Personal Wealth Management / Market Analysis

In Depth: PIIGS Debt

One way to sift through the volume of data on PIIGS debt is to look at debt due in 2012.

The challenges various PIIGS nations face with respect to their individual sovereign debt levels are of course well known. But amid all the numbers discussed by the media, what should investors make of the actual magnitude of their debt woes? One way to break it down is looking at debt due in 2012.

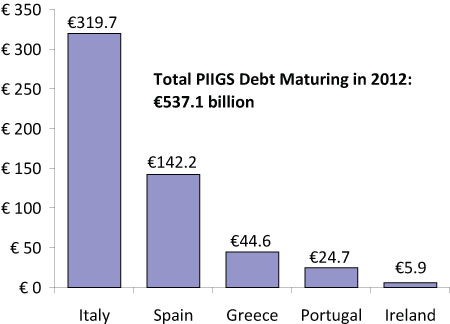

There’s an estimated €537.2 billion of PIIGS debt maturing in 2012 (see Exhibit 1)—the majority (86%) owed by Italy and Spain combined. While that may sound like a daunting sum, demand for Italian and Spanish debt at recent auctions has been fairly strong, and yields have largely retreated from recent highs.

Exhibit 1: PIIGS Debt Maturing in 2012

Source: Bloomberg.

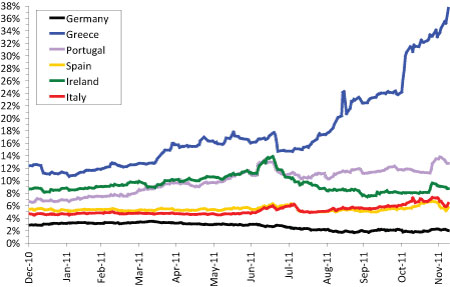

As shown in Exhibit 2, yields on the European periphery’s debt have shown significant volatility recently. And when Italian yields recently hit the 7% mark (prior to falling again), there was considerable consternation in the media—in our view, mostly tied to the fact Portugal and Greece were bailed out when yields were around 7%. But that coincidence doesn’t necessarily mean 7% automatically triggers a bailout across the European periphery.

Exhibit 2: 10-Year Benchmark Sovereign Yields (Since 12/31/2010)

Source: Thomson Reuters, as of 12/8/2011.

In a recent article, we discussed Italian debt and explained why Italian yields at 7% aren’t great, but they’re likely not as disastrous as many think. Which leaves the question: What about Spain?

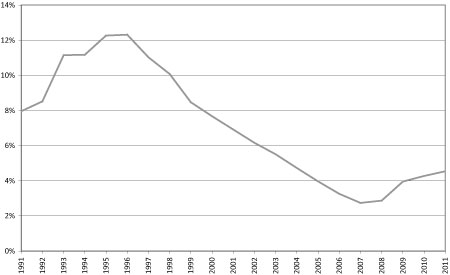

The current average interest rate on Spanish debt is 3.98%—but not all of their debt must be refinanced this year. Assuming all of Spain’s debt due in 2012 (€142.2 billion) rolls over at 7%, the increased interest expense amounts to €4.3 billion, or roughly 0.4% of Spanish GDP—meaning it would be even less impactful for Spain. Now, to be sure, it’s unlikely rates wouldn’t move throughout 2012—they could go lower or higher. But importantly, Spain currently has less than half Italy’s debt-to-GDP ratio and, as shown in Exhibit 3, Spanish interest payments amount to roughly 5% of Spanish federal government tax revenue. That’s less than half the cost during the mid-1990s—and is lower than America’s 9% level and Italy’s 10% level.

Exhibit 3: Spanish Net Debt Interest Payments as % of Government Revenue

Source: IMF and OECD.

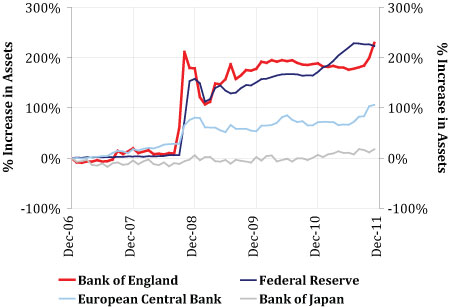

Furthermore, the European Central Bank (ECB) has been buying Italian and Spanish debt in the secondary market as a way to help keep those countries’ borrowing costs lower. If conditions were to worsen for either country, the ECB could conceivably increase those debt purchases. Compared to the Federal Reserve and the Bank of England, the ECB’s been relatively restrained in terms of expanding its balance sheet since 2007 (see Exhibit 4), seemingly making increased bond buying a possibility.

Exhibit 4: Central Bank Balance Sheet Expansion

Source: Thomson Reuters.

But what about Greece, Portugal and Ireland? Since they’ve already been bailed out, they’re not currently financing themselves through debt auctions, avoiding the scrutiny of free-market set rates.

Certainly, materially higher rates for a sustained period from here for both Italy and Spain would be problematic. But this analysis shows at current levels or a bit higher, the debt load they must refinance in 2012 should be manageable.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Don’t Doubt the Old World2026-07-16

-

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today