Personal Wealth Management / Market Analysis

Interest Rates Influence, but Don’t Dictate, Stock Market Trends

“Yield chase” theory’s inability to explain leadership trends illustrates the issues with overrating interest rates’ ability to sway stocks.

Ten months into 2020, global high dividend yielding stocks are trailing their non-high-yielding brethren by a significant margin. Including reinvested dividends, the MSCI World High Dividend Yield Index is down -8.0% thus far this year—while the MSCI World itself is up 5.5%.[i] Some might see this as a reminder that there is no automatic superiority to high dividend stocks—which is a valid point. But there is another angle to this that we find more interesting: It undercuts the notion that low interest rates fuel a hunt for yield, driving stocks up and leading dividend payers to outperform. Interest rates are important, but they don’t dictate stocks’ direction alone.

For most of the last decade-plus, short- and long-term interest rates have been low by historical standards. In the last bull market, this led many pundits to presume investors were selling low-yielding bonds and buying dividend paying stocks—the much-ballyhooed “hunt for yield.” Many claimed these low rates fueled stocks’ rise from 2009 to early 2020.

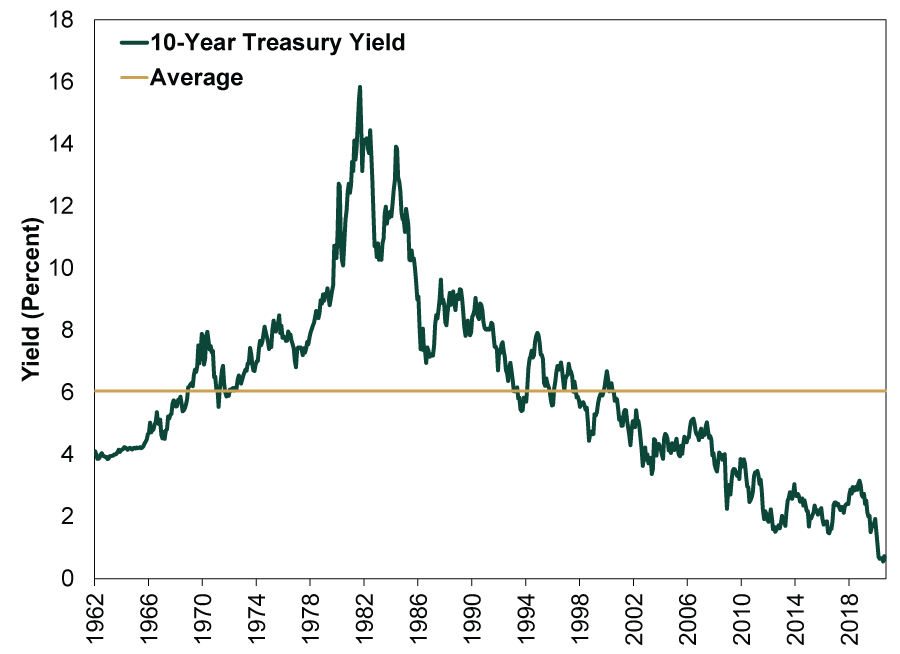

Exhibit 1: Rates Have Been—and Most Certainly Are Now—Historically Low

Source: FactSet, as of 10/15/2020. 10-Year US Constant Maturity Yield, January 1962 – September 2020.

While there is little doubt that some investors did chase yield in this (inadvisable) fashion, we have long been skeptical of theories extrapolating this to a broad market impact. Most investors simply don’t swap their allocations in this manner due to yields alone. Some institutions employ asset allocation mandates that won’t flop because rates drop.

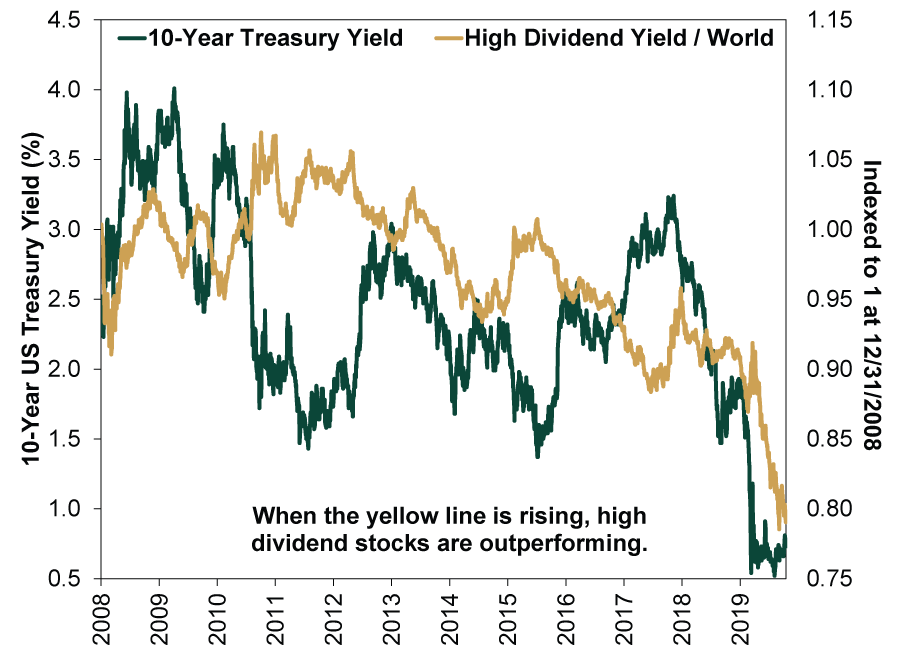

This year, US Treasury yields have plunged to record lows—which, if yield-chase theories hold true, should fuel a rush to yield stocks. Obviously, that hasn’t happened. Some might say this is because firms have been slashing dividends, by choice or government edict, this year. Yet that supposes low and falling yields would have correlated with rising dividend stocks prior to COVID. The data don’t show this. Exhibit 1 plots the MSCI World High Dividend Yield Index divided by the MSCI World Index (after indexing both to 1 at 12/31/2008) and the 10-Year US Treasury yield. As you can see, during the last bull market there were several short spurts in which dividend stocks outperformed alongside falling yields (like 2011 and 2016). But there are as many or more in which rates (dark green line) fall while dividend stocks lag. This year is extreme, with rates falling a lot while dividend stocks lag bigtime. But the longer history shows no set influence—undercutting yield-chase theory.

Exhibit 2: No Relationship Between Low and Falling Yields and Dividend Stocks

Source: FactSet, as of 10/15/2020. MSCI World High Dividend and MSCI World Index returns with net dividends, 12/31/2008 – 10/14/2020. Indexed to 1 at 12/31/2008. 10-Year US Constant Maturity Yield, 12/31/2008 – 10/14/2020.

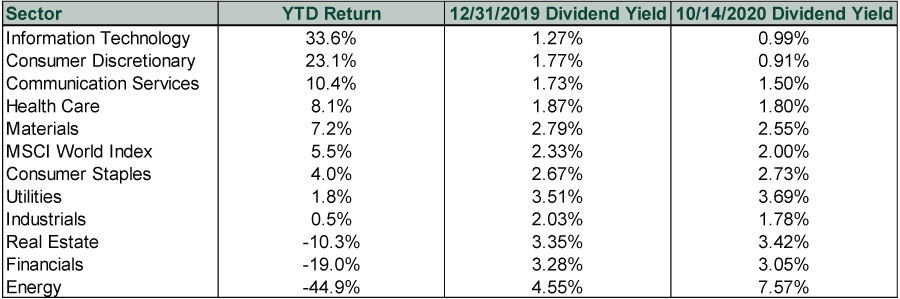

To further illustrate dividend stocks’ year-to-date lag, consider sector returns. As Exhibit 3 shows, sectors that pay dividends higher than the broad MSCI World Index’s average are lagging this year almost uniformly.

Exhibit 3: Sector Returns and Dividend Yields

Source: FactSet, as of 10/15/2020. MSCI World and MSCI World sector returns from 12/31/2019 – 9/30/2020 and and trailing 12-month dividend yields on 12/31/2019 and 10/14/2020.

Accordingly, pundits have seemingly shifted their theory. No longer do many argue low yields benefit dividend payers. They now mostly argue low rates are great for Tech and growth stocks, ignoring the yield-chase narrative so many touted during the bull market that ended not even a year ago. In our view, this newfangled theory gives rates a bit too much influence in the grand scheme of markets. In that way, it makes the same fundamental mistake yield-chase theory made before it.

[i] Source: FactSet, as of 10/15/2020. MSCI World High Dividend Yield Index and MSCI World Index, 12/31/2019 – 9/30/2020.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03 -

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Analysis Reader Mailbag: June 20262026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today