Personal Wealth Management / Politics

How Tuesday's Brexit Vote Solved Everything and Nothing

Tuesday’s big vote perhaps made a second referendum or Brexit delay much less likely, but big questions remain.

As you may have heard, UK parliamentarians (MPs) gathered this evening to vote on a smorgasbord of amendments to Prime Minister Theresa May’s “Plan B” for Brexit following the defeat of her deal with Brussels two weeks ago. Plan B looked a lot like the initial deal, plus a few small concessions aimed at rallying support from the pro-Brexit wing of May’s Conservative Party and perhaps a few from the opposition Labour Party. That was too close to the status quo for many MPs, who tabled 14 amendments this week. House of Commons Speaker John Bercow selected seven for a vote, but once MPs had their say, only two passed—two that don’t much change the calculus. These votes appear to take some of the more extreme options off the table, perhaps reducing uncertainty a bit, but the endgame remains unclear. With the next vote—the much-anticipated “meaningful vote”—set for mid-February, it will be at least a couple weeks before businesses, investors and markets get a better view of the lay of the land.

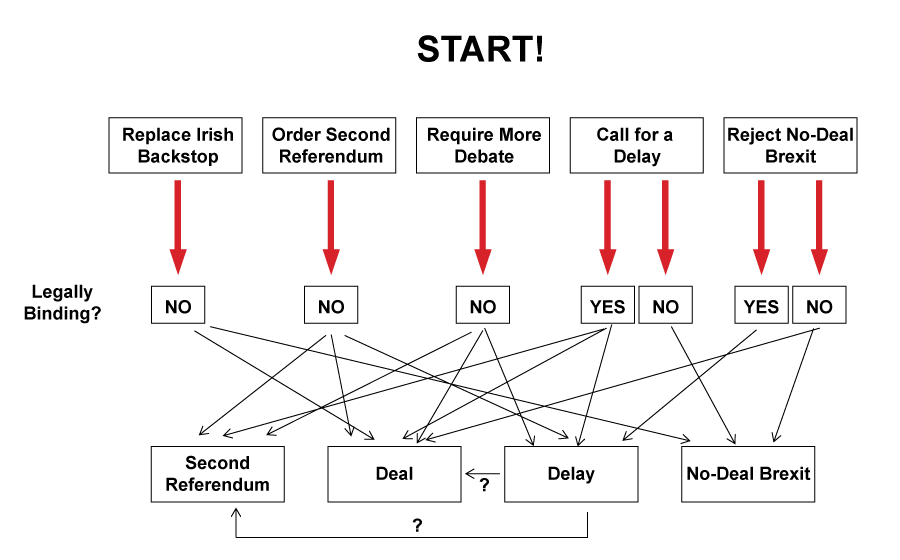

Exhibit 1 is a reductive flow chart summarizing the many confusing ways Brexit could have gone before today’s vote. The starting point is May’s Plan B—her original deal, plus provisions giving MPs more input into a potential free trade deal with the EU, pledging to renegotiate the Irish backstop and increasing protections for workers. The second row is an oversimplified aggregation of the proposed amendments, which combines overlapping amendments into general categories in order to avoid hurting readers’ eyeballs with four different extend the Brexit deadline amendments. The third row specifies whether each would have been legally binding. The fourth, at last, attempts to show how all led, in different ways, to one of four outcomes: a Brexit deal, a delay, a no-deal Brexit and a second referendum. As you will see, the possibilities were perhaps juuuuuuuuuuust a bit hard to keep track of.

Exhibit 1: An Oversimplified Rendering of Those Brexit Amendments

Source: The Telegraph and amateur graphic design by non-graphic designer Elisabeth Dellinger, as of 1/29/2019.

In the end, only two passed: Dame Caroline Spelman’s nonbinding rejection of a no-deal Brexit and Sir Graham Brady’s requirement that May replace the Irish backstop with “alternative arrangements.” The latter, which May’s government supported, may seem redundant considering a pledge to renegotiate the backstop was part of Plan B. But May’s initial provision didn’t go far enough for the pro-Brexit wing of her party, as it didn’t commit to changing the Withdrawal Agreement’s legal text. A few dozen MPs worried all she would get from the EU was nonbinding political statements that wouldn’t guarantee against the backstop’s less satisfactory (in their mind) provisions. So they tabled the amendment, which requires changes to the legal text and pre-pledges MPs’ support for the amended agreement. This compromise would theoretically seal the meaningful vote in two weeks.

We say “theoretically” because it, too, is nonbinding. It also seems too vague to mean much, as “alternative arrangements” could mean anything. Adding a wrinkle, the EU’s response was a swift um, no, we aren’t reopening the Withdrawal Agreement. It takes two to tango, and EU leaders aren’t beholden to nonbinding acts of the UK Parliament. They also seem to find “alternative arrangements” as vague as we do and don’t appear confident they can concede anything that would have a snowball’s chance of passing Parliament.

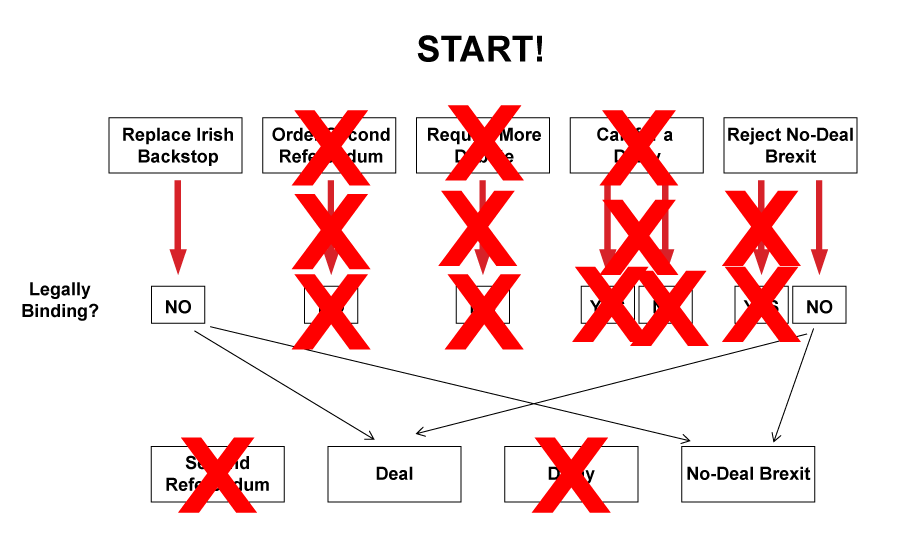

Which leaves us in the same place we were two weeks ago—sort of. While this wasn’t MPs’ last chance to tack on amendments, MPs’ solid, repeated rejection of delaying Brexit and opening the door to a second referendum likely means those possible outcomes are all but DOA. Yes, the Brexit circus is crazy enough that we aren’t ruling anything out. Yet the relevant amendments failed by dozens of votes, and it would take a big swing for them to go differently next time. Thus, it seems likely markets can narrow the field to Brexit happening on March 29 with a deal—or Brexit happening on March 29 without a deal. Obviously, this doesn’t enable businesses to start executing contingency plans. But it does give them a few less crazy outcomes to twist their hands over. Or, if you prefer:

Exhibit 2: An Oversimplified Rendering of Those Brexit Amendment Results

Source: The Telegraph and amateur graphic design by non-graphic designer Elisabeth Dellinger, as of 1/29/2019.

So stay tuned as Mrs. May goes to Brussels and tries to negotiate with EU leaders once again, and check back for fresh commentary on next month’s meaningful vote, which will hopefully not require as many complex flow charts.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics A May Global Economic Check-In2026-05-26

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 18 - May 222026-05-26

-

In The News How to think about the Iran war — and what it means for oil and stocks2026-05-25

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, US Q1 GDP, Graduation Season

2026-05-25

2026-05-25

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today