Personal Wealth Management / Market Analysis

Weighing Italy’s Debt

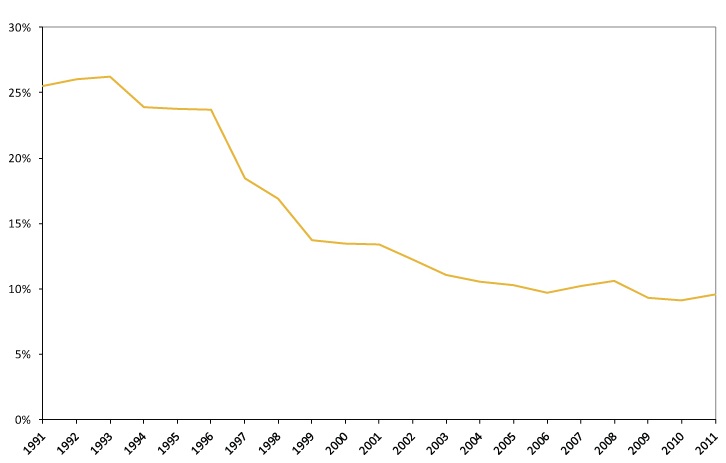

An alternate perspective of Italy’s debt costs shows today’s levels are low by historical standards.

The tempered optimism that greeted last week’s EU summit appeared short-lived Monday as headlines again fretted Italian debt. Monday’s short-term debt auction was decently successful—yields down a bit from last month with robust demand (nearly two times supply)—but longer-term yields remained near 7% on the secondary market. Some posit that doesn’t bode well for Wednesday’s €3 billion auction of five-year debt, and they fear Italy’s debt-service burden will rise as more debt is rolled over in 2012.

As we recently wrote, it’s important to scale Italy’s debt service costs—Italy doesn’t pay 7% on all outstanding debt. The average cost of all outstanding Italian debt is closer to 4%. Secondary market rates tell us more about what yield investors might demand on new Italian debt, so today’s rates suggest Italian debt will likely get more expensive as €319.7 billion in maturing debt is rolled over in 2012.

European sovereign bond yields have been anything but static recently, and it’s unlikely they remain exactly at current levels throughout 2012—they could move lower or higher. But for argument’s sake, suppose all €319.7 billion rolls over at 7%. The additional annual interest (above today’s 4% average) would be around €10 billion annually. No doubt, new Prime Minister Mario Monti wants to avoid this, but how much of an extra burden is it, really? About 0.8% of Italy’s GDP. Not great, but not disaster either.

Here’s another way to assess the affordability of Italy’s debt: compare it to tax receipts. Exhibit 1 shows Italy’s debt service costs as a percentage of government revenue since 1991.

Exhibit 1: Italy’s Net Debt Interest Payments as a Percentage of Government Revenue

Sources: IMF, OECD. Relative to revenue, today’s interest payments are pretty low—less than half of early-to-mid 1990s levels, and Italy met its obligations back then. €9.6 billion more in interest costs would raise the curve in 2012 but likely nowhere near the peak—and again, it’s not guaranteed the marginal increase will be that high. Plenty of as-yet-unknown events could drive rates lower (or, yes, higher).

Plus, yields aren’t the sole variable. Revenues also matter, and the revenue enhancements included in last week’s austerity package could help offset higher interest costs. (The operative word being “could”—at this point it’s hard to handicap Italy’s success in enacting austerity measures.) These include not only higher taxes, but measures to lower tax evasion. For instance, as we wrote last week, the maximum allowable cash payment will drop from €2,500 to €1,000. Theoretically, this should increase the amount of larger transactions that leave a paper trail, helping less fall through the cracks, though its efficacy remains to be seen—many larger cash transactions take place in the shadow economy, and it seems unlikely those folks suddenly start complying with government rules. Still, that officials understand the need to tackle corruption is encouraging.

Over time, austerity alone likely won’t boost revenues enough to erode Italy’s outstanding debt. The economy also must grow, and faster than in recent years (remember, growth increases the tax base, which drives revenue). Some of last week’s reforms were a start, like the €2 billion in tax incentives for firms to hire and the increased loans for small businesses. Labor market reforms are also pending, likely making it easier for firms to hire and fire—which should help them function more efficiently.

Near term, Italy can likely continue meeting its obligations. But it’s not out of the woods. Its ongoing commitment to reform will be a story to watch in 2012.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Don’t Doubt the Old World2026-07-16

-

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today