service markets (e.g., health care, financial services) are fairly closed to foreign competition, but foreign firms have a huge presence in China's retail sector, and China is gunning for a US-style consumption-driven economy.[iii] The more consumers ascend in China, the more demand there will be for all sorts of products from the developed world. The specific foreign sectors that benefit from China's growth might evolve, perhaps with miners enjoying less of a bump, but there should still be a big net positive. And these days, it isn't exactly news that commodity producers are hurting.

Overall, our take on China remains the same: Investors remain too dour, and reality likely continues beating expectations. That should be plenty good enough for stocks, which have known about the slowdown for years now. Even modestly slower Chinese growth should remain a big positive for the global economy and markets.

[i] Or yuan, pound, euro, yen, peso, real, krone, krona, ruble, ringgit, forint, baht, leu, etc.

[ii] The nominal numbers will probably seem wacky, but they are 3.5% for industry and 21.1% for services. Sharp swings in China's service sector nominal growth aren't unusual, but they still look odd on a chart.

[iii] Service-led and consumption-led growth aren't mutually exclusive, and there is actually a lot of overlap. There are simply two main ways of breaking down GDP: output-based and expenditure-based. Output-based GDP tallies the value added from agriculture, heavy industry and services. Expenditure-based GDP tallies all spending and investment from households, businesses and the government, along with net trade.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why Gas Prices’ Big March Swing Barely Registered at Other Retailers2026-04-21

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—April 13 - April 172026-04-20

-

Market Analysis Easing Hormuz’s Grip for the Long Term2026-04-20

-

Expert Commentary Q1 Earnings, April PMIs, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-20

2026-04-20

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today