Personal Wealth Management / Economics

Infatuated With Inflation

There is no mystery behind persistently low inflation readings.

Besides questions about the next rate hike, how do you stump a Fed official? Ask them what's happening with inflation. Myriad theories abound about why CPI readings remain persistently low despite all the predictions that accommodative monetary policy would boost inflation. Some blame US fiscal policy while others think demographics play an underappreciated role. Many presume the low readings are a sign the US economy is in a fragile state. But in our view, all these interpretations overthink what's happening with inflation-the reality is much less complex, and it doesn't say really anything about US economic health.

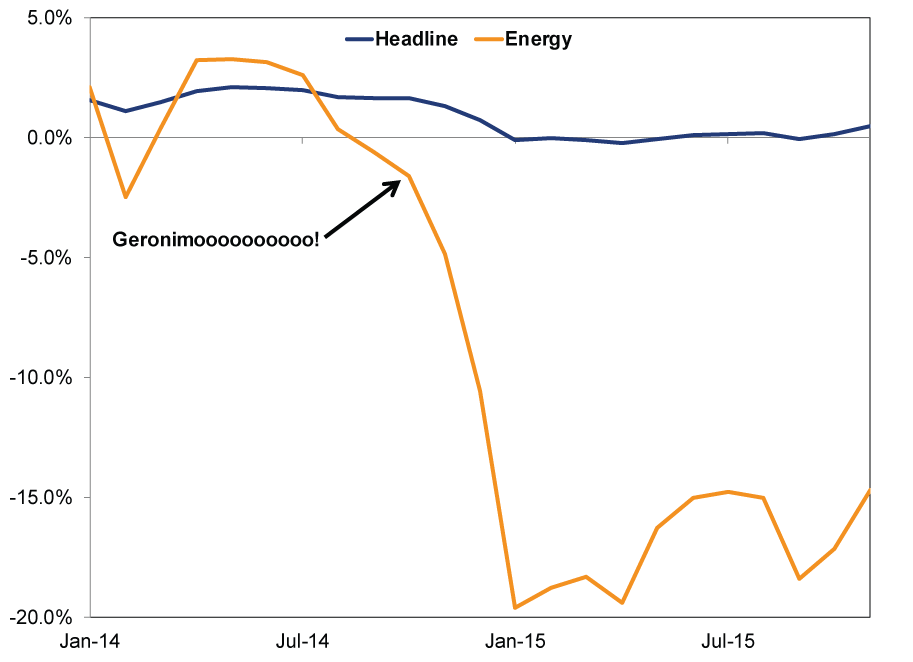

Here is a newsflash that isn't really a newsflash: The skew in headline CPI is largely due to falling energy prices, not exactly a surprising development. November headline CPI rose 0.5% y/y (flat month-over-month), while Energy CPI plummeted -14.7% y/y (-1.3% m/m). Since the summer of 2014, energy prices-highlighted by oil-have tumbled considerably, putting a big deflationary pressure on headline CPI. (Exhibit 1)

Exhibit 1: Annual Headline vs. Energy CPI Since 2014

Source: St. Louis Federal Reserve, as of 12/15/2015. CPI: All Items and CPI: Energy, not seasonally adjusted, y/y percentage change, from January 2014 - November 2015.

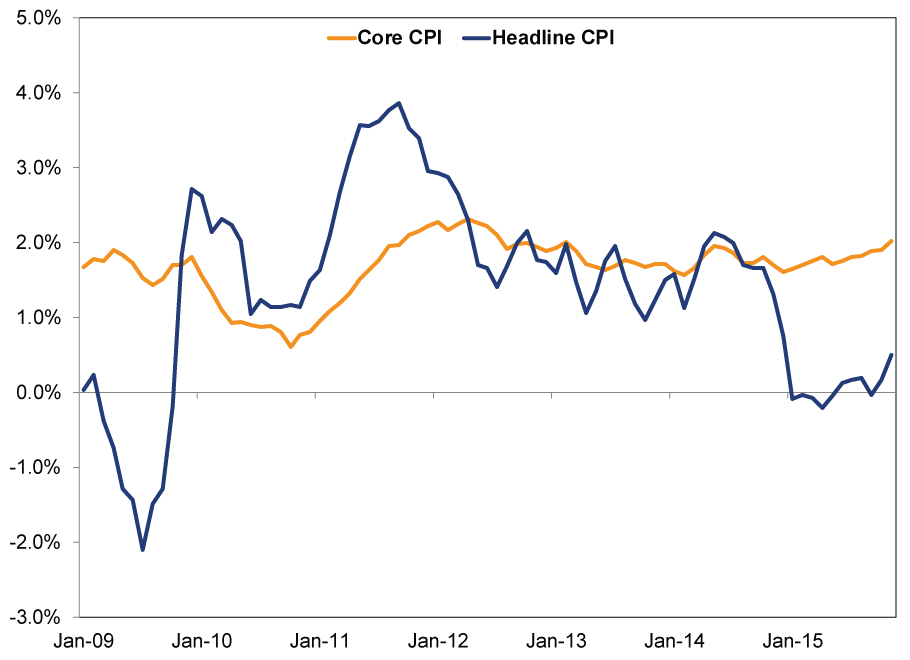

But if you strip out volatile energy and food prices-core CPI-inflation has been much less jumpy and closer to the Fed's stated goal of 2% annual inflation.[i] In November, core CPI actually sped to 2.0% y/y (0.2% m/m)-in line with its recent trend. (Exhibit 2)

Exhibit 2: Annual Headline vs. Core CPI Since 2014

Source: St. Louis Federal Reserve, as of 12/15/2015. CPI: All Items and CPI: All Items excluding Energy and Food, not seasonally adjusted, y/y percentage change, from January 2014 - November 2015.

So the primary reason headline CPI has stubbornly refused to rise higher: one big deflationary input and the math for CPI's year-over-year calculation. No huge mystery there.

Aside from Energy's recent deflationary impact, headline CPI tends to be noisy overall. See how headline CPI has bounced around throughout this bull market compared to core CPI. (Exhibit 3)

Exhibit 3: USAnnual Headline vs. Core CPI Since 2009

Source: St. Louis Federal Reserve, as of 12/15/2015. CPI: All Items and CPI: All Items excluding Energy and Food, not seasonally adjusted, from January 2009 - November 2015.

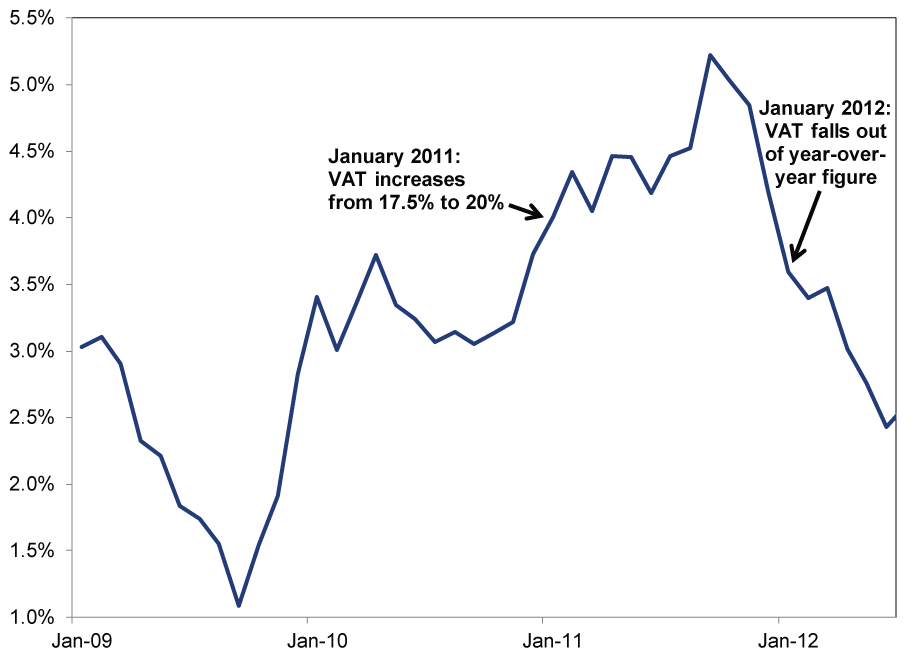

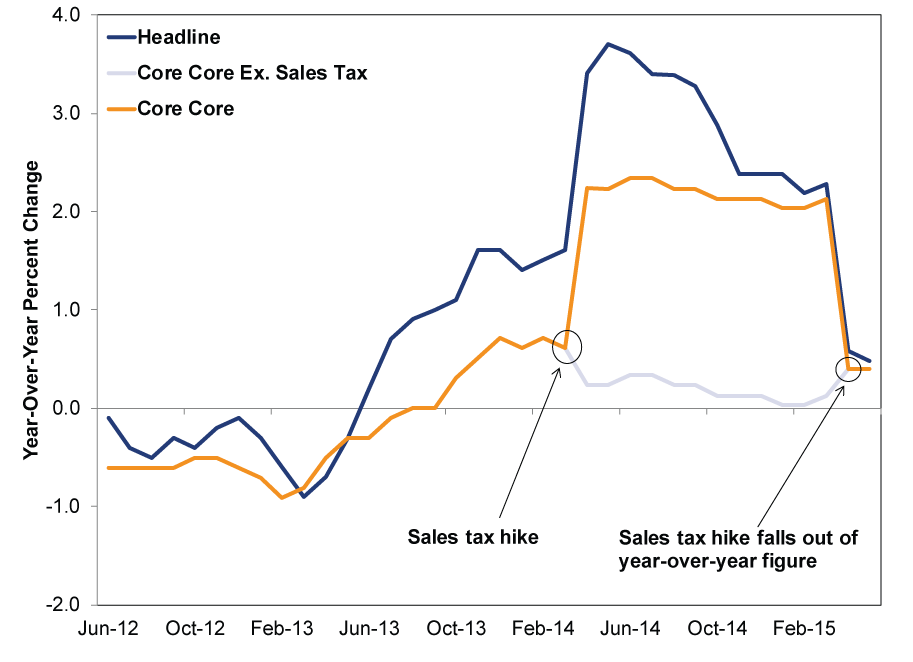

During the bull's first several years, Energy CPI fluctuated greatly-impacting the headline number-thanks largely to changes influencing the year-over-year comparisons. In 2009, weak Energy prices reflected tepid demand as the economy was coming off the recession's lows. Compare that to 2011, when a jump in prices skewed the numbers. But it isn't just Energy prices that can knock the headline CPI figures: other external one-off factors can, too. Consider the impact of the UK's Value Added Tax (VAT) in 2011 or Japan's sales tax hike in 2014. (Exhibits 4-5)

Exhibit 4: The Impact of the UK VAT on Headline CPI

Source: The Office for National Statistics, as of 12/15/2015. Consumer Prices Index (overall index) from January 2009 - June 2012.

Exhibit 5: The Impact of Japan's Sales Tax Hike on CPI

Source: FactSet as of 7/24/2015. Japanese CPI, CPI ex. energy and food, and CPI ex. energy, food and the sales tax hike. June 2012 - May 2015.

With headline CPI subject to great volatility, we caution investors from reading too much into the noise, which can distract from what inflation really is. For the myriad overcomplicated inflation theories and interpretations, Milton Friedman summarized it best: Inflation is always and everywhere a monetary phenomenon of too much money chasing too few goods. This goes to the basic relationship of supply and demand. When you have a growing money supply chasing a limited set of goods and services, those goods and services will demand more money from consumers-i.e., prices will rise. Inflation! However, one-off, non-monetary events can temporarily skew inflation indexes. For example, when the UK raised its VAT in 2011 or Japan hiked its sales tax in 2014, businesses passed some of those expenses to consumers, boosting prices. Eventually, though, that cost gets absorbed in the CPI readings and falls out of the calculation-reflected by the subsequent drop a year later.

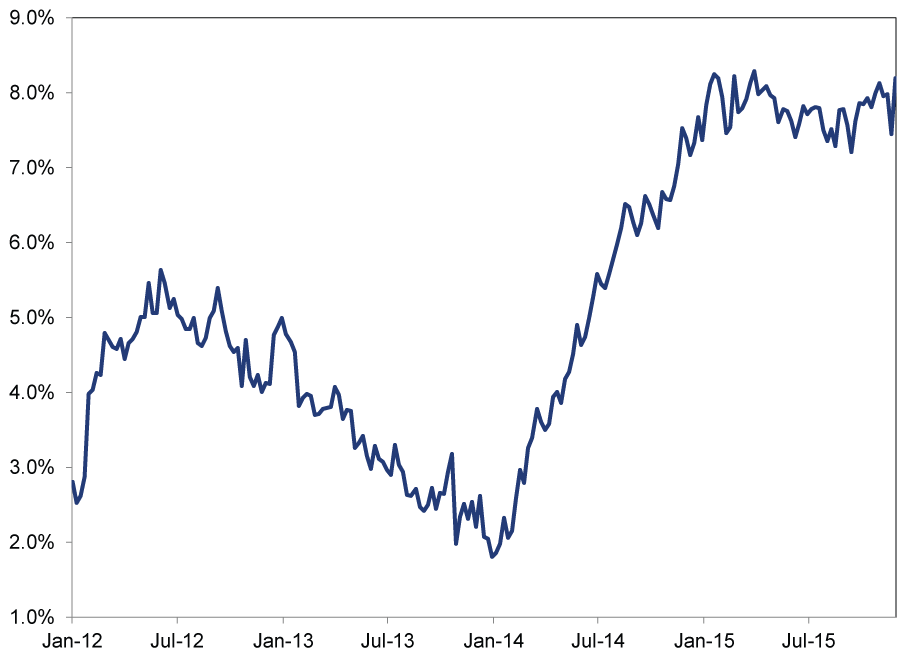

But as noisy as CPI readings can be, other monetary factors are consistent with a rising money supply-a good setup for modest inflation and continued economic growth. The yield curve remains steep and positively sloped, a good sign for future lending and credit availability. US M4-the broadest measure of money-rose 4.6% y/y in November, the fastest rate in more than two years.[ii] Loan growth has picked up considerably, too, over the past two years, notching 8.2% y/y for the week ending December 2-in line with strong growth throughout the year. (Exhibit 6)

Exhibit 6: Total Year-Over-Year Loan Growth at US Banks

Source: St. Louis Federal Reserve, as of 12/16/2015. Loans and Leases in Bank Credit, All Commercial Banks, weekly. January 4, 2012 - December 2, 2015.

So while the experts remain fixated on inflation, we suggest investors take in the bigger picture: One gauge's bounciness-tied to well-known factors- is no reason to fret the current or future state of things. The US economy has been one of the world's strongest during the current expansion, and the current "weak" inflation readings don't contradict that story.

[i] Albeit, the Fed prefers another inflation gauge-personal consumption expenditures, and for some reason, they look at headline, not core.

[ii] Source: The Center for Financial Stability, as of 12/16/2015.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Reader Mailbag: June 20262026-06-30

-

Market Analysis Investors Are (Still) Fighting the Last War on Inflation2026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today