Personal Wealth Management / Market Analysis

Japan Staggers Back Into Contraction

Japan's economic struggles aren't surprising.

Global economic growth has gotten a bum rap for most of this expansion. In most folks' estimation, the US is just barely holding up the rest of the world (especially Emerging Markets) and the specter of recession-or worse-looms. Yet in recent years, investors have given one country the benefit of the doubt: Japan. We always thought it was unwarranted, as the structural economic reforms required to invigorate Japan's stagnant economy never materialized. Growth has been choppy, and Japan's GDP contracted in Q4, underscoring the country's economic struggles. We don't believe these are likely to abate any time soon, disappointing investors who hold out hope for the Land of the Rising Sun.

According to the Cabinet Office's first estimate of GDP, Japan contracted at a -1.4% annualized rate in Q4 (-0.4% q/q), mirroring Q2's decline. One of the biggest detractors: private consumption, which fell -3.3% annualized. Imports, a key indicator of domestic demand, dropped -5.6% annualized, while exports declined -3.4%. The lone positive was business investment, which rose for a second straight quarter at 5.7% annualized, though we wouldn't get too excited considering this very bouncy gauge has been negative in 8 of the past 16 quarters.[i] Japan did eke out meager growth for calendar year 2015, but 0.4% growth hardly set the world on fire. Though private capex rose 1.3%, private consumption dropped -1.2%. Imports rose just 0.2%, while exports gained 2.7%, though that figure should carry an asterisk as it is mostly a currency translation phenomenon. In volume terms, exports fell -0.9%, and imports fell -2.8%. Bleakness continued in January, when export volumes fell -9.1% y/y and imports fell -5.1% y/y. Though government consumption rose 1.1% in 2015, much of it was from a big fiscal spending package at the beginning of the year-yet another case of fiscal stimulus failing to provide a lasting boost.

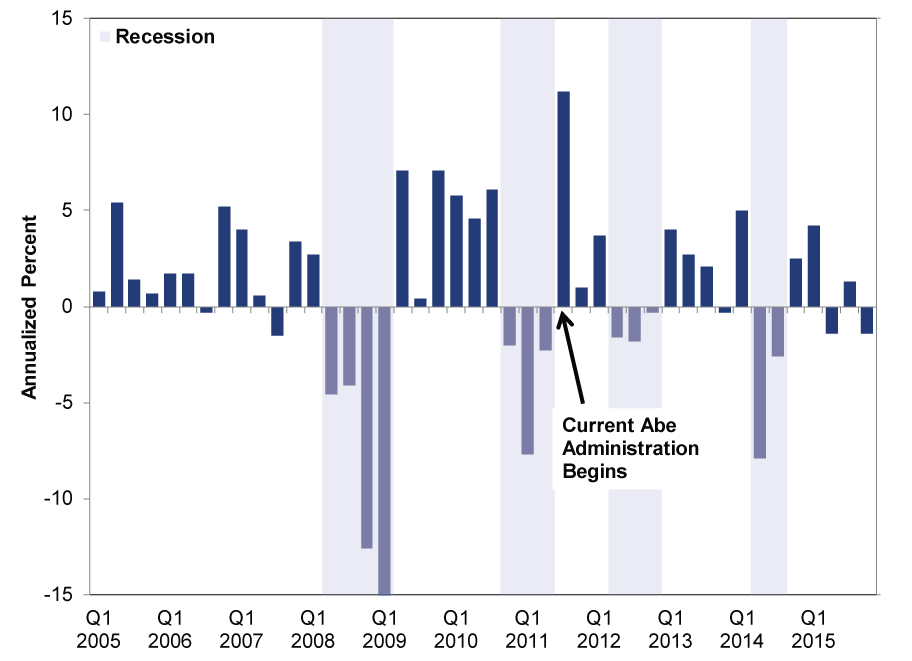

Efforts to revive a flagging economy through fiscal and monetary stimulus have produced lackluster results for years now. At the start of his term, Prime Minister Shinzo Abe announced a three-pronged attack to revitalize Japan: fiscal stimulus, accommodative monetary policy and hard-hitting structural reforms-the much-ballyhooed "Abenomics" program. Officials quickly launched the fiscal and monetary arrows but dragged their feet on reform, and the Abe era[ii] hasn't altered the economy's overall trajectory. (Exhibit 1).

Exhibit 1: Japanese GDP Annualized Growth, Quarter-Over-Quarter Since 2005

Source: Cabinet Office, as of 2/16/2016.

Since Abe took office at the end of 2012, Japan has contracted in 5 of 12 quarters-not exactly a ringing endorsement of Abenomics.[iii] Consider monetary stimulus. The BoJ's greatly hyped "quantitative and qualitative easing" (QQE) weakened the yen, theoretically making Japanese exports cheaper abroad. Policymakers hoped this alleged boost to exporters would spill over to the rest of the economy, boosting growth as they plowed profits from currency translation into new production lines and product development.

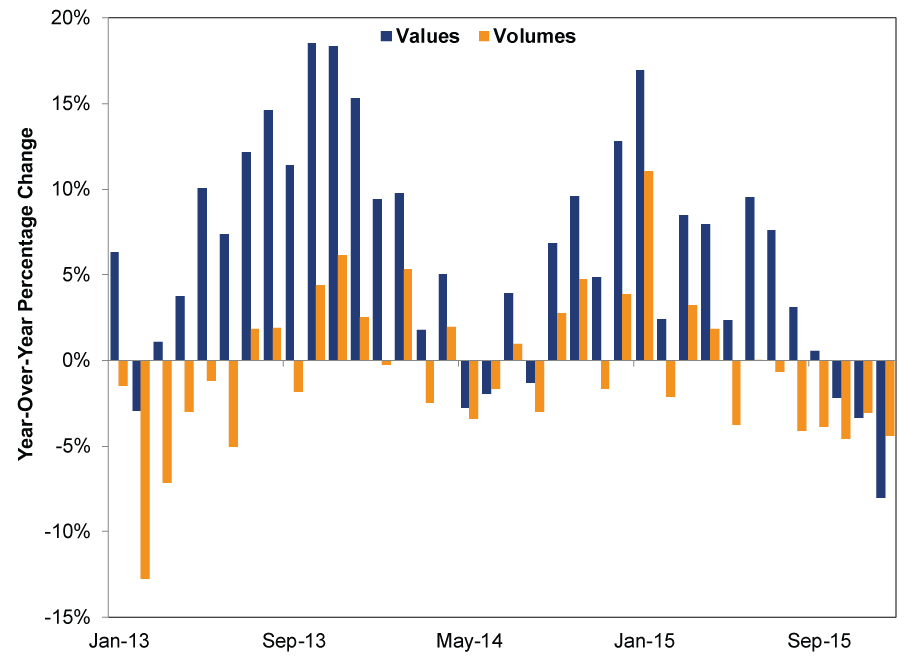

Now, exports did get a temporary boost. But this was primarily in value terms, reflecting yen weakness rather than a meaningful boost in demand. Volumes-which show the amount of actual stuff getting moved-struggled. (Exhibit 2) That big production boost never happened, as producers preferred to hold prices steady abroad and pocket the extra profits from currency translation, rather than cut prices to raise sales volumes and ramp up production lines and product development.

Exhibit 2: Year-Over-Year Japanese Exports, Value vs. Volume, Since 2013

Source: Trade Statistics of Japan, Ministry of Finance, as of 2/16/2016.

And after export volumes spent much of 2015 in negative territory, values followed toward the latter half of the year as the yen began strengthening-further evidence growth was a currency translation phenomenon, not an actual, lasting economic boost.

Yet many still hold a high opinion of QQE's alleged stimulating effects on markets. Sentiment and expectations were high once Abe took office in 2013, as investors anticipated the new prime minister would revitalize Japan after 15 years of stagnation. Though Abe talked up reforms, he passed little, instead papering over the cracks with more stimulus. Yet many investors interpreted the stimulus measures as precursors to reform, sometimes causing sentiment to swell. Now, with more signs the economy is flagging, the BoJ may resort to yet more stimulus-the BoJ and Governor Haruhiko Kuroda have shown a preference to change investor expectations through surprise and unconventional monetary policy. However, we believe the result would be the same-sustainable economic growth won't return without meaningful reform, especially with negative rates needlessly taxing the banking system.

Despite some incremental reform progress, Abe has barely scratched the surface. Small achievements include: the first nuclear power plant restart last year (in the works for two years); a new corporate governance code, which aims to shake up the old guard in Japan, Inc.; and signing the Trans-Pacific Partnership (TPP), a trade pact that will cover about 40% of the global economy if ratified and enacted. And outsiders may finally be penetrating Japan, Inc.'s bubble, as a Taiwanese electronics manufacturing company is close to taking over a big Japanese tech company-with the government's blessing, which would end a long history of the government artificially propping up failing conglomerates.[iv]

These are all nice positives, but surface-level. For instance, there is no guarantee TPP becomes reality as politics in the 12 participating countries might get in the way. Even if TPP goes live, phase-in periods are lengthy-Japan gets 16 years to reduce its beef tariff, for example, which isn't exactly radically freer trade. The long-insulated agriculture industry has protected about 70% of 586 products from becoming tariff-free in the TPP. Japan's byzantine labor code and immigration policy remain largely untouched. Though these types of reforms won't reverse Japan's fortunes immediately, they would lay the groundwork for a much more competitive, dynamic economy.

Making these reforms a reality requires political capital-a limited resource. Throughout his tenure, Abe has decided to use his on issues like controversial national security legislation and scrapping the Constitution's anti-war clause rather than taking on powerful vested interests (e.g., Japan's agriculture lobby). The pro-reform camp has also taken a big hit after Akira Amari, the minister for economic revitalization and one of Abenomics' chief architects, recently resigned amid a corruption scandal. In his place, Abe appointed former environment minister and Liberal Democratic Party secretary general Nobuteru Ishihara to the position. However, it is difficult to envision Ishihara making an immediate positive impact as it takes time for a new minister to navigate the landscape and learn the ropes. In our view, this sudden change likely hinders reform progress even more.

Though we remain pessimistic about its economic prospects, a weak Japan needn't take down the rest of the global economy. Since early 2009, Japan has had three technical recessions (defined as two or more consecutive quarters of economic contraction). Yet the global expansion has continued apace. Growth from other parts of the world-the US, UK, most of the eurozone and the many Emerging Markets that don't rely on commodity exports-is strong enough to overcome the laggards. While Japan may continue claiming sustainable growth is right around the corner, we suggest investors look elsewhere for investment opportunities.

[i] Or, if you're feeling more "glass-half-full," positive in 8 of the past 16 quarters. But we often get accused of being Pollyanna, so how do you like them apples?

[ii] This is actually the second Abe era, since he was also prime minister from September 2006 to September 2007. He's Japan's Grover Cleveland.

[iii] And a contraction in Q3 2015 was revised away in the following estimate.

[iv] Blessing may be a bit strong. "Tacit approval" may be more appropriate.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News In Orbit? On Tech Sentiment and IPOs2026-05-22

-

Market Analysis Global Bond Calamity Calls for Calm Perspective2026-05-22

-

Expert Commentary This Week in Review | UK Politics, Fed Developments, IPOs

2026-05-22

2026-05-22 -

Market Analysis CPI Sheds Light on Britain’s Price ‘Cap’ Conundrum2026-05-20

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today