Personal Wealth Management / Market Analysis

Investing Lessons From India’s Currency Kerfuffle

What's the best move when a sudden reform in an otherwise healthy market looks like it's going badly?

Last month, Indian Prime Minister Narendra Modi went on television with a surprise announcement: 500- and 1000-rupee notes[i] would soon no longer be legal tender, leaving folks with 50 days to swap them for new 1000- and 2000-rupee notes.[ii] As an effort to smoke out criminals and tax evaders, it seemed promising enough, but the chaotic rollout brought much of the country to a standstill, hitting Indian stocks. When weird shocks like this happen, it's easy for investors to jump the gun and overlook positive long-term drivers, like India's fast-growing economy and continued reform progress. But this is often a behavioral error. For global investors, the lesson applies whether or not you own Indian or Emerging Markets stocks: Shock events can cause short-term wiggles or even corrections (sharp, sentiment-driven drops exceeding -10%), but if they don't alter a country's long-term fundamentals, staying cool is usually the right move.

India's cash-heavy economy has long been tax officials' scourge. Some estimates put the public's cash holdings at about 12% of GDP, far higher than the 4% average among Emerging Markets. Most savers stash bills at home, and less than half of India's population has a bank account. This is partly because rural areas are underbanked, and partly because Indian banks don't enjoy much public trust-the biggest are state-run, bloated, shaky and often linked to corruption. Credit cards and debit cards are rare, making it easy to keep transactions under the table. Because India's tax system used to be heavily decentralized and impossible to navigate, citizens had a big incentive to deal in cash and stay off the books. As a result, massive quantities of cash transactions go unreported. This "black economy" reportedly ranges from 20 - 50% of GDP.

This summer, Parliament passed a landmark Goods and Services Tax (or GST) aimed at streamlining tax collection-thus ending that decentralized morass-and combating evasion. But successful implementation requires getting black money out of the shadows and on the books. Substituting new notes for old theoretically forces everyone to declare and exchange their stashes, either revealing illicit funds (thereby subjecting them to taxation and potentially investigation) or rendering them worthless.

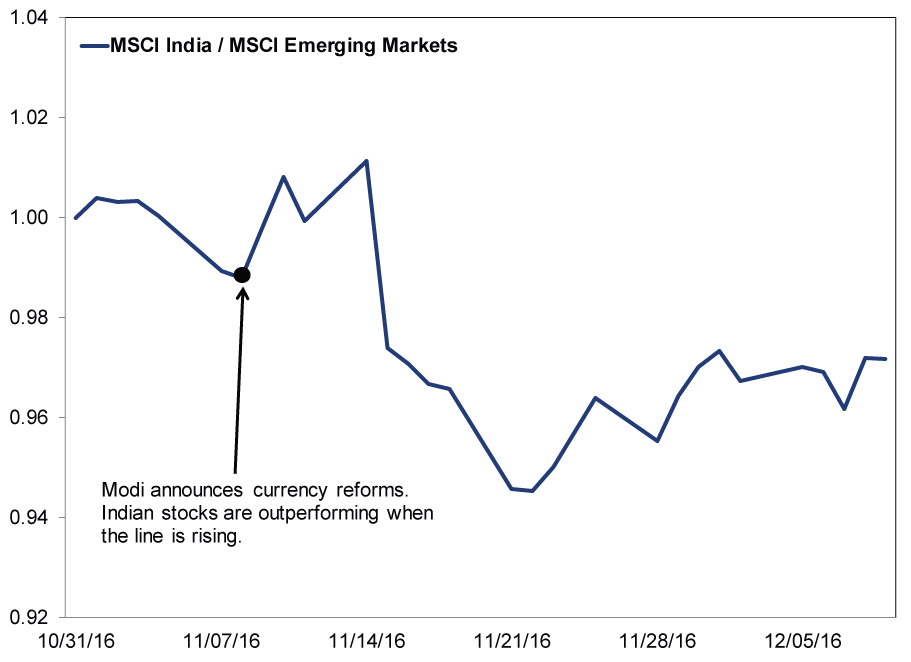

This move should be beneficial in the long run, provided further reforms address the reasons Indians hold so much cash, along with corruption's causes. Indian stocks initially outperformed on the announcement, perhaps seeing it as another win for Modi's administration. But fear soon took over as the implementation stumbled. Indian stocks tumbled, both on an absolute basis and relative to Emerging Markets. By November 21, the MSCI India Index was down -10.1% since Modi announced the reform on November 8-a textbook correction.[iii]

Exhibit 1: Indian Stocks' Relative Returns

Source: FactSet, as of 12/12/2016. MSCI Emerging Markets and MSCI India Index returns with net dividends, indexed to 1 at 10/31/2016.

It is easy to see why the fallout whacked sentiment. People stood in hours-long lines to exchange their old currency. Not just sheepish tax evaders and money launderers, but millions of ordinary people, all of whom needed cash to go about their daily routines as consumers or merchants. However, there weren't enough new bills to go around, and ATMs had to be retrofitted to handle the new bills, which were slightly smaller than the old-a lengthy, labor-intensive process ATM providers got no advance notice of. Sellers demanded payment in new currency customers didn't yet have, and companies couldn't pay workers, so business staggered. Almost 90% of India's trucks were stuck for days at gas stations, toll booths and delivery locations, unable to pay with old banknotes. The aftermath echoes a sudden money supply contraction, which tends to cause a negative economic shock if severe enough.

Complete data won't be out until January, but preliminary evidence suggests India's economy took a hit: November manufacturing and services surveys both slowed, the latter into contractionary territory. Yet stocks have already begun rebounding: Even as more problems came to light and data started trickling in, Indian stocks are up 6.5% since November 21. It appears markets are getting over the shock and moving on. This seems rational to us: Despite the botched rollout, India has many strengths. GDP grew 7.3% y/y in Q3, the fastest among major economies. Modi's reforms are starting to bear fruit. Challenges remain, but India's longer-term outlook appears plenty positive. As Ben Graham said: Stocks act like voting machines in the short term, but in the long run, they're weighing machines.

This is the latest example of a seemingly chaotic political event roiling stocks and unnerving investors, only for markets to rebound, rewarding the patient-an object lesson for all investors. Consider, for example, China's surprise yuan revaluation in August 2015. Folks feared a currency war, a long-awaited Chinese hard landing or worse. Global stocks had been faltering since May, and the news sent them down sharply while Chinese markets plunged-but the bull market continued. Stocks clawed back most of their losses, only for another Chinese currency move and the botched rollout of China's bizarrely constructed stock trading circuit breakers-which had the opposite of their intended effect-to knock markets anew in early January. But that double-dip correction ended February 11, and world stocks have since rallied to new all-time highs. Most recently, South Korean stocks tumbled after an influence peddling scandal involving President Park Geun-hye came to light, but they soon turned the corner and rallied as the legislature voted to impeach her.

It's normal to be nervous about headline-grabbing political events, whether scandals or seemingly odd reforms. When markets react, it can feel like fundamentals radically shifted overnight. You can point to a tangible reason. But short-term events rarely alter a country's long-term course, as these examples show. Remember this the next time something weird happens and it feels like the rug was pulled out: Stay cool, don't make hasty moves, and think critically about whether recent events will still be going concerns in 12 to 18 months.

[i] That's about $7.40 and $14.80, respectively.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today