Personal Wealth Management / Economics

Japan: Rising Sun or False Dawn?

Rekindled optimism over Japanese stocks seems premature.

Japan's trade deficit narrowed in June, with exports jumping 9.5% y/y, the fastest rate in five months-causing some to cheer. But factoring out the weak yen, export volumes stagnated, which may turn those smiles upside down. This pretty much exemplifies Japan's recent economic and political developments: On the surface, things appear better. Underneath, troubles remain. These trade data, combined with other recent weak economic data and middling economic reform progress, suggest reality isn't likely to live up to investor optimism. With little fundamental support, Japan's year-to-date outperformance is likely a mirage, and in our view, other regions of the world look more attractive for the foreseeable future.

What's behind the values/volumes disconnect? Currency conversion. The yen weakened considerably over the last year, largely due to the Bank of Japan's alleged monetary "stimulus." When Japanese firms convert revenues earned abroad back to yen, they get a bump up. Export growth (in value terms) can boost some export-oriented firms' profits.

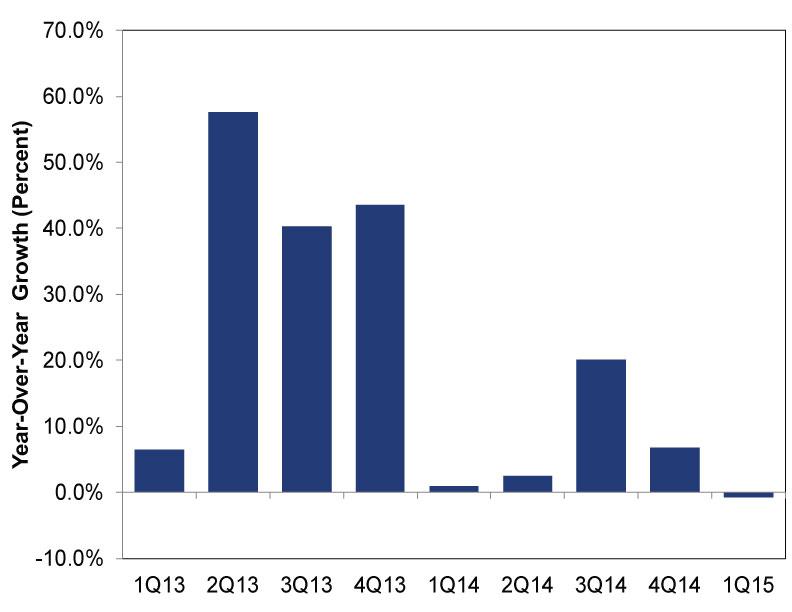

However, don't overstate this benefit. The weak yen makes imported goods more expensive, and many Japanese manufacturers import raw materials and components, including energy. Just as the strong dollar doesn't doom US profits, the weak yen is not a panacea ensuring big gains in Japanese firms' earnings. Iffy profit growth the last few years further illustrates this.[i] (Exhibit 1) Many investors underappreciate the offsetting effects of a weak or strong currency.

Exhibit 1: Japan Corporate Profit Growth 2013-2015

Source: Factset, as of 7/24/2015. MSCI Japan year-over-year earnings growth.

For the economy, export volumes are key to boosting growth. Stimulus proponents expected a weaker yen would boost profits and export volumes, driving up production, wages and hence, consumption. It was supposed to trigger a virtuous cycle. But this requires firms to sell more stuff in quantity terms. Absent volume growth, you don't get much increased production, component and raw materials reordering, hiring, factory expansion, equipment upgrades, etc. Firms downstream don't benefit and similarly deploy capital to increase production capacity. Volume growth is key, but absent.

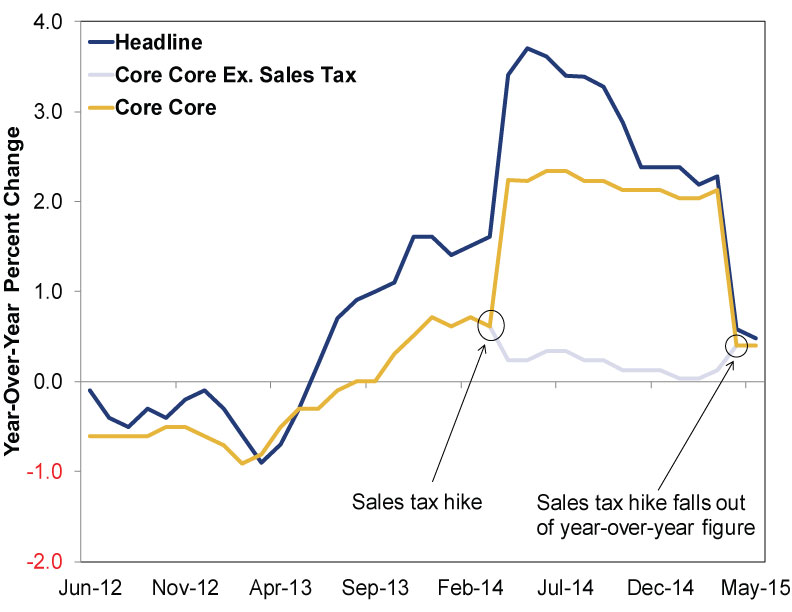

Lackluster export volume growth is one piece of evidence Japan's massively expanded quantitative easing (QE) isn't a net benefit. QE aims to boost ultra-low inflation and juice the economy. But there is ample evidence elsewhere Japan's QE program isn't spurring the economy much at all. Exhibit 2 shows Japanese inflation, both headline and core-core (excluding food and energy) since 2012. Inflation hovered around zero for a while, then shot up briefly in 2014. Yet while some cheered the rise, it too was illusory-the gain was entirely due to the one-time impact of Japan's sales tax hike. Absent that, inflation is basically flat.

Exhibit 2: Japan Consumer Price Index 2012 - 2015

Source: Factset as of 7/24/2015. Japanese CPI, CPI ex. energy and food, and CPI ex. energy, food and the sales tax hike.

The BoJ claimed sharply falling energy prices have kept inflation from reaching their target this year-which may have a grain of truth to it. But flattish inflation preceded oil's big fall. The BoJ hasn't admitted it, but theory and experience elsewhere globally suggest to us quantitative easing is dis- or deflationary, not stimulus.

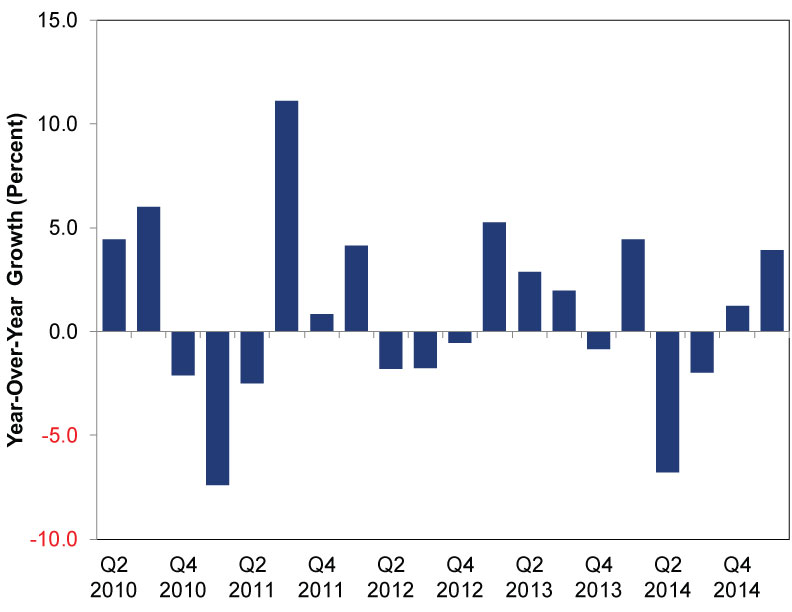

At a broader level, Japanese GDP growth has been overall anemic throughout this global expansion. (Exhibit 3) That's true since Abe took office, too. The economy slipped back into recession last year-Japan's third since 2009. It emerged in Q4 2014 and grew nicely (3.9% annualized) in Q1 2015. However, most analysts expect a far weaker Q2-the median forecast of 25 analysts projects 0.8% growth, but some expect contraction as deep as -2.5%. The Conference Board's Leading Economic Index for Japan is in a persistent downtrend, falling -0.1% m/m May after a flat April read and a -0.4% drop in March.

Exhibit 3: Japan GDP Growth 2010 - 2015

Source: Factset as of 7/24/2015.

Monetary stimulus was a big plank in PM Shinzo Abe's "Abenomics" platform, but economic reform was always the swing factor. Japan has passed some measures, and these have somewhat benefited the economy. But they're likely too small to materially boost Japanese competitiveness, and obstacles remain for some of the more impactful items on Abe's agenda. Curbing the influence of vested interests opposing reform remains a challenge. For example, this year's agricultural reforms were heavily watered down from Abe's original proposals, illustrating the agricultural lobby maintains its powerful (often counterproductive) grip on Abe's Liberal Democratic Party-that, in turn, makes meaningful agricultural tariff reductions unlikely. Japan cut corporate income tax rates, but they remain among the developed world's highest. Combined national and local tax rates went from 34.62% to 32.11% this year, and will fall to 31.33% next year. Abe continues to claim he'll push rates below 30%, but when is anyone's guess.

Corporate governance reforms passed and took effect in June to great fanfare, with many expecting an influx of outside directors to shake things up and make firms more accountable to shareholders. While a nice step, this was low-hanging fruit, and the changes don't appear to cut deep enough to tackle deep-seated problems among Japan's bloated conglomerates. Labor reforms passed last month are similarly small-a beneficial step, but insufficient to overhaul the culture of lifetime employment, which most observers agree is a ginormous roadblock to productivity.

This and other items remain on Abe's agenda, but passage will require significant political capital-political capital Abe may choose to spend elsewhere. His focus seems to have flipped back to national security, in line with his lifelong quest to revise Japan's pacifist post-WWII constitution. This is unpopular with Japanese voters, who have sent Abe's poll numbers to their lowest since he took office. The more energy he spends on the military, the more his popularity slides, and the less clout he has over entrenched interests.

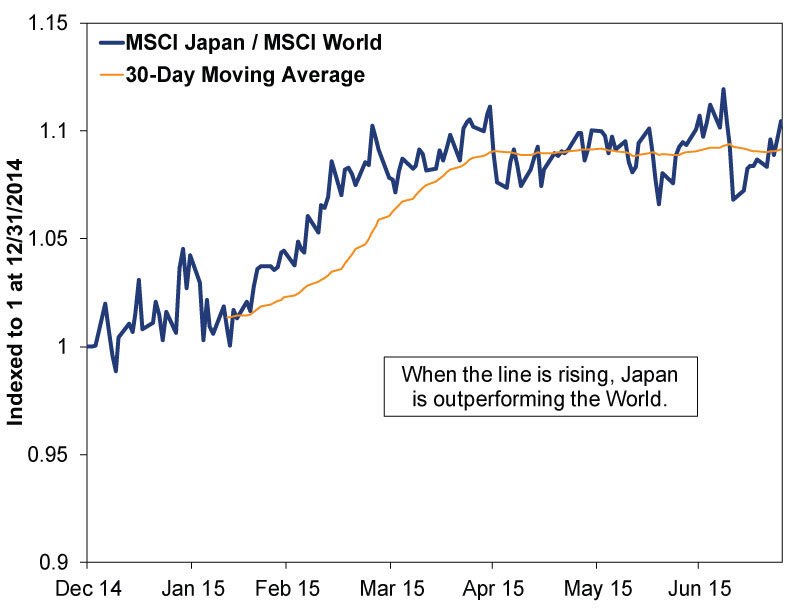

It seems Q1's growth uptick and a few nice-but-smallish reforms rekindled the over-optimism that triggered short-lived bursts for Japanese stocks in 2013. Outperformance didn't last then, and it appears similarly temporary now. As Exhibit 4 shows, Japanese outperformance has leveled off since the early 2015 burst. We wouldn't be surprised if it slid the other way soon. With few signs sustainable growth has arrived and Abe's focus moving off the economy, it seems investors are catching on gradually that the sun hasn't risen on Japan.

Exhibit 4: MSCI Japan / MSCI World 2015 To Date

Source: Factset, as of 7/24/2015.

[i] The growth rates in 2013 may seem big, but they are building off a very depressed base.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Insights Ken Fisher on Inflation Data, Currency Reset Risks, Commodity Opportunities and More– April 20262026-04-17

-

Market Analysis Foraging Through Japan’s February Data2026-04-17

-

Expert Commentary This Week in Review | Iran Conflict Update, Canada Election, UK GDP

2026-04-17

2026-04-17 -

Market Analysis An Economic Check In on the UK2026-04-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today