Personal Wealth Management / Market Analysis

Into Perspective: Markets and Impeachment

For investors, history can add some valuable perspective to the firing of FBI head James Comey.

Photo by John Sorrell/iStockPhoto.

As a reminder, our political analysis is nonpartisan and focuses exclusively on political developments' potential market impact (or lack thereof). We favor no party, politician or ideology and believe political biases lead to investing errors. For details on why we believe it's important for investment advisers to help clients avoid acting on political biases during the course of their work, read Fisher Investments CEO Damian Ornani's InvestmentNews article.

2016's US election was odd in many ways, one being Russia's hacking the Democratic National Committee and dumping a spate of embarrassing emails via Wikileaks weeks before the vote. Since Donald Trump won November 8, many have wondered about possible connections between the Russian hacking and the Trump campaign, perhaps including the president himself. Throughout, Trump has dismissed the connection. Nevertheless, up until Tuesday, FBI Director James Comey was investigating.

As you are likely aware, his investigation ended Tuesday, when Trump fired him at Attorney General Jeff Sessions' urging, setting off a gigantic media firestorm eclipsing basically all other news. With it came speculation that this was Trump's "Saturday Night Massacre," recalling former President Richard Nixon's October 1973 firing of a special prosecutor assigned to investigate Watergate. As a result, many are beginning to wonder what a Trump impeachment might mean for stocks. In this piece, we aim to use history to hopefully put the current talk into perspective.

Before we launch into that, let's be clear: Right now all the impeachment talk discusses something possible-not probable. In investing, probability is what matters. Investing based on possibilities would mean never owning anything, because it is always possible stocks fall to zero. It is always possible a meteor slams into Earth. Negative and positive possibilities can never be excluded.

So the question isn't, "Could Comey's firing mean we are facing another Watergate?" but "How likely is it-based on the evidence we have now-that impeachment looms?" The answer: Not likely at all. Note, we aren't making a political prediction here-rather, weighing recent events relative to history, while acknowledging new evidence could arise later to tip the scales.

Comey's firing occurred amid whispers, rumors and an FBI investigation of said whispers and rumors. By contrast: When Nixon fired Watergate special prosecutor Archibald Cox on October 20, 1973,[i] all of the following (and more!) had already occurred:

- The appointment of said special prosecutor.

- A Watergate burglar was proven to have deposited a $25,000 check from the Nixon campaign into his personal bank account.

- Nixon's campaign head and former Attorney General John Mitchell had been implicated in the case publicly.

- Three senior White House staffers had resigned related to Watergate.

- Televised Senate hearings involving the administration were underway.

- The existence of Richard Nixon's secret Oval Office recordings was revealed, which he promptly refused to surrender to the investigation.

This last point is the issue that led to Cox's firing and the abolition of the Watergate special prosecutor's office. Moreover, the Democrats controlled the House and Senate during this period, giving them greater power to pressure Nixon's administration.

You may already see some distinctions between the current situation and those days: One, the Republicans control Congress now (although this is mitigated some by intraparty strife). Two, there was a special prosecutor for Watergate. Nixon could not claim, as Trump can, the termination was tied to other matters. There were no other matters. Three, he was fired after requesting very specific evidence, and only after a slew of other evidence had emerged. As of now, about the only concrete evidence connecting the Trump campaign to Russia is one Michael Flynn, fired some months ago.

To be utterly, crystal clear: We have no idea how high up this stuff goes. But the evidence available now says no one who wasn't a direct participant has any idea either. Heck, just a couple months ago Democrats probably would have been overjoyed if Trump fired Comey. We get that the timing is key, but if that's the only evidence of wrongdoing, you don't have much at all. Speculating about motives and outcomes, as many seem wont to do now, is a waste of time.

With that out of the way, let's get into what-ifs: What if Trump is impeached-how have stocks historically reacted to impeachments or similarly high-profile scandals? The unfortunate answer when we shook our magic 8-ball of market history is: It's unclear.

There are only a tiny number of historical scandals that come close to impeachment level: Watergate, of course. Bill Clinton's impeachment in 1998. Andrew Johnson's impeachment in 1868. Perhaps, stretching a little, the 1920s' Teapot Dome scandal involving Warren Harding's administration[ii] and Iran-Contra involving Ronald Reagan in the 1980s. Outside America, we've had two impeachments in the last twelve months-Brazil's Dilma Rousseff and Korea's Park Guen-hye. But other than that, we've got very little from a country even close to as developed as America.[iii] Whatever the findings about market impact, this dataset is too small to draw any conclusion.

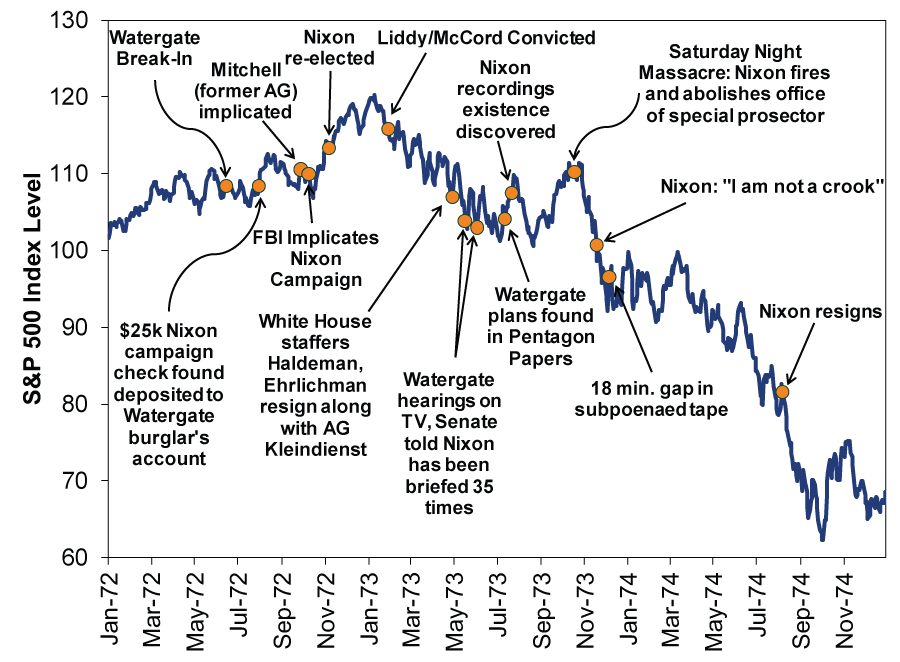

WATERGATE

The first thing to remember about Watergate: Nixon was never impeached. He resigned before impeachment was initiated, following a two-year investigation. Much, though not all, of this period coincides with the big 1973 - 1974 bear market. (Exhibit 1)

Exhibit 1: Watergate and the S&P 500

Source: Global Financial Data, Inc., as of 4/20/2017. S&P 500 Price Index, 1/1/1972 - 12/31/1974. Events and dating sourced from The Washington Post's Watergate Timeline, accessible here.

But a slew of other negatives also coincide: Nixon expanded and extended price controls in January 1973, right when stocks peaked; OPEC's oil embargo and resulting global fuel shortages began in the middle of this bear; the Nifty Fifty equity market bubble burst. While rising political uncertainty tied to Nixon's plight likely played a role in the downturn, it is a mistake to presume 1973 - 1974 was all about that.

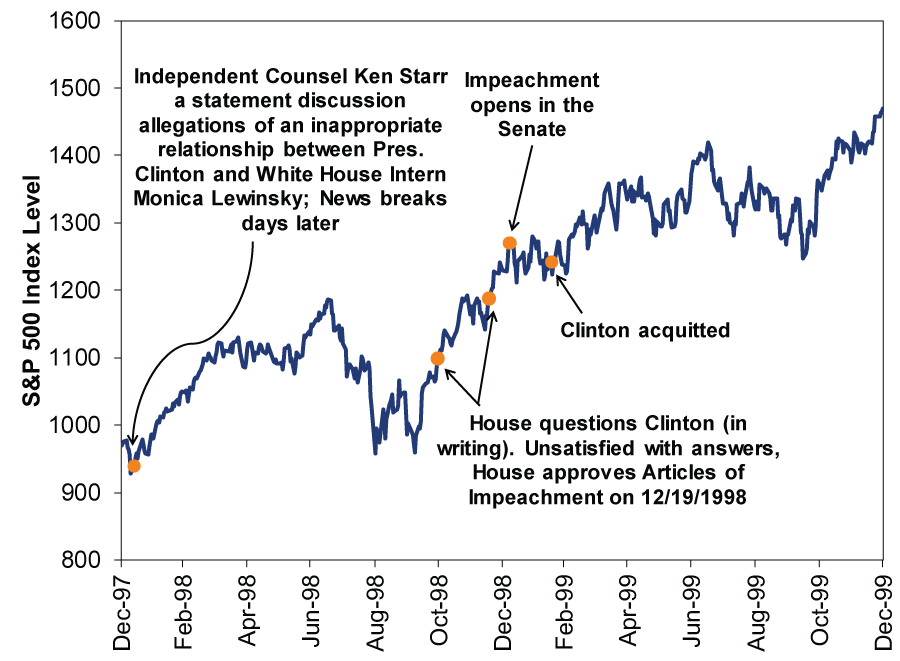

CLINTON IMPEACHMENT

While Watergate seems to have to been negative, one can't say that of the only modern impeachment to occur-the Clinton impeachment over perjury and obstruction of justice during the Lewinsky affair in the late 1990s. From the moment the scandal broke through Clinton's February 12, 1999 acquittal, the S&P 500 rose 28% in price terms. As Exhibit 2 shows, stocks barely reacted to major developments. 1998's correction-beginning long after the scandal began-was tied to the Asian currency crisis and Russian default.

Exhibit 2: The Lewinsky Affair

Source: FactSet, as of 5/10/2017. S&P 500 Price Index, 12/31/1997 - 12/31/1999. Events and dating sourced from CUNY Brooklyn History Professor KC Johnson's timeline, accessible here.

Similarly, Iran-Contra broke in the mid-1980s and does not coincide with negativity. While data are dodgy regarding the early 1920's Teapot Dome scandal, they do not show a bear market occurring then either. As for Andrew Johnson's 1868 impeachment, some pundits suggest markets were weak in the month between the Articles of Impeachment passing and the hearings, but data that old are totally unreliable. American equity markets then were basically a handful of railroads and a bank.

Korea and Brazil suggest a similarly mixed bag. Korean stocks fell after former President Park Geun-hye was implicated in a very odd scandal involving a Rasputin-like figure, but started rising before impeachment proceedings even opened. As for Brazil's Rousseff, markets celebrated her impeachment, perhaps because she was seen as very anti-business.

So, ultimately, whichever direction you think the current Trump/Russia/Comey debacle is headed, we'd humbly suggest you not factor this into portfolio decisions. An impeachment is only a possibility, and even if it happens, the evidence is too sparse, contradictory and unclear-not something you can position portfolios for.[iv]

[i] As well as several senior Department of Justice staffers who refused to deliver that message to him.

[ii] Teapot Dome was essentially a bribery scandal, in which oil executives gave interest free "loans" to Warren Harding's Secretary of the Interior, Albert Fall. Fall, in turn, secretly gave these firms exclusive access to Naval oil reserves in Wyoming and California. It was a big deal.

[iii] Iran in 1981, another Brazilian one in 1992, the Philippines in 2000, Lithuania in 2004, two Romanias and a Paraguay.

[iv] PS: Those thinking this would be bad for stocks given the Trump Trade should really read this now or watch this.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Reviewing Q1 Earnings and What Q2 Expectations Say2026-06-18

-

Market Analysis Kevin Warsh and the Magical Delete Button2026-06-17

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

-

Market Analysis Gold Fails the Safe Haven Test Again2026-06-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today